Written by Hazel Secco, CFP® CDFA®

Estimated reading time: 9 minutes

Table of contents

- What an IPO Changes for Employees with Stock Options and RSUs

- How Stock Options, RSUs, and Shares Are Treated in an IPO

- Lockups, Blackouts, and Trading Windows

- IPO Tax Implications: Stock Options, RSUs, and Capital Gains

- Turning Paper Wealth into a Concrete Strategy

- Working with a Financial Advisor on Post-IPO Equity Decisions

- Relevant Blog Posts

If your company is heading toward an Initial Public Offering (IPO), it’s hard not to think about what that could mean for you. The equity that’s been sitting in the background of your compensation package is suddenly front and center—and potentially worth real money.

That shift can feel exciting, but it also raises a lot of questions. When can you sell? How much will you get to keep after taxes? And what decisions matter most in those first few months after the company goes public?

This topic can be dense, but a little preparation can save you a lot of time and anxiety if your company goes public. Let’s walk through what typically happens to options, Restricted Stock Units (RSUs), and shares during an IPO, what to expect with lockups and trading windows, and how to think through the tax and planning decisions that come with it.

As a CFP® who works with women navigating complex portfolios, I walk clients through these decisions regularly. Here’s what I tell them.

What an IPO Changes for Employees with Stock Options and RSUs

When your company goes public, its shares begin trading on a public stock exchange. From that point on, the company must follow stricter reporting and disclosure rules, and everything around your equity becomes more structured.

For you, that usually means a few important shifts:

- You finally have a clear, real-time value for your equity based on the public stock price.

- Your vested shares may become liquid, giving you a path to turn equity into cash, though timing is still controlled by lockups and trading windows.

- The rules tighten, so you should expect more formal policies around when you can trade, along with blackout periods and stricter compliance requirements.

Before the IPO, your equity was mostly on paper. You could see an estimated value, but there wasn’t a simple way to turn it into cash.

After the IPO, that changes. There’s now a real market for your shares, so selling becomes possible, but only within specific rules and timeframes you’ll need to follow.

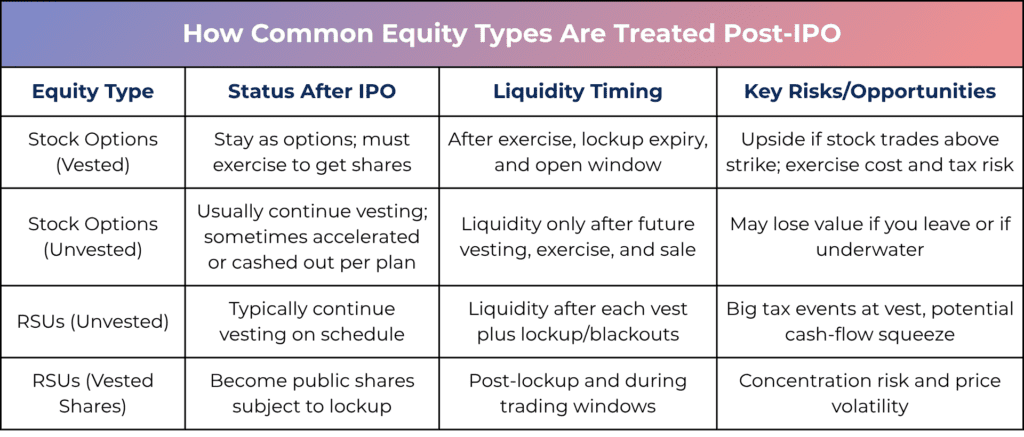

How Stock Options, RSUs, and Shares Are Treated in an IPO

The specifics of what happens when your employer goes public depend on your plan and the company’s IPO details. However, many follow a similar pattern.

Here’s how the main types typically work.

Stock Options (ISOs and NSOs)

Stock options give you the right to buy shares at a set price for a certain period of time. After the IPO, a few key things happen:

- Vested options stay as options. They don’t automatically turn into shares. Instead, you decide if and when to exercise, and whether to sell the shares later.

- Unvested options usually continue vesting on the same schedule. In some cases, companies may accelerate vesting, cash them out, or convert them to new awards, but that depends on the plan.

- Incentive Stock Options (ISOs) can qualify for lower long-term capital gains tax rates if you meet holding requirements, but exercising and holding them can trigger alternative minimum tax (AMT).

- Nonqualified Stock Options (NSOs) are typically taxed when you exercise based on the difference between your strike price and the current market price. Any additional gain after that may be taxed at capital gains rates if you hold the shares.

Many employees choose to take a simple approach with NSOs by exercising and selling at the same time to cover taxes and avoid taking on too much risk. ISOs, on the other hand, tend to require more careful planning because of how AMT can come into play.

Restricted Stock Units (RSUs)

RSUs are a promise to grant you shares of company stock in the future, usually once you meet certain vesting conditions. After an IPO, here’s how they typically play out:

- Time-based RSUs continue vesting on schedule. When they vest, you receive shares, but you may still need to wait to sell based on lockups and trading windows.

- Double-trigger RSUs (common at pre-IPO companies) require both time-based vesting and a liquidity event like an IPO. Once both happen, shares are released and taxed, often all at once.

- Taxes can add up quickly. When RSUs vest, the value of those shares is treated as ordinary income based on the stock price at that time. Companies usually withhold some shares or cash for taxes, but it may not be enough to cover what you ultimately owe.

One thing that often catches people off guard is timing. Keep in mind that you can owe taxes when your shares vest, even if you haven’t sold anything yet. If the stock price is volatile after the IPO, that can lead to large tax bills based on a high stock price at vest, even if you sell later at a lower price or haven’t sold the shares yet.

Already Owned Shares

If you already own shares, whether from early option exercises, restricted stock, or a tender offer, those shares simply become stock in the newly public company. It’s important to note:

- You likely won’t be able to sell right away. Many employees are subject to a lockup period, often 90 to 180 days, where sales are restricted.

- After the lockup ends, you can usually sell during open trading windows, as long as you follow insider trading rules and any required pre-clearance.

Here’s the bottom line: while you may already own the shares, turning them into cash depends on timing and the company’s trading rules.

Lockups, Blackouts, and Trading Windows

After an IPO, one of the biggest surprises for employees with equity compensation is that “public” doesn’t mean you can sell right away. In reality, there are a few sets of rules that control when you’re actually allowed to trade.

IPO Lockup Period

Most IPOs come with a lockup period that prevents employees and insiders from selling shares for a set amount of time after the company goes public.

- Lockups usually last 90 to 180 days, though the exact timing can vary based on your role and the structure of the deal.

- Some companies use staggered or alternative lockups, especially with direct listings or Special Purpose Acquisition Company (SPAC) mergers.

The reason for the lockup period is to keep too many shares from hitting the market at once, which could push the stock price down.

Ongoing Blackout Periods

Even after the lockup ends, you may not have full flexibility. Public companies set blackout periods when employees can’t trade, usually around earnings or major announcements. Here’s what to know:

- These blackout periods happen several times a year.

- Some employees, especially at more senior levels, also need pre-clearance before placing trades.

This means you may only have a few windows of opportunity each year when you’re allowed to sell. That makes timing and planning more important than most people expect.

10b5-1 Trading Plans

To make things more predictable and ensure compliance with blackout periods and insider trading rules, many employees set up a 10b5-1 trading plan. This lets you schedule trades in advance at a time when you’re not holding any inside information.

Once the 10b5-1 plan is in place, trades happen automatically based on the rules you set, as long as they follow company policies and regulations. This approach helps create consistency and reduces the pressure of trying to time everything perfectly within a limited number of trading windows.

IPO Tax Implications: Stock Options, RSUs, and Capital Gains

When your employer goes public, the IPO itself usually doesn’t create a tax bill. What matters more is what happens after the IPO and when it happens.

Here’s where taxes typically come into play:

- NSO exercises: When you exercise, the difference between your strike price and the current stock price is taxed as ordinary income. If you hold the shares after that, any additional gain or loss depends on when you sell.

- ISO exercises: Exercising and holding can trigger alternative minimum tax (AMT). If you meet the required holding periods, you may qualify for long-term capital gains treatment when you sell.

- RSU vesting: When RSUs vest, the value of those shares is treated as ordinary income based on the stock price at that time. Your company will usually withhold some shares for taxes, but it may not cover the full amount you owe.

- Selling shares: When you sell, you’ll have a capital gain or loss based on your cost and how long you’ve held the shares.

It’s important to note that a higher stock price after the IPO can turn routine vesting or exercises into a much larger tax bill than expected. By taking a closer look at the potential tax consequences before those events happen, you can make more informed decisions and avoid surprises.

Turning Paper Wealth into a Concrete Strategy

Once an IPO is in sight or already behind you, the conversation around your equity changes. Before, the focus was on potential. Now it’s about what to do with it. You’re deciding when to sell, how much to keep, and how it fits into the rest of your financial life.

Here are a few practical steps to help you make practical and informed decisions with your equity:

- Start by getting organized. List out each grant you have, including the type (ISOs, NSOs, RSUs, restricted stock), vesting schedule, strike price, and expiration dates. If you have double-trigger RSUs (RSUs that vest only after a time-based vesting requirement and a liquidity event such as an IPO), note those details too.

- Know your timing. Look at when your lockup ends, when trading windows are likely to open, and whether you’ll need pre-clearance or a 10b5-1 plan to sell.

- Get ahead of taxes. Map out what exercising options or RSU vesting could look like at different stock prices so you’re not making emotional or snap decisions in the moment.

- Decide how much is “enough”. Think about how much company stock you’re comfortable holding versus selling. This helps you avoid Home Stock Syndrome™, or staying overconcentrated longer than you should.

- Tie it back to real goals. Whether it’s paying down debt, buying a home, or building long-term investments, give your equity a goal so your decisions aren’t driven by short-term price swings.

Working with a Financial Advisor on Post-IPO Equity Decisions

An IPO can create real financial opportunity, but it also introduces a new level of complexity. Timing, taxes, and concentration risk all start to overlap, and the decisions you make early on can shape your long-term outcome.

You don’t have to sort through it alone. Working with a financial advisor who understands equity compensation can help you evaluate your options, run the numbers, and make decisions that align with your broader goals.

Consider working with a fee-only fiduciary financial advisor if you have six figures or more in equity compensation, you’re not sure how exercising or selling affects your tax picture, you’re within 10 to 15 years of retirement and need your equity to be part of a broader income plan, or you’re holding concentrated stock and aren’t sure how much is too much.

At Align Financial Solutions, I help women in their 40s and 50s turn complex equity positions into part of a clear, tax-efficient retirement plan. If your company is going public and you want to understand how it fits into your bigger financial picture, schedule a complimentary 15-minute Align Call to get started.