Written by Hazel Secco, CFP®, CDFA®

Estimated reading time: 7 minutes

Table of contents

Introduction

Most of us don’t think twice about trimming down concentrated positions in our investment portfolios—unless that position happens to be our own company’s stock. For many high-achieving women with RSUs, stock options, or ESPPs, the same person who is disciplined and diversified everywhere else suddenly becomes hesitant, emotional, and overly attached when the shares belong to the company they work for. I’ve seen this repeatedly in my work, and I’ve experienced it personally. In fact, watching my own reaction to my husband’s RSUs is what led me to name this phenomenon: Home Stock Syndrome™.

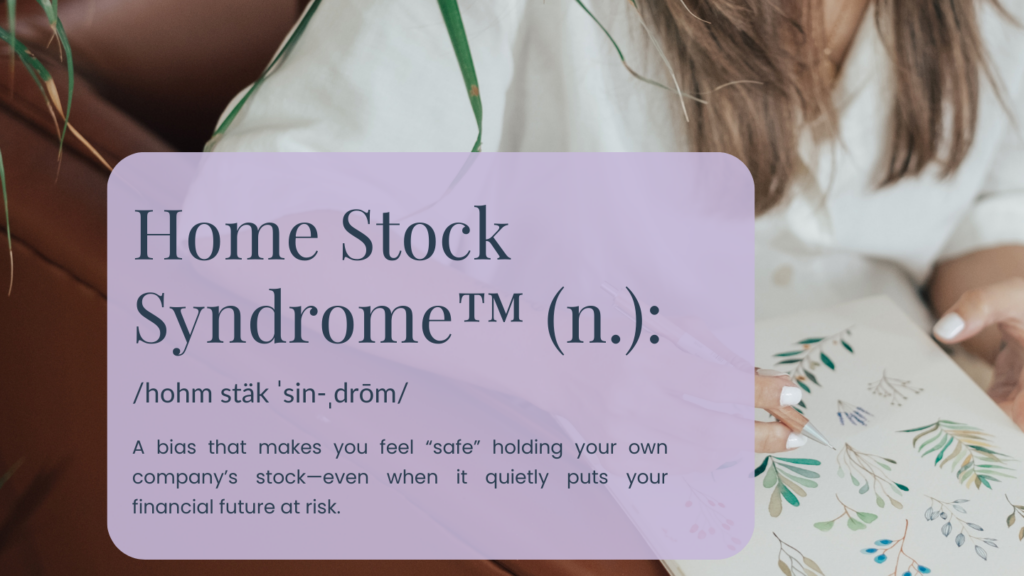

What Exactly Is Home Stock Syndrome™?

Home Stock Syndrome™ is the prevalent emotional bias that appears when someone underestimates the risk of holding their own company’s stock—not because the financial fundamentals support it, but because the emotional attachment makes it feel safe.

You work there. You know the people. You understand the product. You believe in the mission. You may even feel like selling your shares is a sign that you don’t trust the very organization you show up for every day. This emotional loyalty can cloud even the most rational financial judgment, and for women in pharma, biotech, and large corporate environments, the attachment tends to run even deeper. When you’ve poured years into building a reputation, launching major projects, or contributing to something meaningful like a life-changing drug approval, the stock doesn’t feel like “just an asset.” It feels personal.

What Home Stock Syndrome™ Sounds Like

If you’ve ever caught yourself thinking, “It’s different—this is my company,” or “I’ll wait until the stock rebounds,” you’re not alone. Many people say things like, “I trust the leadership team,” or “It’s not that risky; I’ll deal with it later.” But the truth is simple: if this stock weren’t tied to your company or your identity, you wouldn’t treat it with the same loyalty. You would look at it objectively. You would diversify. You would manage the risk. You would run the numbers with a clear head. Home Stock Syndrome™ convinces you that holding is safer than selling, even when the opposite may be true.

Why It’s a Problem (Especially for Women in Pharma & Corporate Leadership)

If your compensation includes RSUs, stock options, or ESPPs (which it likely does), you’re already relying on your company to provide a significant portion of your income. Add in stock comp—and suddenly, your income, your investments, and your net worth are all tied to one company. That’s a lot of eggs in one basket. Now layer on industry-specific risks like:

- Mergers & acquisitions

- Market volatility

- Internal restructures

- Leadership turnover

…and that emotional attachment to company stock? It’s no longer harmless. It could quietly derail your retirement plans if you don’t have a clear, structured strategy.

How to Know If You’re Caught in Home Stock Syndrome™

Ask yourself these questions.

- Do I know what % of my portfolio is in company stock?

- Do I have a plan for when and how to sell?

- Am I holding onto shares simply because it feels safer than letting go?

If you’re unsure about any of those, that’s a sign it’s time to pause and take a closer look.

What to Do Instead

The good news is that this is fixable. Yes, Home Stock Syndrome™ is real—and no, it’s not doing you any favors. It’s a subtle bias that can quietly lead you to make decisions (or avoid them altogether) that don’t actually serve your future. But awareness is the first step. Once you recognize the emotional grip your company stock may have on you, you can start to take action—not from fear or loyalty, but from intention.

So what now? Is there a remedy for this kind of emotional attachment? Can you actually turn this around and make smart, aligned decisions with your stock compensation?

Absolutely. It’s not about perfection—it’s about structure, clarity, and aligning your stock decisions with the life you want to live.

Here’s what you can do.

✅ Create a personalized strategy around your RSUs, stock options, and ESPPs

Without a clear structure in place, your company stock just… sits there. You’re too busy juggling everything else, and when life moves fast (a promotion, a new role, a company change), it’s easy to let it all pile up untouched—until one day, you realize you’ve been holding for years without a plan.

Your strategy doesn’t need to be complicated. Start by visualizing your future:

- When do you want to retire?

- What do you want your lifestyle to look like?

- What are you unwilling to sacrifice?

From there, reverse-engineer:

- How much do you need to set aside for short-term needs vs. long-term goals?

- How much risk can you afford to take?

- Can you truly justify keeping a large chunk in one company’s stock, or would diversifying give you a better shot at freedom and flexibility?

Think of it like a decision map. Compare two scenarios—holding vs. diversifying—and ask yourself: Which one actually supports the life I want to live?

The clearer you are about your vision, the easier it is to align your decisions with it.

✅ Understand the tax impact of exercising and selling

This one’s big—because each type of stock compensation (RSUs, options, ESPPs) comes with its own set of tax rules, and the impact can be substantial.

Most executives divest their shares without a proactive plan for timing or methodology. This lack of strategy often leads to avoidable tax surprises—or worse, missed opportunities for high-impact giving. Donating appreciated shares to charity, for instance, is one of the most underutilized strategies for simultaneously fulfilling philanthropic goals while capturing significant tax savings.

Take ESPPs, for example. The discount might look appealing, but depending on your holding period and how you sell, the tax treatment could outweigh the benefit. Just because something is “on sale” doesn’t mean it’s the right fit.

You know that feeling when you buy a jacket because it’s 40% off… and it just sits in your closet? Same idea. Let’s make sure your financial choices are actually serving you—not just collecting dust (or tax bills).

✅ Set clear thresholds for when to reduce exposure

YES—this is one of the most important steps.

Because here’s what I’ve seen time and time again: brilliant, successful women—some with millions in company stock—still feeling anxious about their financial future. Why? Because deep down, they know that if the stock drops, everything they’ve built could be at risk.

But the decision feels so overwhelming, they freeze. They wait. They tell themselves they’ll deal with it later… and then later never comes.

I don’t blame them. This stuff is complex, and emotional. But that’s why setting a threshold in advance is so powerful. It gives you a rule to follow when emotions are high, so you don’t have to keep re-deciding every time the market shifts.

And if doing it alone feels too hard? Delegate. You don’t have to go it alone.

But if you can take action—start now. Set a cap. Create a plan. Stick to it. You’ll thank yourself later.

Final Thoughts

Home Stock Syndrome™ is emotional. It’s sneaky. And it’s real. But with a little structure and support, you can break free from it—and build a wealth plan that actually works for you. Because your financial future deserves more than just hope and loyalty. It deserves intention, clarity, and confidence.

Clarity creates confidence. Let’s help you see the full picture so you can make smart, intentional decisions for your future. Want help evaluating your current stock comp strategy? Book your Align Call today to see what strategies we have used to help other professional women like you.

You May Also Like

Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

No investment strategy assures a profit or protects against loss.