Estimated reading time: 16 minutes

Key Takeaways

- RSUs are taxed as ordinary income upon vesting.

- Holding RSUs beyond the vesting date triggers capital gain/loss tax.

- RSUs show on your paystub with automatic tax withholding, which can be insufficient.

- Executives and insiders face restrictions on trading RSUs freely.

- The grant date signifies promised units, while the vesting date marks actual ownership of stock units.

- Developing a strategy around RSU taxes, in addition to understanding RSUs, can significantly build your asset base from RSUs.

- Proactive management of RSUs is essential to mitigate concentration risk, company-specific risk, and unsystematic risk.

Table of contents

- What Are RSUs?

- What are the tax implications if I sell my RSUs immediately after they vest?

- How can I minimize the tax burden on my RSUs?

- What are the tax differences between RSUs and stock options?

- Can RSUs affect my tax bracket and how can I plan accordingly?

- Why are RSUs taxed so high

- How are restricted stock units (RSUs) taxed when they vest?

- What are the tax implications if I sell my RSUs immediately after they vest?

- How can I minimize the tax burden on my RSUs?

- Are RSUs subject to capital gains tax when sold?

- You May Also Like

This blog post discusses everything you need to know about RSUs (Restricted Stock Units)—a seemingly simpler form of equity compensation, yet often challenging for tech professionals to navigate. Tech employees have busy schedules and they often prioritize what they are good at or what they enjoy doing. Many of them have entrepreneurial endeavors for their own ventures, apps, or software, which they could potentially fund using RSUs as a means to support these future aspirations.

Navigating RSUs can seem straightforward initially, but their various vesting schedules can lead to oversight. It’s common to overlook these schedules until RSUs accumulate substantially in value, potentially leading to missed opportunities for proactive management. Proactively optimizing RSU assets is crucial, even if understanding the concept is straightforward; managing it actively poses challenges. This blog aims to equip you with insights to manage your RSU assets effectively for future financial optimization, ensuring they work in your favor rather than becoming a surprise tax burden.

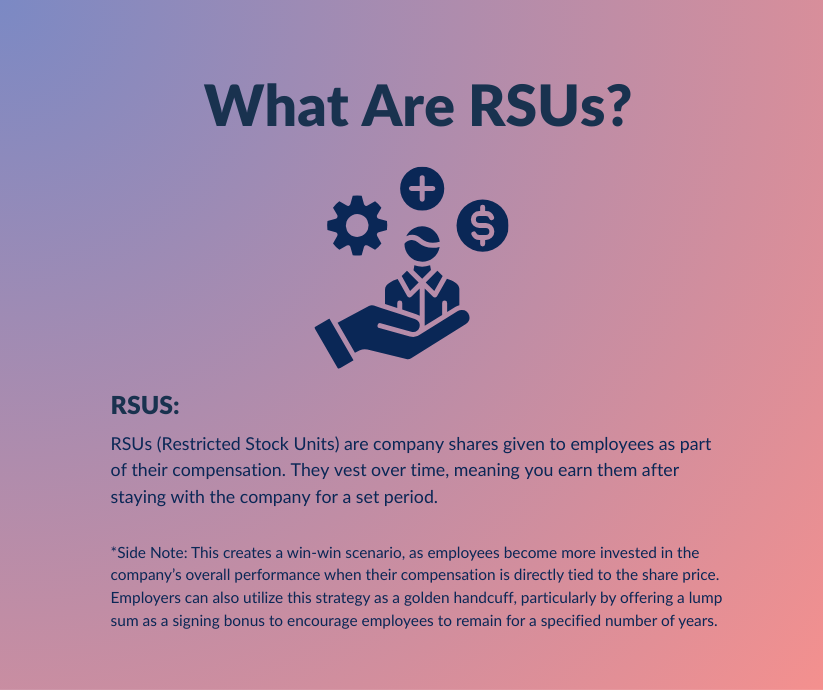

What Are RSUs?

Restricted Stock Units (RSUs) are compensation grants where your employer promises to deliver actual company shares once you satisfy specific conditions—usually staying with the company for a predetermined period. Think of them as IOUs for stock that convert to real ownership over time.

Here’s what makes RSUs unique: you receive no actual shares upfront. Instead, you’re granted units that represent future shares. When these units vest—typically following a schedule tied to your tenure—they automatically convert to company stock. At that moment, you own the shares outright and can hold or sell them.

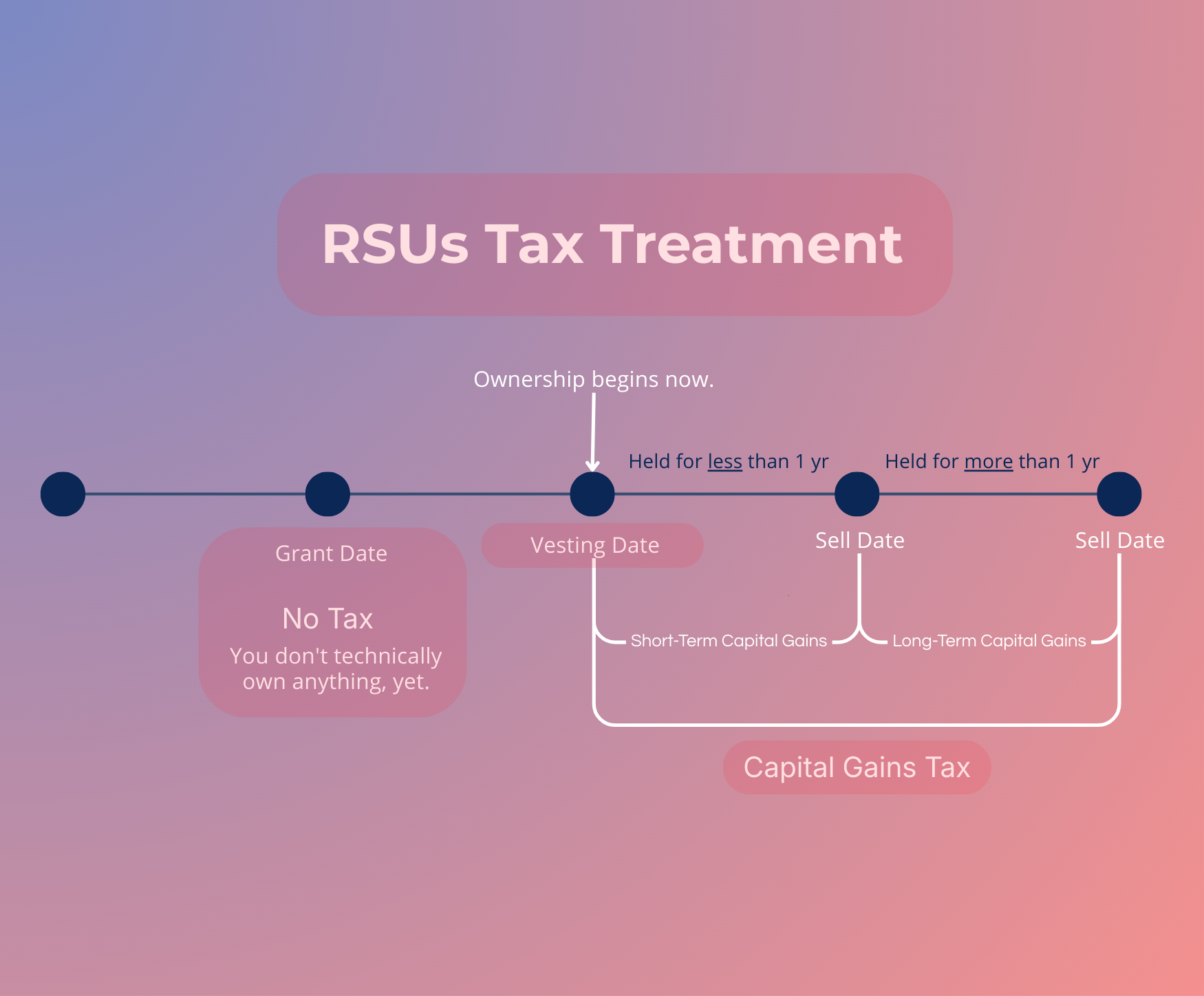

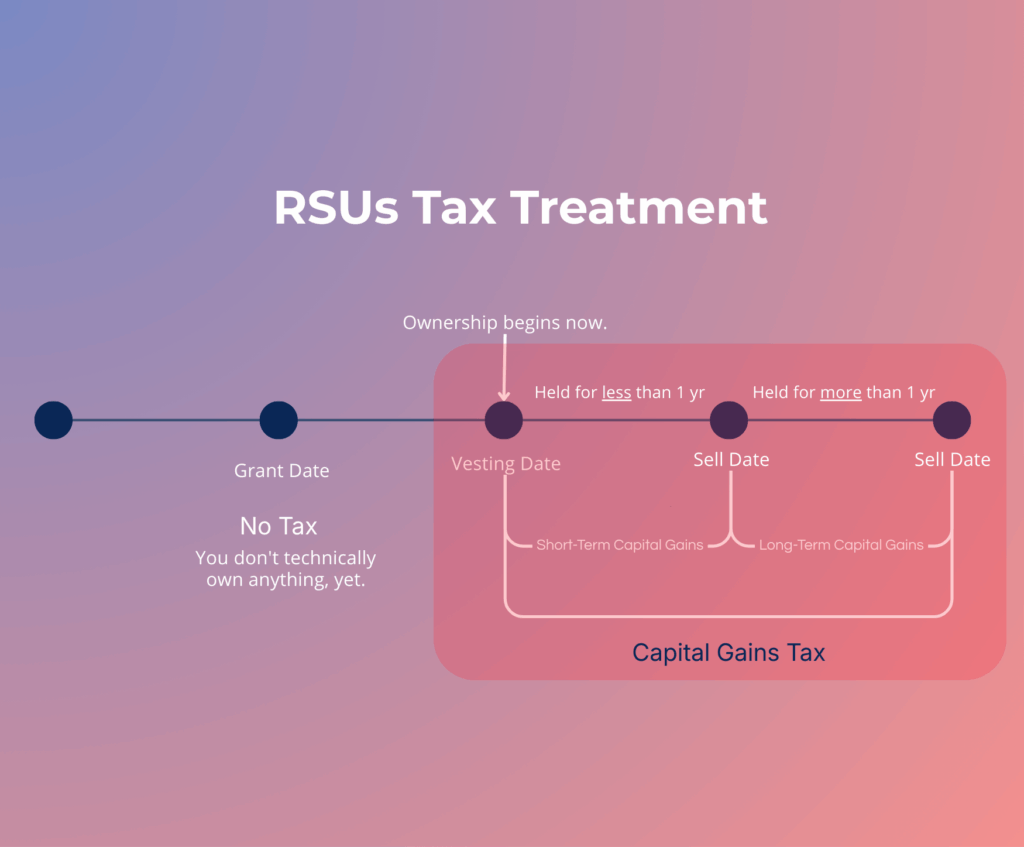

The critical distinction is timing. With stock options, you choose when to exercise and purchase shares. RSUs vest automatically according to the predetermined schedule, triggering immediate tax consequences. An RSU tax treatment example illustrates this perfectly: if 100 RSUs vest when your company’s stock trades at $150 per share, you recognize $15,000 as ordinary income that year—even if you never sell a single share. This automatic taxation catches many first-time recipients off guard, since you owe taxes before seeing any cash.

Most tech companies structure RSU grants with cliff vesting (often one year before any shares vest) followed by monthly or quarterly vesting periods. This structure aligns employee retention with company goals while building substantial equity over time—especially powerful when high-earning years coincide with multiple vesting events.

What are the tax implications if I sell my RSUs immediately after they vest?

Selling your RSUs immediately after vesting typically results in minimal additional tax liability beyond the income tax already withheld at vest. When your RSUs vest, you’ve already paid ordinary income tax on their fair market value—that tax burden is locked in regardless of when you sell. If you sell immediately, the sale price closely matches the vesting price, meaning you’ll have little to no capital gain or loss to report.

However, timing matters. Even selling within hours of vesting can trigger a small capital gain or loss if the stock price moves. For example, if your shares vest at $100 each and you sell later that same day at $102, you’ll owe short-term capital gains tax on the $2 difference. Conversely, if the price drops to $98, you can claim a $2 capital loss per share. These gains or losses are typically minimal when you execute the sale quickly.

The immediate-sale strategy eliminates the risk of additional tax liability from future price appreciation. By converting your equity to cash at vesting, you avoid the potential for substantial capital gains taxes that would apply if you held the shares and they increased in value. This approach also removes the uncertainty of whether future gains will be taxed as short-term (ordinary income rates) or long-term (preferential rates), making your tax situation more predictable and easier to plan around for the year ahead.

How can I minimize the tax burden on my RSUs?

Minimizing your RSU tax burden requires strategic planning throughout the year, not just at vesting. The most effective approach combines timing strategies, tax-loss harvesting, and charitable giving tactics. Common RSU mistakes often stem from reactive rather than proactive tax planning.

Maximize your tax-advantaged retirement contributions by increasing 401(k) deferrals to offset RSU income. If you know a large vesting event is coming, front-load your annual 401(k) contributions earlier in the year to reduce your overall taxable income in that period.

Tax-loss harvesting becomes particularly valuable when you’re holding previously vested shares that have declined. Selling these shares at a loss can offset the capital gains from selling appreciated RSUs, reducing your overall tax liability. However, be mindful of wash sale rules that prevent you from repurchasing the same stock within 30 days.

Consider charitable giving strategies if you’re charitably inclined. Donating appreciated RSU shares directly to qualified charities allows you to avoid capital gains taxes while claiming a charitable deduction. This strategy works best for shares held longer than one year that have significantly appreciated.

However, these strategies have limitations—you cannot eliminate the ordinary income tax triggered at vesting, and timing the market rarely works out as planned. The key difference between RSUs and stock options in minimizing taxes lies in their initial tax treatment, which we’ll explore next.

What are the tax differences between RSUs and stock options?

The fundamental difference is timing: RSUs generate taxable income at vesting with no upfront cost, while stock options typically create tax events only when you exercise them. Understanding these distinctions is crucial for accurate tax planning.

With RSUs, you face ordinary income tax automatically at vesting based on the shares’ fair market value that day. Your employer withholds taxes immediately, and you receive the net shares. There’s no purchase decision or upfront investment required.

Stock options work differently. You receive the right to buy shares at a predetermined price (the strike price). No tax occurs at grant—the tax event happens when you exercise those options and purchase the stock. For Incentive Stock Options (ISOs), you might avoid ordinary income tax entirely if you meet holding requirements, though Alternative Minimum Tax may apply.

The capital gains treatment also differs. For RSUs, your cost basis equals the vesting-day value already taxed as income. Any subsequent appreciation is capital gains. With options, the spread between strike price and sale price determines your tax treatment, which varies significantly between ISOs and Non-Qualified Stock Options (NSOs).

This distinction matters for residency changes, as your tax jurisdiction when RSUs vest versus when you exercise options can dramatically impact your tax bill.

Can RSUs affect my tax bracket and how can I plan accordingly?

RSUs can absolutely push you into a higher tax bracket, particularly during large vesting events. When multiple RSU grants vest simultaneously, the concentrated income can create what feels like an unexpectedly high tax bill. The vesting value gets added to your regular salary, potentially moving you from, say, the 24% federal bracket to 32% or even 35%.

A common pattern is underestimating the impact of multiple vesting tranches coinciding with year-end bonuses or stock price appreciation. According to financial planning research, one of the most frequent RSU mistakes is failing to account for the full tax impact of concentrated vesting schedules. Your withholding rate—often the supplemental wage flat rate of 22%—may not cover your actual marginal rate, leaving a balance due at tax time.

Strategic planning helps minimize bracket creep. Consider timing charitable contributions or retirement plan contributions in heavy vesting years to offset the additional income. If your company allows it, coordinate with HR to stagger vesting dates across calendar years. Some tech employees strategically time large deductible expenses—like business investments or home office improvements for contractors—during peak vesting periods.

What typically happens without planning is a tax surprise in April, followed by scrambling for estimated quarterly payments the following year. Understanding these bracket dynamics now positions you to make informed decisions about RSU sales and tax-loss harvesting strategies, which become even more critical when tax rates seem disproportionately high on equity compensation.

Why are RSUs taxed so high

RSUs aren’t actually taxed at a higher rate than your salary—they just feel that way. The perception stems from how RSUs are taxed at vesting: they’re treated as ordinary income and subject to immediate withholding, often at the mandatory federal supplemental wage rate of 22% (or 37% if your total supplemental wages exceed $1 million).

This withholding rate may not match your actual tax bracket. If you’re in the 24% or 32% bracket, the 22% withholding could leave you with an unexpected tax bill come April. Conversely, if you’re in the 12% bracket, you’ll receive a refund, but the cash flow impact at vesting still stings.

According to Restricted Stock Units and How They Work, many employees mistakenly believe their RSUs face double taxation when they eventually sell the shares. In reality, only the appreciation beyond the vesting price faces capital gains tax—the initial vesting amount was already taxed as income.

The timing concentrates the pain: a large vesting event can push tens of thousands into your income in a single pay period, triggering Social Security, Medicare, state, and local taxes simultaneously. When your employer withholds shares to cover these obligations, it feels like a significant chunk disappeared overnight. Understanding how RSUs are taxed when they vest clarifies why the effective rate appears so steep.

How are restricted stock units (RSUs) taxed when they vest?

The moment your RSUs vest, they’re taxed as ordinary income—just like your salary. The fair market value of the shares on the vesting date becomes taxable compensation, reported on your W-2.

Your employer typically withholds taxes through share-withholding, where they keep a portion of your vested shares to cover federal, state, and FICA taxes. The standard withholding rate is 22% for federal taxes (or 37% for supplemental income exceeding $1 million), but this might not cover your full tax liability if you’re in a higher bracket.

What catches many women off guard: you owe taxes even if you don’t sell a single share. Unlike stock options where you can choose when to exercise, RSU taxation is automatic at vesting. This creates an immediate tax bill based on the shares’ current value, regardless of whether you plan to hold or sell them.

After vesting and initial taxation, any future appreciation becomes a capital gains matter—which brings us to the important decision of whether to sell immediately or hold your vested shares.

What are the tax implications if I sell my RSUs immediately after they vest?

Selling immediately after vesting typically results in minimal additional taxes—though you’ll likely recognize a small gain or loss. Since you already paid ordinary income tax on the shares’ value at vesting, selling right away means the cost basis is established at that vesting-day price.

The tax implication depends on how much the stock price changed between vesting and sale. If you sell within days of vesting and the price moved $2 per share, you’ll recognize a short-term capital gain or loss on that $2 difference. A common pattern is to see either a negligible gain or a small loss if the stock dipped slightly post-vesting.

This “sell immediately” approach is often favored by those looking to minimize concentration risk in a single company’s stock. However, any gain—no matter how small—from selling within a year is taxed at ordinary income rates as a short-term capital gain, not the preferential long-term rate.

The real benefit of immediate sales isn’t tax savings; it’s liquidity and diversification. You avoid the uncertainty of holding volatile stock and can redirect proceeds toward broader investment goals or debt reduction—considerations that become increasingly important as you think about strategies to reduce your overall tax burden.

How can I minimize the tax burden on my RSUs?

The most effective strategy is timing your tax liabilities strategically—though your options are more limited than with stock options. Since you can’t control when RSUs vest (that’s set by your company), focus on what you can control: the timing of sales and your overall tax planning.

One practical approach involves selling shares immediately upon vesting to cover the tax bill, then diversifying the remainder. According to The Most Common RSU Mistakes, many tech employees make the mistake of holding too much company stock, creating unnecessary concentration risk. Selling strategically helps manage both taxes and portfolio balance.

Consider these tax-minimization tactics:

- Contribute to tax-advantaged accounts like 401(k)s and HSAs in high-income years to lower your adjusted gross income

- Harvest tax losses from other investments to offset gains when you eventually sell RSUs

- Time discretionary income (bonuses, consulting work) to avoid stacking too much ordinary income in one year

- Plan around vesting schedules by adjusting withholding or estimated payments to avoid underpayment penalties

However, avoid common pitfalls like refusing to sell vested shares solely for tax reasons. The bigger risk is often concentration, not the capital gains rate you’ll face later. What typically happens is that employees watch their company stock decline while trying to hold long enough for favorable tax treatment—erasing any tax savings.

Your goal isn’t eliminating taxes entirely—it’s optimizing your after-tax wealth by balancing tax efficiency with smart diversification.

Are RSUs subject to capital gains tax when sold?

Yes, but only on gains that occur after vesting—the difference between your sale price and your cost basis (the fair market value at vesting). When you sell RSUs, you’ll owe capital gains tax on any appreciation that occurred while you held the shares. If you sell immediately after vesting, there’s typically little to no capital gain since the price hasn’t changed much. However, if you hold the shares for months or years, any increase in value is subject to capital gains tax.

The holding period matters significantly for your tax rate. Selling within one year of vesting triggers short-term capital gains, taxed at your ordinary income rate (up to 37%). Hold for more than a year, and you qualify for long-term capital gains rates (0%, 15%, or 20% depending on your income)—a substantial savings for many tech professionals. This distinction becomes increasingly important as your RSU holdings grow and appreciation accumulates, making the decision of when to sell a strategic tax consideration alongside your investment and diversification goals.

What are the tax differences between RSUs and stock options?

The fundamental difference is when you owe taxes—RSUs trigger ordinary income tax automatically at vesting, while stock options give you control over timing through the exercise decision. This distinction affects both your tax liability and planning flexibility.

With stock options, you choose when to exercise (and trigger taxes), potentially timing it for lower-income years or favorable market conditions. RSUs offer no such flexibility—the IRS treats vesting as a taxable event regardless of whether you sell the shares or hold them.

Stock options also create different tax categories: Incentive Stock Options (ISOs) can qualify for preferential capital gains treatment if you meet holding requirements, while Non-Qualified Stock Options (NSQOs) trigger ordinary income tax at exercise. RSUs, by contrast, always generate ordinary income at vesting—there’s no path to convert that initial gain into capital gains.

One practical advantage RSUs do offer: you can’t be underwater. Stock options become worthless if the strike price exceeds the current stock price, while RSUs always have value at vesting (even if lower than grant price). However, this guaranteed value comes with guaranteed taxes at every vesting event, making tax planning essential as you transition to reporting your RSU income on your return.

How do I report RSU income on my tax return?

Your RSU income appears automatically on your W-2—the value at vesting is reported as compensation in Box 1, and taxes withheld show in the appropriate boxes. However, common reporting mistakes occur when selling shares after vesting.

When you sell vested RSUs, you’ll receive a Form 1099-B from your brokerage showing the sale proceeds. The critical step is reporting your cost basis correctly on Schedule D—this is the fair market value on the vesting date, already taxed as income. Many people accidentally double-report income by not properly accounting for this basis.

Keep your vest date documentation from each vesting event. If you sold shares throughout the year, match each sale lot to its original vesting date and value. Tax software can help automate this, but verify the basis calculations align with your records—not all brokerages report basis accurately.

Understanding residency rules becomes increasingly important if your location changes, which we’ll explore next.

What happens to the tax treatment of RSUs if I change my residency status?

Changing residency creates a complex tax situation that depends on when you relocate relative to when your RSUs vest. If you move states after receiving an RSU grant but before vesting, both your old and new states may claim the right to tax that income based on where you physically worked during the vesting period.

States use different methods to determine how much income they can tax. California, for example, uses a sourcing formula that allocates RSU income based on the number of days worked in the state divided by the total service period. If you worked in California for two years of a four-year vesting schedule before moving to Texas, California may tax 50% of each vest even after you’ve left.

Moving to a state with no income tax—like Texas, Florida, or Washington—can provide significant savings on future vests, though you’ll still owe federal taxes. The reverse situation creates unexpected tax bills: relocating from a no-tax state to California or New York means higher taxes on subsequent vests.

International moves add another layer of complexity involving tax treaties and potential dual taxation. Each country has different rules about when RSUs become taxable and how to credit taxes paid elsewhere. Document your relocation dates carefully and consult with a tax professional who understands multi-state equity compensation rules well before making any move. The tax implications of relocating could impact your overall compensation package by tens of thousands of dollars.

Can RSUs affect my tax bracket and how can I plan accordingly?

Yes, RSUs can absolutely push you into a higher tax bracket—the vesting value counts as ordinary income in the year shares vest, potentially creating a significant spike in your taxable income. A common scenario involves receiving a substantial RSU grant that vests all at once or in large tranches, which can unexpectedly bump you from the 24% federal bracket into the 32% or even 35% bracket.

Strategic timing matters more than you might think. If you have control over certain financial decisions—like exercising stock options, realizing capital gains, or making large charitable contributions—concentrate these moves in years with lower RSU vesting to smooth out your tax burden. Conversely, maximize deductions and tax-advantaged contributions during high-vesting years. One of the most common mistakes is failing to adjust withholding or estimated payments, which can trigger underpayment penalties.

Tax bracket planning requires a multi-year perspective. Review your vesting schedule now and project your income for the next 2-3 years. Consider strategies like bunching charitable deductions, maxing out retirement contributions ($23,000 for 401(k)s in 2024), or accelerating/deferring other income sources when possible. However, acknowledge this limitation: you typically can’t defer RSU vesting itself, so your primary control lies in managing everything else around those vesting events.

Take control of your RSU tax strategy today. Calculate your projected income with upcoming vests, adjust your W-4 withholding if needed, and consult a tax professional or a financial planner specialized in working with tech professionals before year-end to optimize your approach—waiting until tax season means missing opportunities to reduce your burden.