Author: Hazel Secco, CFP®, CDFA®

Estimated reading time: 8 minutes

🎧 Prefer to watch or listen? This episode of Align Your Retirement covers exactly this:

Table of contents

Why does a widow usually pay more in taxes than she did when her husband was alive, on the exact same income? Most people have no idea this even happens until it does.

It’s called the widow’s penalty, and for most married women it isn’t a question of if it hits, but when. The encouraging part is that it’s a predictable, solvable problem, as long as you plan for it while both spouses are still alive.

This guide walks through what the widow’s penalty is, why the same income suddenly costs more, a real-world example, and the strategies that can soften or even erase the impact.

Prefer to listen? I walk through the widow’s penalty and the Roth conversion math in this episode of the podcast.

What is the widow’s penalty?

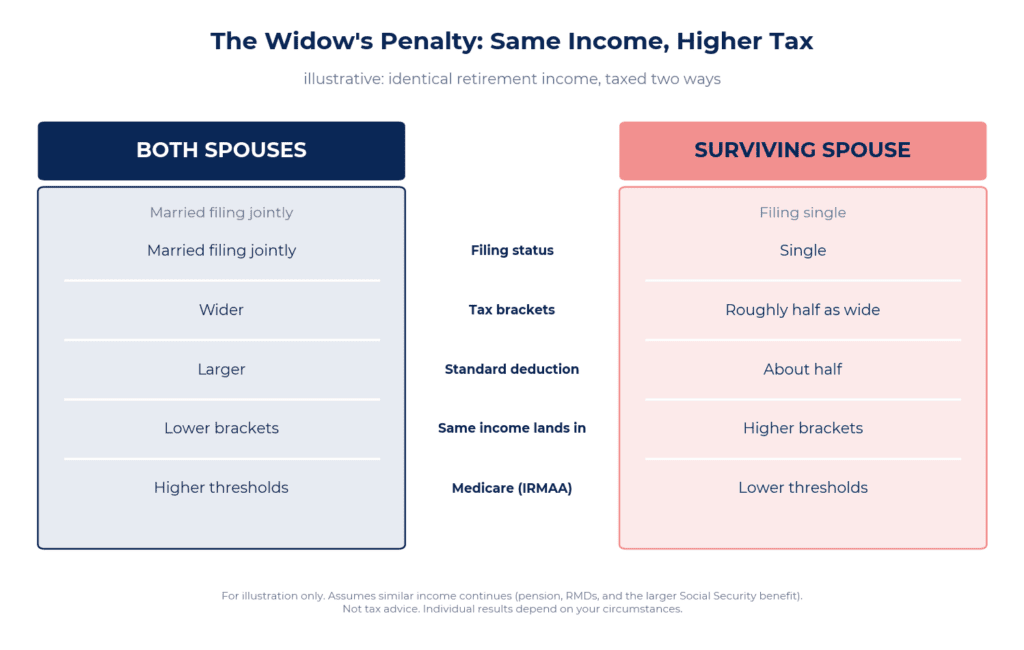

The widow’s penalty is the higher tax bill a surviving spouse faces when they go from filing jointly to filing as a single taxpayer on nearly the same income.

For the year a spouse passes away, the survivor can typically still file a joint return. Starting the following year, though, they usually file as single, which changes everything about how their income is taxed.

Single tax brackets are roughly half as wide as the married brackets, and the standard deduction is about half as large. So the same income gets squeezed into a narrower, less forgiving structure, and more of it is taxed at higher rates.

One nuance: if the survivor still has a dependent child at home, they may qualify to use joint brackets for a couple more years as a qualifying surviving spouse. For most couples in or near retirement, though, that doesn’t apply, and single-filer status arrives quickly.

Why does the same income suddenly cost more?

Because the income barely drops while the brackets shrink around it.

When one spouse dies, most of the household’s income keeps flowing. Pensions continue. Required minimum distributions from retirement accounts continue. And Social Security keeps paying the larger of the couple’s two benefits, while only the smaller one goes away.

So the survivor often lands with nearly the same income, now filtered through single brackets that are half as wide. Same lifestyle, same money coming in, higher tax bill.

Because women statistically outlive their husbands, this penalty can stretch across a decade or more, not a single year. And it doesn’t stop at income tax.

Those narrower single thresholds can also push a survivor over the income lines that trigger higher Medicare premiums, known as IRMAA surcharges. The result is a one-two punch: more income tax and higher healthcare costs, both landing at the same time.

A real-world example: Diane and Paul

Let’s make this concrete with a hypothetical couple. Diane and Paul aren’t real clients, but their situation is common.

Diane is 59 and Paul is 62, and together they’ve saved about $2.1 million. What matters most here is that $1.45 million of it sits in traditional, pre-tax retirement accounts. Every dollar they eventually withdraw will be taxed as ordinary income.

Right now, filing jointly, their income sits comfortably in a moderate bracket. But picture the statistically likely path: Paul passes away in his late 70s, and Diane lives into her 90s.

Diane’s income barely changes. The pension continues, the required distributions from that $1.45 million continue, and she keeps the larger Social Security check. But now she files as a single taxpayer, and that nearly identical income fills up the much narrower single brackets.

Over the years she spends on her own, the extra tax can add up to six figures. Not because her lifestyle grew, but because the tax structure around her income shrank.

How can you reduce the widow’s penalty?

The core idea is to move income out of the future single-bracket years and into the present, while the wide married brackets are still available.

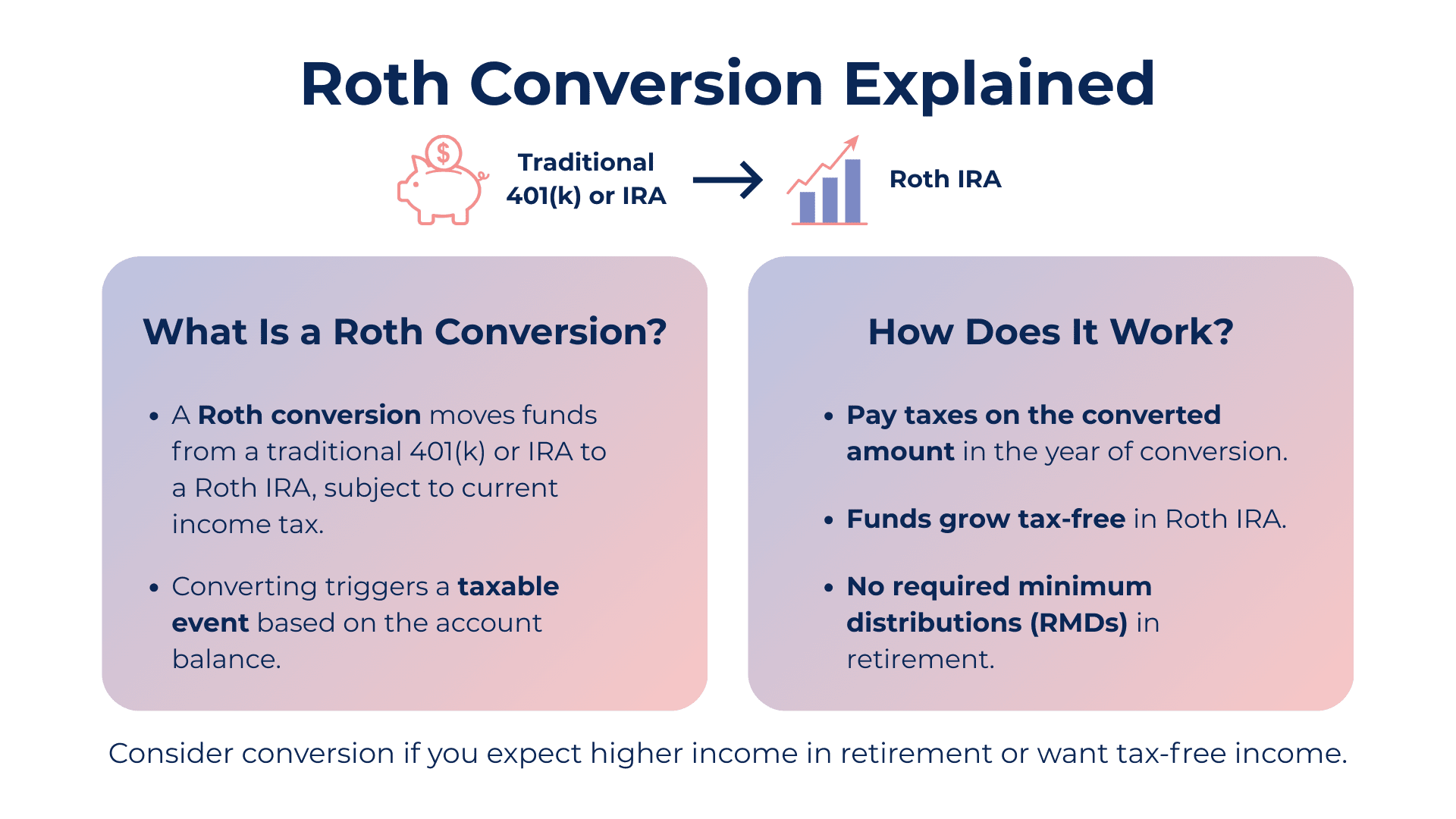

The most powerful tool for doing that is the Roth conversion.

{kind=link}

Use Roth conversions during the married years

While both spouses are alive, you can convert a portion of your traditional retirement accounts to a Roth each year, paying tax on the amount you convert at today’s married rates.

The trick is to convert only up to the top of a target bracket, so you fill the wide married brackets deliberately rather than spilling into a higher one. Do this over a series of years, and a meaningful share of the savings ends up in the Roth.

That matters later for two reasons. Money in a Roth is never taxed again, and a Roth IRA has no required minimum distributions for the original owner. So by the time Diane is on her own, she has a large pool of tax-free money to draw from and a smaller pre-tax balance forcing out taxable distributions. Her taxable income as a single filer drops, and the penalty shrinks with it.

Weigh the trade-off honestly

A conversion isn’t free. You pay tax today, which reduces the portfolio’s value in the moment, and that can feel counterintuitive.

So this isn’t about winning a tax-bracket game. It’s about deciding whether to pay a known, often lower tax now to protect the spouse who will face the single brackets for possibly a decade or more.

Where possible, it’s usually best to pay the conversion tax from a taxable account rather than from the retirement money itself, so the full converted amount keeps growing tax-free. That single choice can make a real difference in how well the strategy works.

Don’t overlook the other levers

Roth conversions get the spotlight, but they’re not the only move. Coordinating the order you draw from taxable, tax-deferred, and Roth accounts can keep taxable income smoother across both the married and single years.

Once you’re old enough, qualified charitable distributions can satisfy part of your required distributions while keeping that money off your tax return entirely. Life insurance can provide tax-free liquidity to help the survivor absorb the higher future tax bill. And reviewing beneficiary designations and account titling alongside your estate plan makes sure the accounts actually pass the way you intend.

None of these replaces the conversion strategy. Together, though, they give a survivor more room to breathe.

When does a Roth conversion make sense, and when not?

It comes down to the gap between your bracket as a couple today and the survivor’s likely bracket alone in the future.

The strategy tends to shine when you have large pre-tax balances, you’re sitting in a moderate bracket now, and you expect sizable required distributions down the road, exactly the setup Diane and Paul have.

It’s less compelling if you’re already in the top bracket today with no expectation of a higher one later, if you plan to leave most of the pre-tax money to charity (which would receive it tax-free anyway), or if you don’t have outside cash to cover the conversion tax.

You may have heard about finding your Roth conversion break-even point, the age at which the upfront tax pays off. I dig into that in the episode linked above, and the short version is that it’s a useful number but not the whole story. The widow’s penalty is one of the big reasons why: the break-even math changes once you account for the survivor facing single brackets for years. That’s why this decision deserves a look at your specific numbers, not a rule of thumb.

The bottom line

The widow’s penalty is one of the more predictable challenges in retirement, and one of the most overlooked. The same income, taxed as a single filer, simply costs more, often for a decade or more, and it can raise Medicare costs on top of that.

The good news bears repeating: it’s solvable when you plan ahead. The years when both spouses are alive are a window to use the wide married brackets on purpose, and that window doesn’t stay open forever.

If you’d like to see where you stand, I offer a complimentary retirement readiness assessment, and if you’re ready to go deeper, we can get on a short call and run the conversion math for your own situation, so the decision rests on your numbers rather than a general guideline. Retirement is too important to wing, and this is exactly the kind of planning we do at Align Financial Solutions.

Frequently Asked Questions

It’s the higher tax bill a surviving spouse faces after a spouse dies, when they shift from filing jointly to filing as a single taxpayer on nearly the same income. Single brackets are roughly half as wide as married brackets, so more of that income is taxed at higher rates.

Often, yes. Pensions and required distributions continue, and the survivor keeps the larger of the couple’s two Social Security benefits while the smaller one stops. Income may dip modestly, but rarely enough to offset the jump to single brackets.

It can last for the rest of the survivor’s life. Because women tend to outlive their husbands, that’s frequently a decade or more of paying more tax on the same income.

It can. The narrower single-filer income thresholds can push a survivor over the lines that trigger higher Medicare Part B and Part D premiums, known as IRMAA surcharges, adding to the overall cost.

No. Conversions work best when you have large pre-tax balances, a moderate current bracket, and outside cash to pay the tax. They’re less useful if you’re already in the top bracket with no future increase expected, or if you plan to leave the money to charity. The right answer depends on your specific numbers.

Disclosures

This article is for educational purposes only and should not be considered legal, tax, or financial advice. Tax rules, brackets, Social Security provisions, and Medicare premium thresholds change over time and depend on your individual circumstances and filing status.

The example is hypothetical and simplified. Roth conversions have important trade-offs and are not suitable for everyone. Always consult a qualified tax professional and your financial advisor regarding your specific situation before acting on any strategy described here.