How Effective Tax Planning Can Help Your Retirement Income

Written by Hazel Secco, CFP®, CDFA®

Estimated reading time: 8 minutes

Planning for taxes in retirement is not something that intuitively comes to mind when you are looking at your nest egg. People often think about their taxes when it’s time to pay them or when they are surprised by an unexpected tax bill during the tax season. However, when it’s time to pay the tax bills, it might be too late to take advantage of the available tax planning strategies.

Many people have different definitions of what tax planning is. Some advisors will say tax-loss harvesting at the end of the year is tax planning, while others might say buying tax-efficient ETFs is tax planning. What I am going to talk about today in the context of tax planning is taking a proactive approach to taxes so that you are in control of how much you pay and how much to allocate for tax bills.

Tax accountants often help you file taxes for the previous year and tell you how to reduce your tax bill during the year. They are more of a historian, while financial planners who are savvy with tax planning are strategists. In my opinion, tax planning involves modeling out lifetime taxes and adopting strategies that could reduce your taxes over time.

Table of contents

- How Effective Tax Planning Can Help Your Retirement Income

- Understanding Tax Planning

- The Historical Context of Tax Rates

- The Reality of Tax-Deferred Accounts

- Strategies for a Tax-Efficient Retirement

- Tax Planning as a Safer and More Predictable Strategy

- Planning for the Unknown

- Common Misconceptions and Risks

- The Importance of Comprehensive Retirement Planning

- Conclusion

Understanding Tax Planning

Tax planning involves looking at your financial situation comprehensively and understanding the tax implications of various decisions to minimize your tax liability over the course of your lifetime. Despite many people’s beliefs, true tax planning isn’t just about making annual contributions to a traditional IRA; it’s about creating a long-term strategy that considers your entire financial picture. This approach can also help you make a bigger impact while giving to your family or favorite charities.

The Historical Context of Tax Rates

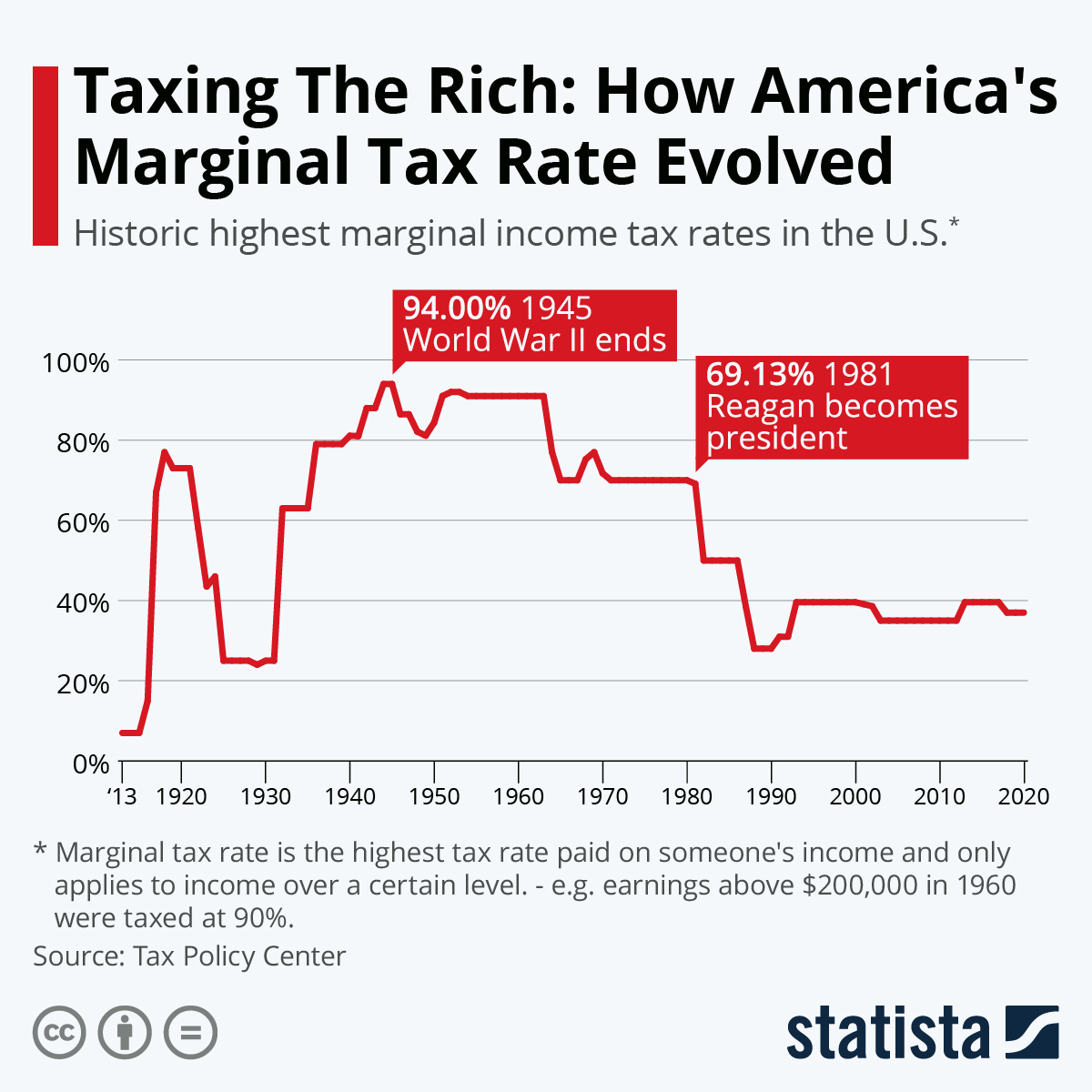

To appreciate the importance of tax planning, it helps to understand where we stand historically with tax rates. Currently, the top federal income tax rate is 37%, but it hasn’t always been this low. In the 1940s, the top marginal tax rate was as high as 94%, and it remained around 70% in the 1970s. The tax cuts enacted during the Trump administration lowered some of the tax rates, but these cuts are also set to expire at the end of 2025, which means the top rate will revert to 39.6%.

[Picture Credit: statista]

This historical context highlights the urgency of tax planning. With tax rates likely to increase in the future, the money you save in tax-deferred accounts today might be subject to higher taxes when you need it most.

The Reality of Tax-Deferred Accounts

Many people diligently save money in tax-deferred accounts like IRAs and 401(k)s, thinking they are setting themselves up for a secure retirement. Don’t get me wrong—tax-deferred accounts are amazing tools to mitigate taxes during your high-earning years. However, it’s important to make informed decisions because, without considering future tax rates, you might be in for a surprise. For example, a million dollars in your IRA today might be worth significantly less in the future once taxes are taken into account. If tax rates increase, your effective savings could be substantially reduced.

Strategies for a Tax-Efficient Retirement

Diversify Your Tax Exposure

Don’t rely solely on tax-deferred accounts. Consider contributing to Roth IRAs, which offer tax-free withdrawals in retirement, or taxable investment accounts, which might offer more flexibility. When you talk with a financial advisor, they should help determine the right mixture of different accounts to contribute to each year by modeling your financial picture and the likely scenarios for different tax rates.

Roth Conversions

If you expect to be in a higher tax bracket in the future, converting some of your traditional IRA funds to a Roth IRA now, while tax rates are low, might make sense. You’ll pay taxes on the conversion amount today, but future withdrawals will be tax-free. Approach this with caution. You don’t want to do it alone and make mistakes. After all, it’s hard-earned money saved for your future, and we want to help make sure it’s done right.

Tax-Efficient Investments

Investing in tax-efficient mutual funds or ETFs is a smart strategy to minimize capital gains distributions, thereby reducing your taxable income. These investments are designed to be more tax-friendly by employing strategies such as low turnover rates, which means they buy and sell securities less frequently, resulting in fewer taxable events. Additionally, tax-efficient funds often focus on holding stocks for longer periods to take advantage of long-term capital gains tax rates. (Long-term capital gains rates are often less than your ordinary tax rates.)

This method of tax planning is passive yet effective. Many advisors utilize this approach. However, you need to always understand its benefits and how it fits into your overall financial strategy. By minimizing the tax drag on your investment returns, you can enhance the growth potential of your portfolio over time.

Charitable Giving

If philanthropy is something you are passionate about, consider strategies like donating appreciated securities or establishing a donor-advised fund. These approaches can provide significant tax benefits while supporting causes you care about. Many people don’t know how to “give” effectively because they often donate without taking advantage of tax benefits. Why not kill two birds with one stone?

Tax-Loss Harvesting

Tax-loss harvesting is a strategy that involves selling investments at a loss to offset gains from other investments, thereby reducing your overall taxable income. This technique can be particularly effective if you know you’ll be in a higher tax bracket in a specific year or if you anticipate a significant capital gain that could elevate your tax liability.

How it works

When you sell an investment that has declined in value, you realize a capital loss. These losses can be used to offset capital gains you’ve realized from selling other investments at a profit. For instance, if you have a $10,000 gain from one investment and a $4,000 loss from another, you can offset the gain with the loss, reducing your taxable gain to $6,000.

Additionally, if your losses exceed your gains, you can use up to $3,000 to offset other income (wages or salary). Any remaining losses can be carried forward indefinitely, allowing you to use them to offset gains in future years.

Things to consider

This strategy requires careful planning and timing. For example, the wash-sale rule prohibits you from repurchasing the same or substantially identical security within 30 days before or after the sale. Hence, you need to understand the rule if you want to claim the loss for tax purposes. Violating this rule can disqualify the loss, negating the benefits of tax-loss harvesting.

Tax-loss harvesting is more than just a year-end activity. It can be a year-round strategy, especially in volatile markets where frequent adjustments might be necessary. It’s essential to maintain a diversified portfolio and ensure that the moves you make for tax purposes don’t compromise your overall investment strategy.

How your financial planner can help

Working closely with your financial advisor can help you navigate the complexities of tax-loss harvesting. They can provide the expertise to identify suitable opportunities, execute transactions in compliance with IRS rules, and integrate this strategy into your broader financial plan.

The goal is to reduce your tax burden while keeping your investment portfolio aligned with your long-term objectives, ultimately maximizing your after-tax returns. It’s all about collaboration and communication. Discuss with a financial advisor to determine the best strategy for you and your family’s future.

Tax Planning as a Safer and More Predictable Strategy

Tax planning might be one of the least risky and most predictable ways of helping grow your assets by not losing extra money to the IRS. Investment inherently has risks, especially when it’s more growth-oriented. Tax planning, on the other hand, can provide a more stable foundation for your financial future. It might be controversial to some, but I believe it’s the most important aspect of financial planning and often the most overlooked.

Planning for the Unknown

The future of tax rates is uncertain, but that doesn’t mean you can’t plan for it. By diversifying your tax exposure and considering various scenarios, you can create a more resilient retirement plan. This approach can help you save a substantial amount of money over your lifetime.

Common Misconceptions and Risks

One common misconception is that maxing out contributions to tax-deferred accounts is always the best strategy. However, this isn’t necessarily true for everyone. Depending on future tax rates and your personal circumstances, other strategies might be more beneficial.

The Importance of Comprehensive Retirement Planning

Retirement is too important to leave to chance. A comprehensive retirement plan considers not just your savings but also how you’ll withdraw and use those funds. The way you withdraw money from your accounts can significantly impact your tax liability and overall financial health.

Conclusion

Tax planning for retirement is about more than just maximizing annual contributions. It’s about creating a long-term strategy that minimizes your tax burden and helps you work towards your financial goals. By implementing these strategies and considering the impact of taxes on your retirement savings, you can make more informed decisions and enjoy a more fulfilling retirement.

If you found this information helpful, consider working with a financial advisor to develop a tax-efficient retirement plan tailored to your needs.

Learn more about what it’s like working with a financial planner who specializes in women nearing retirement. You can schedule an intro call or contact us to arrange a consultation. Let’s work together to ensure you have a solid plan in place for a tax-efficient retirement.

And don’t forget to subscribe to our YouTube channel for more tips and updates on achieving financial freedom!

Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. We suggest that you discuss your specific tax issues with a qualified tax advisor.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

No investment strategy assures a profit or protects against loss.