Key Points:

- State taxes on equity compensation can create unexpected tax bills, especially in high-tax states or if you’ve moved during the vesting period.

- RSUs and stock options are often under-withheld at the state level, which can lead to underpayment penalties if you don’t proactively manage it.

- Multiple states may tax the same equity income based on where you worked between grant and vest, not just where you live now.

- Making timely estimated payments and coordinating multi-state tax credits can reduce stress, avoid penalties, and prevent overpaying.

Table of contents

- Why State Taxes Matter with Equity Compensation

- State Taxes with Equity Compensation: The Big Picture

- A General Playbook for Paying State Estimated Taxes

- How to Pay State Estimated Taxes in California (CA)

- How to Pay State Estimated Taxes in New York (NY)

- How to Pay State Estimated Taxes in New Jersey (NJ)

- A Smarter Way to Stay Ahead of State Taxes on Equity Compensation

If a meaningful part of your income comes from RSUs or stock options and you live in a high-tax state, your state tax bill can sneak up on you just as easily as your federal one. I see this all the time, especially for people in places like California, New York, or New Jersey, or for those who’ve moved while their equity was vesting and don’t realize multiple states may be involved.

At a high level, state estimated taxes work the same way as federal estimated taxes: the state expects you to pay as you go throughout the year. And just like with federal taxes, things start to get tricky with equity compensation. Large vesting events or option exercises often aren’t withheld at a high enough rate, which can leave you underpaid and subject to penalties without realizing it.

One of the simplest ways to stay ahead of this is by making estimated tax payments at the state level, just like you would federally. If you do this consistently, you can avoid scrambling at tax time and keep your cash flow more predictable.

Here’s how this works in practice, with a closer look at what to expect if you live in California, New York, or New Jersey.

Why State Taxes Matter with Equity Compensation

If you’re a high earner with RSUs, stock options, or an ESPP, you probably already feel the weight of federal taxes. What tends to catch people off guard is how much state taxes can add to this, especially if you live in a high-tax state like California, New York, or New Jersey.

In many cases, state taxes are even harder to manage than federal taxes. Here’s where things start to get complicated:

- High-tax states like California, New York, and New Jersey have top rates in the 10% to 13%+ range, which can take a meaningful bite out of equity income.

- Employers usually withhold state tax on RSUs at a flat supplemental rate that can be lower than your actual bracket, which could mean you’re underpaying without realizing it.

- If you’ve lived or worked in more than one state while your equity was vesting, multiple states may claim a portion of that income.

This is how people often end up with a surprise tax bill in April and why having a clear, repeatable approach to managing state estimated taxes is essential.

State Taxes with Equity Compensation: The Big Picture

At the federal level, taxes are pretty straightforward: the IRS looks at your total income for the year versus how much you’ve already paid in through withholding and estimated payments. State taxes are a little different, because states care less about where you live today and more about where you earned the income.

With equity compensation, that distinction matters. Many states use what’s called a “grant-to-vest” or “grant-to-exercise” approach to figure out how much of your income they can tax.

Here’s how it works:

- States look at the time between when your equity was granted and when it vests or is exercised.

- They track where you were physically working during that period.

- They tax the portion of income tied to the days you worked in their state, even if you no longer live there.

This is where a lot of confusion comes in. For instance, you could be thinking, “I left New York years ago, why am I still paying taxes there?” The answer is that the income didn’t just appear at vesting. You actually earned a portion of it while working in that state, and they’re claiming their share based on that timeline.

A General Playbook for Paying State Estimated Taxes

If you live in a state with income tax, it’s smart to have a simple, repeatable system for handling estimated payments. This is even more important when you have equity compensation, since what you owe can shift quickly and get complicated fast.

Here’s a practical approach you can follow no matter where you live:

#1: Identify which states can tax your equity.

- List where you lived and worked between grant and vest or exercise for each award.

- Keep in mind if you’ve moved during that time, more than one state may claim a portion of the same income.

#2: Understand how each state sources equity income.

- Many states use a workday allocation from grant to vest or exercise.

- States like California and New York often claim income based on where it was earned, even if you no longer live there. Here’s a basic example of how this might work:

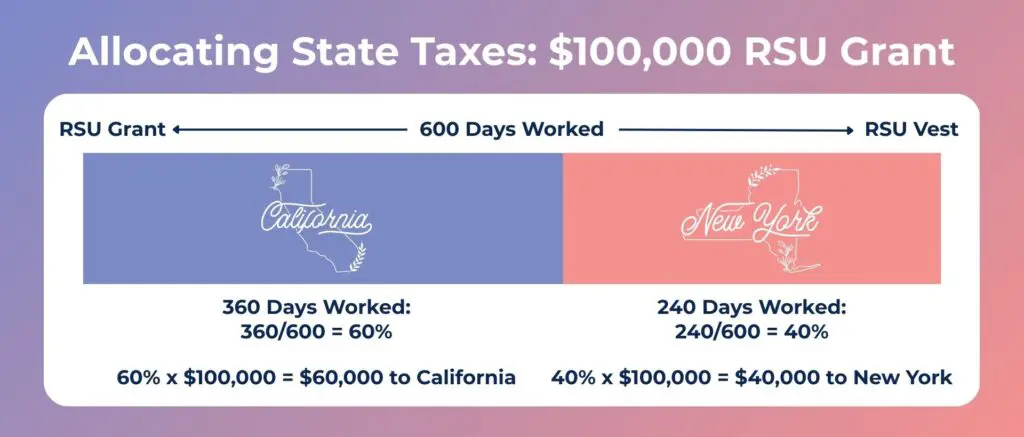

Suppose you received an RSU grant while you were working in California, and it vests three years later after you’ve moved to New York.

Over those three years, you worked 600 total days between grant and vest. Of those 600 days, 360 were in California (60% of the workdays) and 240 were in New York (40% of the workdays).

If the RSU grant is worth $100,000 when it vests, California and New York will each tax the portion of that income that you “earned” while you worked there. In this case, California would tax $60,000 (60% x $100,000), and New York would tax $40,000 (40% x $100,000).

Even though you no longer live in California by the time the shares vest, it still gets to tax its 60% slice because that’s where you earned most of the grant.

#3: Project your state income, not just your federal.

- Start with your federal income, then adjust for each state’s rules.

- Apply that state’s tax brackets and any surtaxes, especially in higher-income ranges.

#4: Compare what you’ll owe to what’s being withheld.

- Look at your pay stubs and equity event confirmations to see what’s already been paid in.

- Then estimate what will be withheld for the rest of the year, including upcoming vesting or exercises.

#5: Check safe harbor and timing rules.

- Many states follow federal-style safe harbor rules, while some have their own variations.

- California, for example, requires a larger portion of taxes to be paid earlier in the year, which can create issues in equity-heavy years.

#6: Decide how to close the gap.

- You may be able to increase state withholding through payroll.

- If not, you’ll need to make estimated payments directly through the state’s system.

#7: Track credits to avoid double taxation.

- When multiple states tax the same income, your home state may offer a credit for taxes paid elsewhere.

- Missing this step can lead to overpaying or triggering penalties.

Once you have a high-level framework like this in place, the state-specific rules become much easier to manage. Let’s take a closer look at how to pay estimated taxes in California, New York, and New Jersey.

How to Pay State Estimated Taxes in California (CA)

The first thing to know is that California taxes residents on worldwide income and nonresidents on CA‑source income, including equity earned for CA workdays between grant and vest/exercise.

This means if you lived or worked in CA during a vesting period, CA may claim part of your RSU, NSO, ISO or ESPP income using a time‑based allocation. Combine that with some of the highest marginal rates in the country, and big equity events can lead to very large tax bills.

CA Estimated Tax and Safe Harbor Rules

You can often avoid California underpayment penalties by paying the lesser of:

- 90% of current year’s CA tax, or

- 100% of prior year’s CA tax (110% if your AGI exceeds $150,000).

Once your CA AGI exceeds $1,000,000, you generally must use the 90% current‑year method.

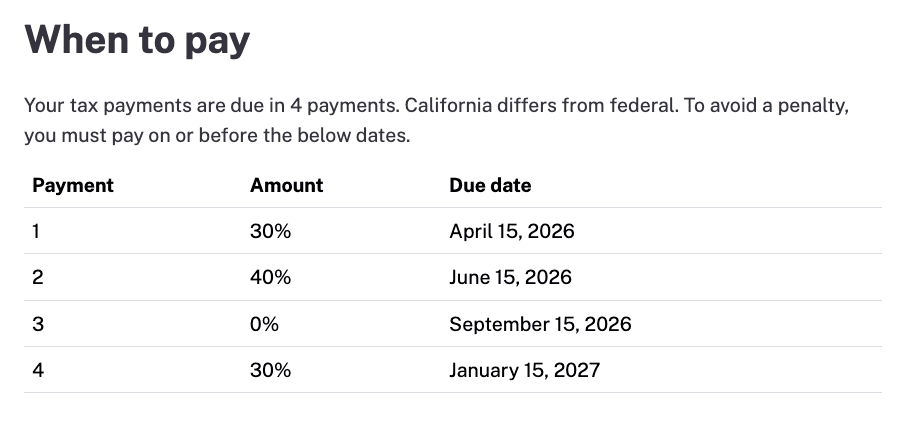

When to Pay California Estimated Taxes

California effectively requires a front‑loaded payment pattern:

- Roughly 70% of the required safe‑harbor amount must be paid in by the June estimate deadline to avoid penalties, especially under the current‑year method.

- Penalties are assessed quarter by quarter, so a big catch‑up payment in January can’t fix a shortfall that existed at the June checkpoint.

Source: State of California Franchise Tax Board

This timing requirement can be a major trap in equity‑heavy years if a big vest or exercise hits early and you don’t adjust estimates until late.

Step-by-Step Payment Instructions

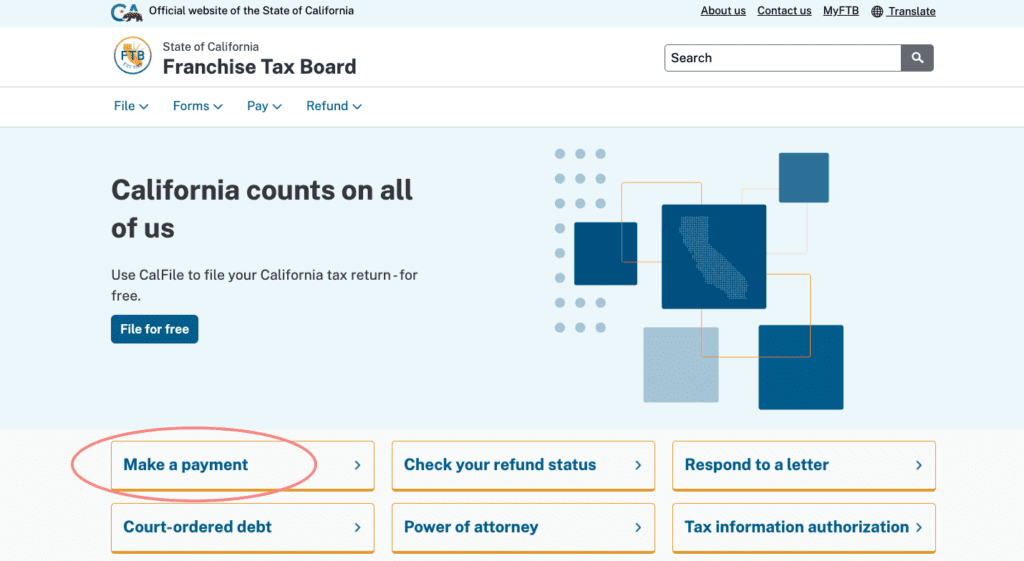

1. To make California estimated tax payments, go to the State of California Franchise Tax Board’s home page and select “Make a Payment.”

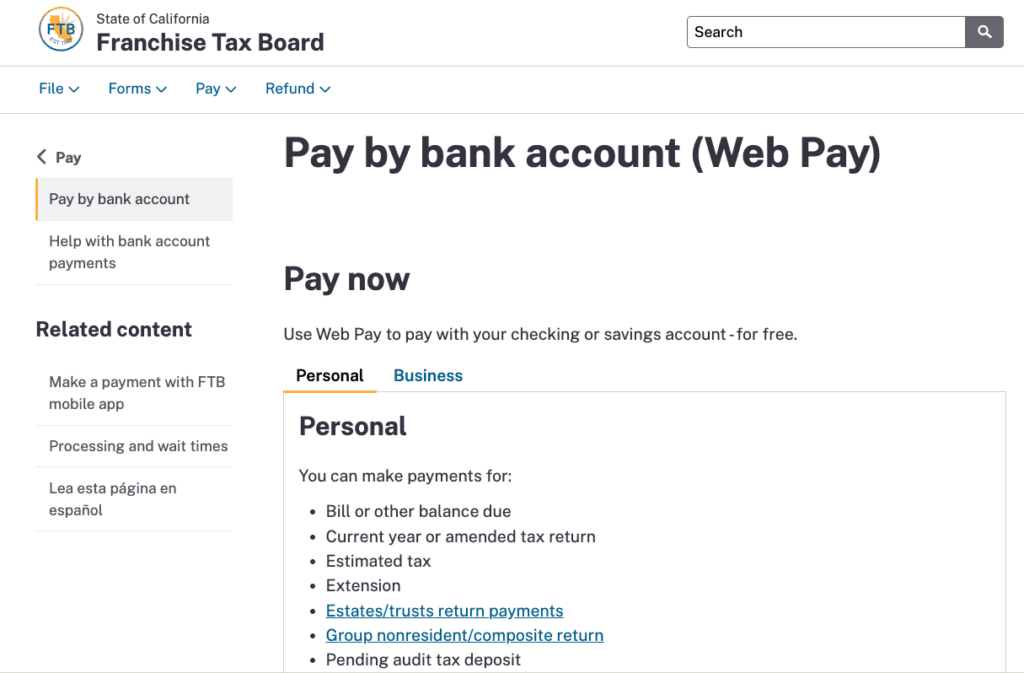

2. On the next page, select “Bank account.”

Here’s where you’ll pay your personal estimated taxes.

- If you have a MyFTB account, enter your User Name and Password and click Login.

- If you’re new, click “Register for MyFTB” and follow the prompts to create an account using your SSN and prior-year CA return information.

3. Once you’re logged in, select “Estimated Tax” as the payment type.

4. Select the tax year and quarter of your estimated tax payment.

5. Enter your bank account (routing number and account number), your payment amount, and your desired payment date.

6. Review and submit. Be sure to save your confirmation number for your records.

How to Pay State Estimated Taxes in New York (NY)

New York is famously aggressive about taxing equity compensation, including when you’ve moved.

For nonresidents and those who have moved, New York uses a workday allocation similar to California’s from grant to vest/exercise for many equity awards. This means if you spent a large part of the vesting period working in NY (even if you’ve since moved), NY will tax a corresponding portion of that RSU/option income.

Your new state of residence may also tax the same income, so be sure to keep an eye on this and take advantage of available credits to avoid double taxation.

New York Estimated Tax and Safe Harbor Rules

You can typically avoid New York underpayment penalties by paying the lesser of:

- 90% of the tax shown on your current year’s NY return, or

- 100% of the tax shown on the prior year’s NY return (110% of that amount if your NY AGI exceeds $150,000).

If you realize that you underpaid or paid your estimated tax late, New York requires you to calculate the amount of your penalty using Form IT-2105.9 and submit it with your state tax return.

Note: If you’re a resident of New York City, don’t forget to account for the NYC resident tax in your estimates.

When to Pay New York Estimated Taxes

New York’s estimated tax payment due dates mirror federal deadlines:

- 1st payment: April 15

- 2nd payment: June 15

- 3rd payment: September 15

- 4th payment: January 15

Step-by-Step Payment Instructions

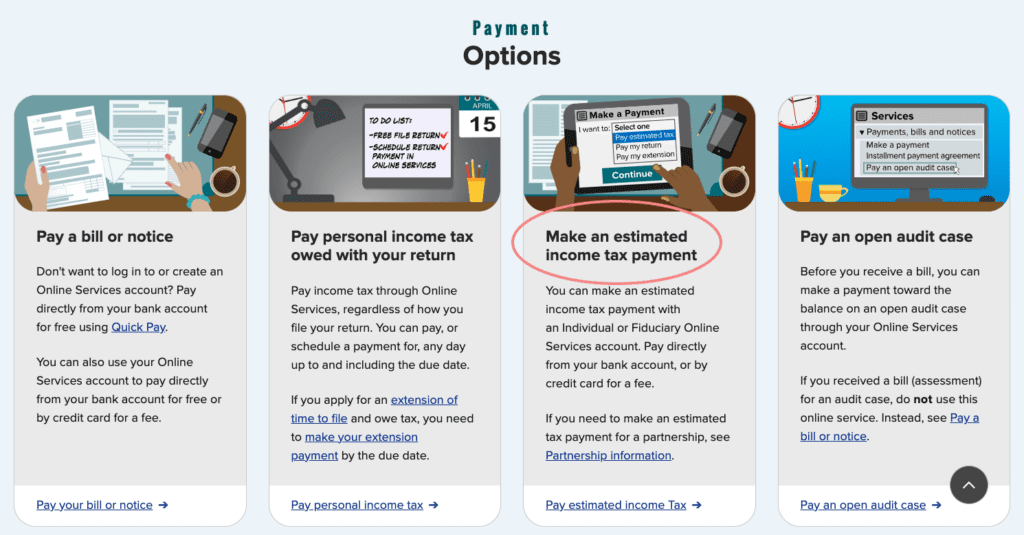

1. To pay your New York estimated tax, go to the NY Department of Taxation and Finance Make a Payment page.

2. Scroll down to Payment Options and select “Pay estimated income tax” under “Make an estimated income tax payment.”

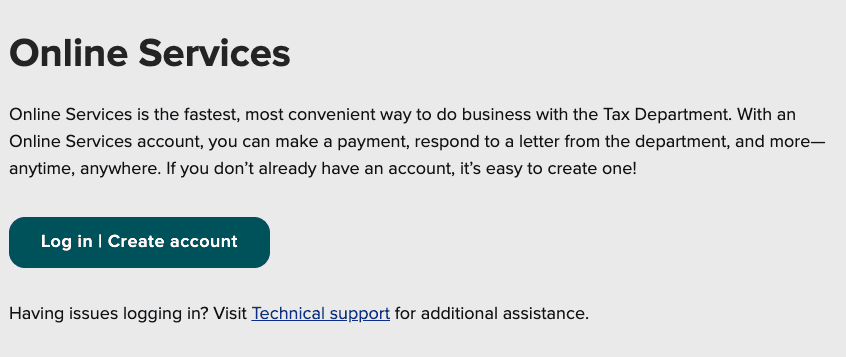

3. To pay through your Online Services account, click “Log in | Create account.” Log in with your username and password.

If you don’t have an account, click “Create account.” You’ll need your Social Security Number and information from a previously filed NY return to verify your identity.

4. Once you’re logged in to your Online Services account, click “Make a Payment.”

5. Select “Estimated Tax Payment” from the payment type options. Make sure you select the correct tax year for the estimated payment.

6. Enter the amounts for: NY State tax, NYC tax (if you’re a city resident), and any other applicable taxes.

7. Click “Calculate” to verify the total.

8. Enter your bank account information, choose your payment date (on or before the quarterly due date), and submit. Be sure to save your confirmation number for your records.

How to Pay State Estimated Taxes in New Jersey (NJ)

Like California and New York,New Jersey taxes RSU, stock option, and ESPP income to the extent it’s sourced to New Jersey workdays between grant and vest/exercise. Your equity income becomes New Jersey gross income at the taxable event (vest, exercise, or sale, depending on the award) and may require estimated payments if under‑withheld.

Because employers often withhold NJ tax based purely on where you currently live/work and not the historical grant‑to‑vest sourcing, your NJ withholding can be off in either direction if you’ve moved.

New Jersey Estimated Tax and Safe Harbor Rules

You can typically avoid New Jersey underpayment penalties by paying the lesser of:

- 80% of your current year’s NJ tax liability, or

- 100% of the prior year’s NJ tax liability.

When to Pay New Jersey Estimated Taxes

New Jersey’s estimated tax payment due dates mirror federal deadlines:

- 1st payment: April 15

- 2nd payment: June 15

- 3rd payment: September 15

- 4th payment: January 15

New Jersey allows you to pay your estimated tax in full by the first due date (April 15) or in four equal installments throughout the year.

Step-by-Step Payment Instructions

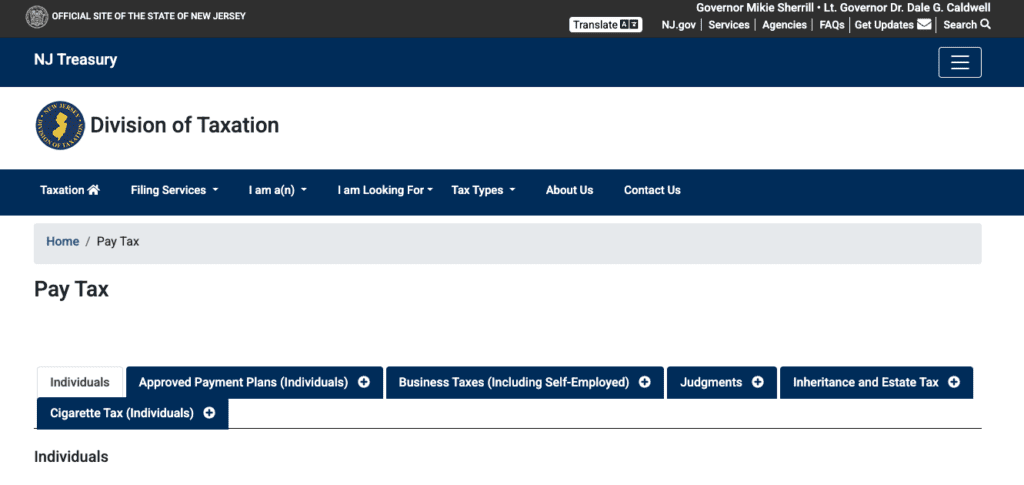

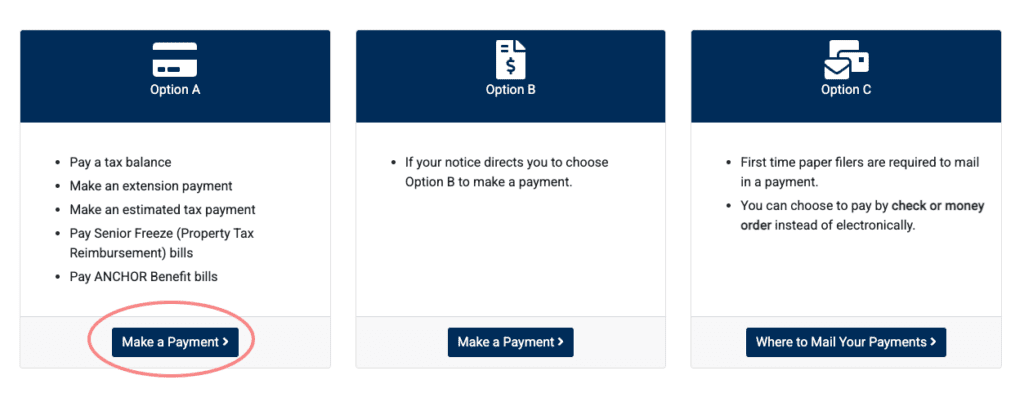

1. To pay your New Jersey estimated taxes, go to the NJ Division of Taxation Pay Tax page.

2. Scroll down and select “Make a Payment” under “Option A.”

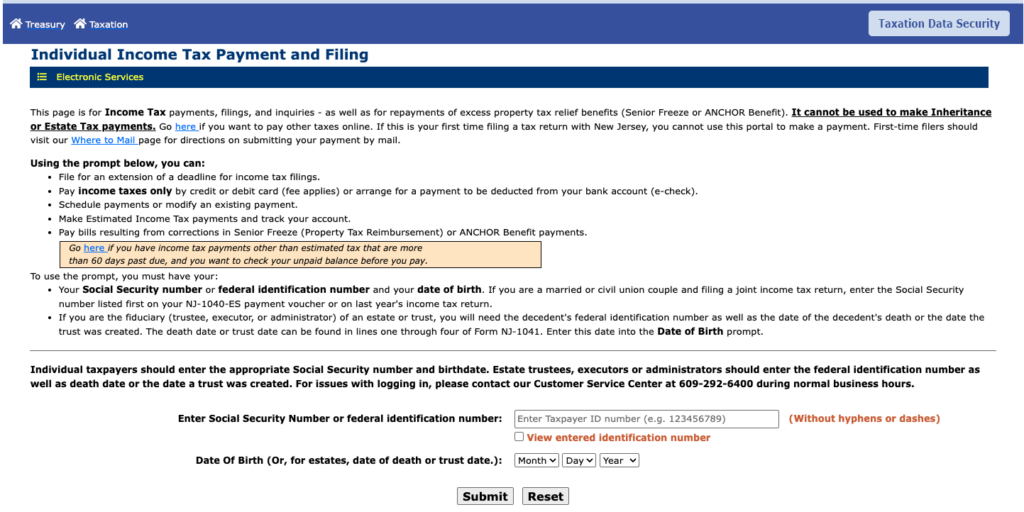

3. On the next page, enter your Social Security number and date of birth, then click “Submit.”

Note: If you’ve never filed a NJ tax return before, you can’t use this online portal yet. You’ll have to mail in a check with a Form NJ-1040-ES voucher until your first return is filed and processed.

4. Once you’re logged in, select “Estimated Payments – Schedule/Submit NJ-1040-ES.”

5. Choose whether to schedule a single payment for the current quarter or schedule all four quarterly payments at once for the full year.

6. Select the quarter you’re paying for, enter your payment amount, choose your payment method, and enter your bank account information.

7. Click “Submit” and save your confirmation number for your records.

A Smarter Way to Stay Ahead of State Taxes on Equity Compensation

State taxes on equity compensation are manageable, but only if you’re proactive. The complexity tends to build quietly, especially if you’ve moved during the vesting period or have income tied to multiple states. Without a system, it’s easy to fall behind, underestimate what you owe, or pay more than necessary.

A clear, repeatable approach puts you back in control. It helps you stay current throughout the year, avoid penalties, and make smarter decisions about withholding, estimated payments, and multi-state coordination. More importantly, it removes the stress of wondering what’s coming at tax time.

You don’t have to piece this together on your own. At Align Financial Solutions, we help you make sense of equity compensation and taxes so you can focus on what actually moves your financial life forward. If you want a plan that works in real life, not just on paper, book a 15-minute Align Call to see how we can support your goals.