Key Points

- Equity compensation like RSUs and stock options can create large bursts of taxable income that often aren’t fully covered by standard employer withholding, which can lead to unexpected tax bills.

- The IRS requires taxes to be paid throughout the year through withholding or estimated payments, and failing to keep up can result in underpayment penalties.

- A simple framework that includes projecting income, estimating taxes, comparing against withholding, and using safe harbor rules can help you determine how much to pay in quarterly estimated taxes.

Table of contents

- Why Equity Compensation Often Creates Tax Surprises

- The IRS Cares When You Pay, Not Just How Much

- First, Understand How Your Equity Compensation Is Taxed

- Estimating Your Quarterly Tax Payments: A Simple Framework

- When to Pay Estimated Taxes

- How to Pay Quarterly Estimated Taxes: Step-by-Step Instructions

- A Smarter Way to Stay Ahead of Taxes on Equity Compensation

If you earn a high income and part of your pay comes through restricted stock units (RSUs) or other equity awards, tax season can get messy fast. Equity income can quietly push you into higher tax brackets while your employer continues withholding at a flat rate that may be well below your actual tax rate. The result is a gap between what’s withheld and what you ultimately owe, which can lead to an unpleasant surprise in April and even potential penalties.

Paying quarterly estimated taxes during the year is one of the most effective ways to avoid these surprises. The payments themselves are simple to make. The real challenge is figuring out how much to send.

That’s where having a repeatable process helps. To make it easier, I’ve outlined how federal estimated taxes work when you have equity compensation, how the IRS safe harbor rules fit in, and a practical step-by-step approach you can follow each year to stay ahead of your potential tax liability. Let’s dive in.

Why Equity Compensation Often Creates Tax Surprises

On paper, RSUs and other equity awards look like a great deal. The company grants you stock, the vesting dates feel far away, and it all shows up in your portal as part of your total compensation package.

In reality, those shares often create large bursts of income that hit only a few times a year. And because the withholding tied to those events is usually too low, the amount withheld at vesting often doesn’t keep pace with the taxes you’ll actually owe for the year.

Here’s why that matters:

- RSUs and non-qualified stock options (NSOs) exercises are treated as ordinary income when they vest or when you exercise.

- Most employers treat this income as “supplemental wages” and withhold federal tax at a flat 22% up to $1 million of supplemental income, then 37% above that.

- If your marginal federal tax rate is actually 32%–37%, that 22% withholding on much of your equity income can leave a sizable gap between what’s paid in and what you ultimately owe.

That gap is what shows up in April as: “How could I possibly owe this much when I’ve been paying taxes all year?” If this sounds familiar, you’re not alone. Many people run into this at least once.

The good news is there are a few ways to close the gap, so tax time doesn’t come as such a shock. And for many high earners, one of the simplest approaches is making quarterly estimated tax payments.

The IRS Cares When You Pay, Not Just How Much

The U.S. tax system requires you to pay taxes as you earn income throughout the year. This is known as the “pay-as-you-go” system, which means even if you ultimately pay the correct amount when you file your return, you can still face penalties if you didn’t send enough to the IRS during the year.

Most people meet this requirement through a combination of paycheck withholding and estimated tax payments. But when your income fluctuates because of bonuses or equity vesting events, it can be difficult to know how much you should be paying each quarter.

This matters because when you pay too little along the way, the IRS typically assesses an underpayment penalty. As of the first quarter of 2026, the current penalty rate is 7% per year, compounded daily. Depending on how much you owe, an innocent mistake can quickly turn into an expensive lesson.

Fortunately, you can avoid federal underpayment penalties if you meet one of the IRS “safe harbor” thresholds:

- You pay at least 90% of your total tax for the current year, or

- You pay 100% of last year’s total tax (110% if your adjusted gross income is above a certain threshold), or

- After all withholding and payments, you owe less than $1,000.

High earners with equity compensation tend to follow one of two approaches:

- “Prior year safe harbor” – aim to pay 110% of last year’s tax, even if this year’s income will be higher.

- “Current year safe harbor” – aim to pay at least 90% of this year’s projected tax and adjust as your equity income unfolds.

Once you choose your target, the next step is deciding how much to cover through W-2 withholding and how much to send through quarterly estimated payments.

First, Understand How Your Equity Compensation Is Taxed

Before you can estimate how much tax you may owe, it helps to understand when your equity actually becomes taxable. Many people assume they only owe taxes when they sell stock, but with equity compensation, that’s often not the case. In many situations, the taxable income shows up earlier, sometimes before you’ve sold a single share.

You don’t need to become a tax expert, but it’s helpful to know which events create ordinary income, which may trigger capital gains, and which can involve the alternative minimum tax (AMT). If your equity is administered through a brokerage platform, it will often show estimated taxable income for each vesting or exercise event. That information can be helpful when projecting how much additional income your equity may generate during the year.

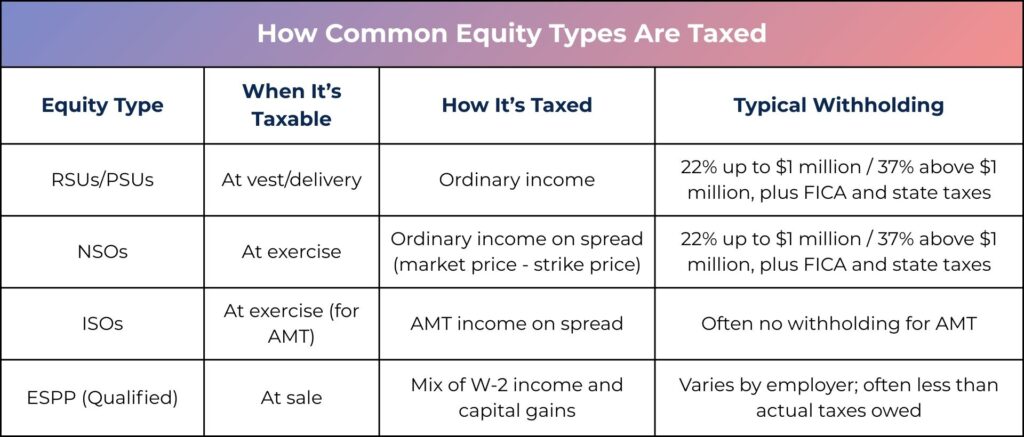

Here’s a high-level tax breakdown for the most common types of equity compensation:

Restricted Stock Units (RSUs) / Performance Share Units (PSUs)

- Taxable event: When the shares vest and hit your account.

- Tax treatment: The fair market value of the shares at vest is treated as ordinary income and reported on your W-2.

- Typical withholding: 22% federal up to $1 million of supplemental wages, then 37% above that, plus FICA and state taxes.

Nonqualified Stock Options (NSOs)

- Taxable event: When you exercise the option.

- Tax treatment: The “spread” between the market price and the strike price is treated as ordinary income.

- Typical withholding: The same supplemental wage rules as RSUs, which often results in under-withholding for high earners.

Incentive Stock Options (ISOs)

- Regular tax: Exercising an ISO does not create ordinary income for regular tax purposes. If you sell too soon (a disqualifying disposition), part of the gain may show up as W-2 income later.

- AMT: The spread at exercise counts as income under the alternative minimum tax system, which can trigger a separate tax calculation and sometimes a sizable additional liability.

Employee Stock Purchase Plans (ESPPs)

- Taxable events: Both the purchase and the eventual sale of the shares matter.

- Tax treatment: The purchase discount and part of the gain may be treated as W-2 income, while the remaining gain may be taxed as a capital gain.

- Typical withholding: Varies by employer and often isn’t enough to fully cover the tax bill for high-income households that regularly sell ESPP shares.

A Note on Federal Tax Rates

For high earners, long-term capital gains are often taxed at a lower rate than ordinary income. While long-term capital gains typically fall in the 15% or 20% range, ordinary income for high earners can be 30% or more once federal and other taxes are included.

That difference matters. If you hold shares for at least one year after they vest or after you exercise options, any additional gain may qualify for the lower long-term capital gains rate.

It’s also important to keep the alternative minimum tax (AMT)) in mind, particularly if you have incentive stock options. Exercising ISOs can trigger AMT even if you don’t sell the shares, which can create a larger tax bill than expected.

If you’re concerned about AMT or want help thinking through the timing of exercises and sales, working with a financial planner who understands equity compensation can help you make more informed decisions and avoid surprises.

Estimating Your Quarterly Tax Payments: A Simple Framework

You don’t need a complicated spreadsheet to stay ahead of quarterly estimated tax payments. Here’s a simple process you can revisit a few times throughout the year to avoid unpleasant surprises in April and sidestep potentially costly penalties.

Step #1: Estimate Your Full-Year Income

Start with your base salary and bonus, then add in any income you expect from RSUs, stock options, ESPP sales, or other equity events. Don’t forget to include other household income too, such as a spouse’s pay, business income, rental income, or investment income. The goal is to get a realistic idea of how much total income may show up on your tax return.

Estimated Ordinary Income = Base Salary + Bonus + Equity Income + Other Household Income

Step #2: Estimate Your Total Federal Tax

Once you have an income estimate, the next step is estimating what your federal tax bill may look like. That includes ordinary income tax on wages and equity income, plus any capital gains tax or AMT if those apply. This gives you a rough target for what needs to be paid in over the course of the year.

A simple way to think about it:

Total Estimated Tax ≈

Tax on your ordinary income (salary, bonuses, RSUs, option exercises)

+ Tax on long-term capital gains from stock sales

+ Any additional taxes that may apply, such as Net Investment Income Tax or AMT

Step #3: Confirm What’s Already Being Paid In

Next, look at how much tax is already being withheld from your paycheck and from any equity events. Then compare that number to your projected total tax bill. If there’s a gap, that’s the amount you may need to cover through additional withholding or estimated tax payments.

Estimated Tax Shortfall = Total Estimated Tax – Total Projected Withholding

Step #4: Choose Your Safe Harbor Target

From there, decide which IRS safe harbor you want to use to avoid underpayment penalties. Some high earners aim to pay 110% of last year’s tax to avoid penalties, especially if this year’s income is unusually high. Others aim to cover at least 90% of this year’s projected tax so they stay more current as the year unfolds.

Safe Harbor Payment = Max [(90% x Current Year Tax), (110% x Last Year’s Tax)]

Step #5: Cover the Shortfall

Once you know how much more needs to be paid in, you have two main options: increase withholding through your paycheck or make quarterly estimated tax payments. Many people use a mix of both. For example, you might increase paycheck withholding a bit and then make larger estimated payments after major vesting events.

Additional Tax Payment = Safe Harbor Target – Projected Withholding

Step #6: Revisit After Big Equity Events

This isn’t something to calculate once in January and ignore for the rest of the year. Be sure to revisit your numbers after big events like a large RSU vest, option exercise, or major stock sale. Equity income can change quickly, and checking in along the way helps you adjust before a tax surprise has time to build.

When to Pay Estimated Taxes

Federal estimated taxes are typically due four times a year, though the deadlines don’t line up perfectly with calendar quarters. Payments are generally due on the 15th of the month unless that date falls on a weekend or holiday.

- April 15 (Q1: income from Jan 1–Mar 31)

- June 15 (Q2: income from Apr 1–May 31)

- September 15 (Q3: income from Jun 1–Aug 31)

- January 15 of the following year (Q4: income from Sep 1–Dec 31)

If a large portion of your equity income shows up during certain months, you can often time larger estimated payments around those events. For example, if most of your RSUs vest in March and September, you may choose to make larger payments in the April and September cycles, so each period has enough tax paid in.

There are a few ways to make these payments:

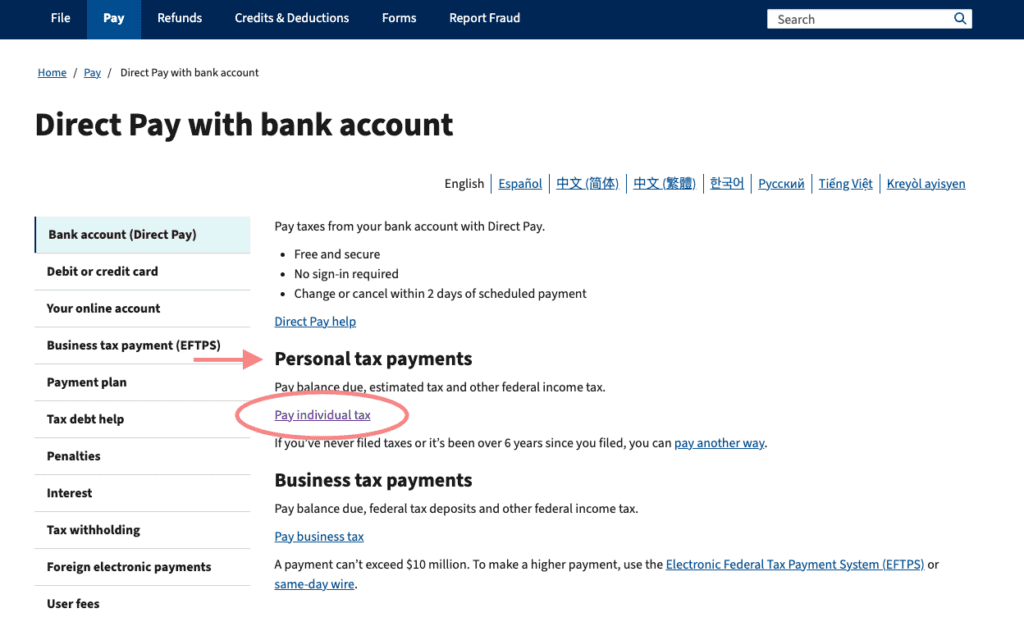

- Online using IRS Direct Pay from your bank account

- Through the Electronic Federal Tax Payment System (EFTPS)

- By mailing a check with Form 1040-ES vouchers

Let’s walk through how each payment method works.

How to Pay Quarterly Estimated Taxes: Step-by-Step Instructions

Make Quarterly Payments Online Using IRS Direct Pay from Your Bank Account

1. Go to IRS Direct Pay and choose Pay Individual Tax –> Make a Payment.

Note: For most people, Direct Pay is the most efficient way to pay quarterly estimated taxes because it’s free, secure, and doesn’t require you to create an account.

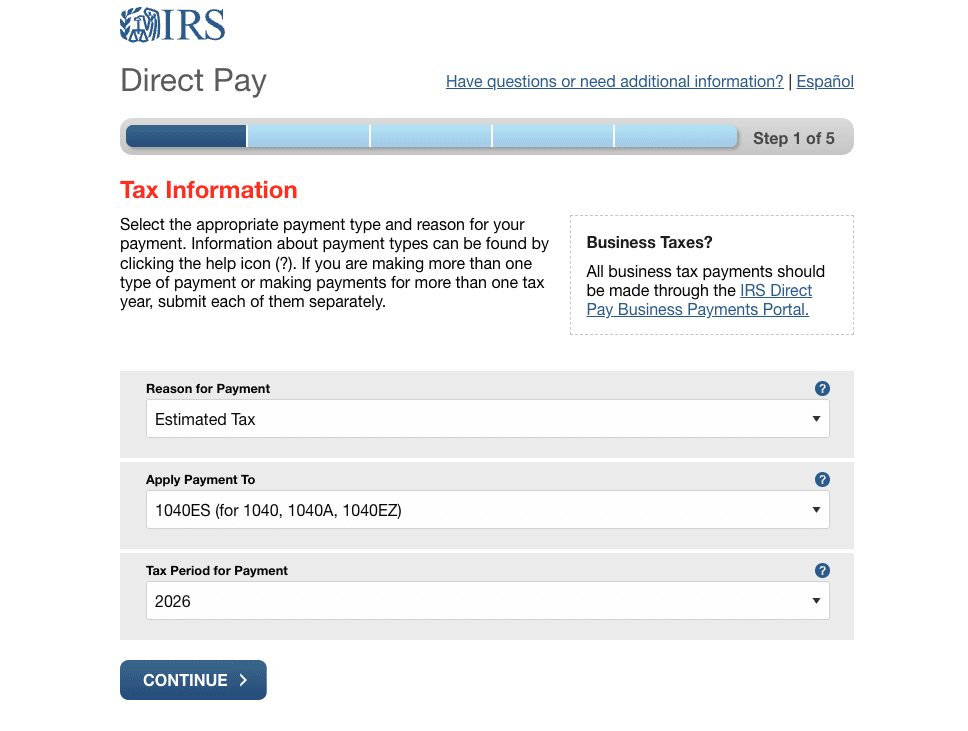

2. Under “Reason for Payment,” select Estimated Tax. Then choose 1040ES (for 1040, 1040A, 1040EZ) and the correct tax year so your payment is applied properly. Hit Continue when you’re ready.

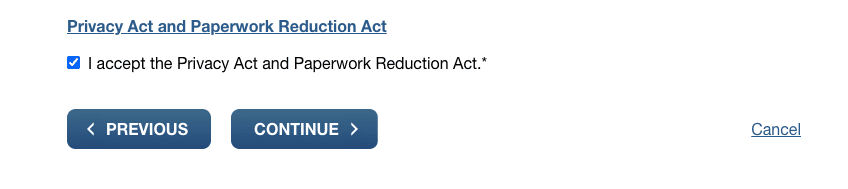

3. On the next page, verify your identity using information from a previously filed tax return. If you recently moved or got married and changed your name, make sure the information you enter matches your previous tax return, even if it’s no longer current. Accept the Privacy Act and Paperwork Reduction Act and hit continue when you’re ready to move on.

4. Next, enter your bank account information, payment amount, and payment date. Keep in mind you can make the payment immediately or schedule it for a future date.

5. Finally, review everything carefully and submit the payment. Save the confirmation number or request an emailed confirmation and be sure to file this with your other tax documents, as you’ll need a record of your estimated payments when you prepare your annual tax return. If necessary, you can look up, change, or cancel a scheduled Direct Pay payment up to two business days before the payment date.

Make Quarterly Payments Through the Electronic Federal Tax Payment System (EFTPS)

1. Enroll in EFTPS if you haven’t used it before. If you already have a Login.gov or ID.me account, you can use either one to verify your identity and access EFTPS.

Note: In most cases, Direct Pay is sufficient to pay your estimated taxes quickly and securely. However, EFTPS can be useful if you want to schedule multiple payments far in advance.

2. Once enrolled, log in to your EFTPS account.

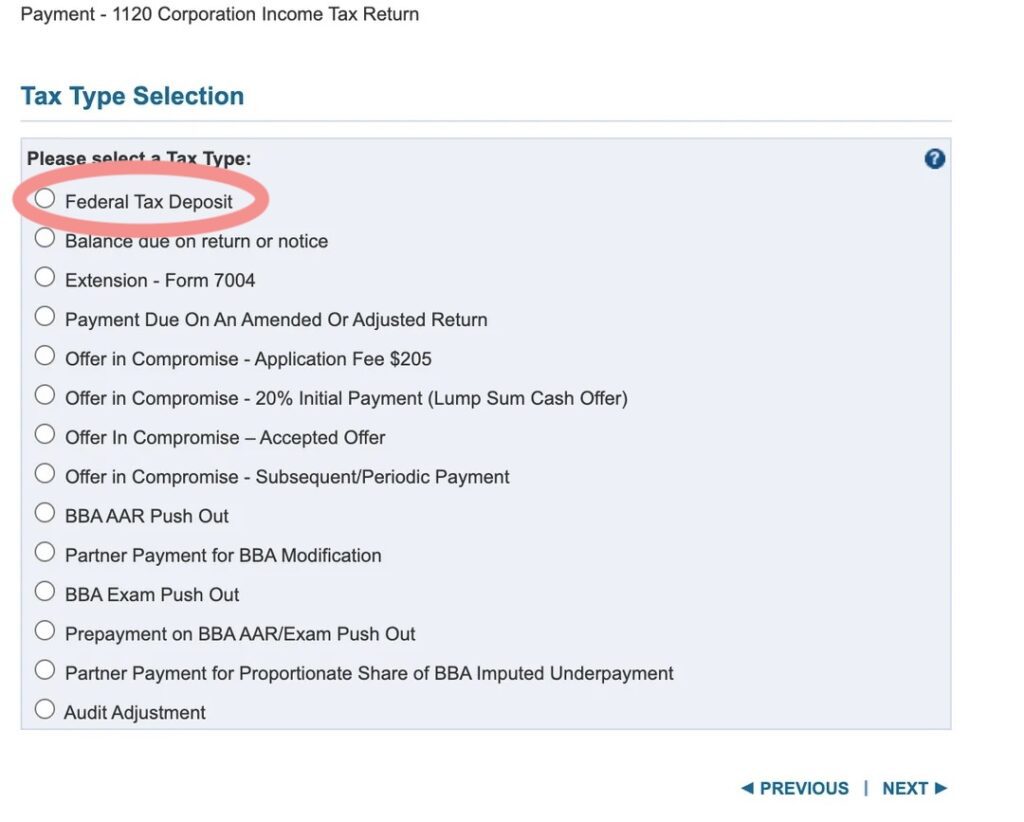

3. Select “Federal Tax Deposit” –> Next. This is the option to make an estimated tax payment. On the following page, verify the correct tax year.

4. Enter the payment amount and the date you want the IRS to pull the funds from your bank account. EFTPS allows scheduling up to 365 days in advance.

5. Lastly, review the payment details and submit. Keep the confirmation for your records and payment tracking. EFTPS also provides email notifications and payment history.

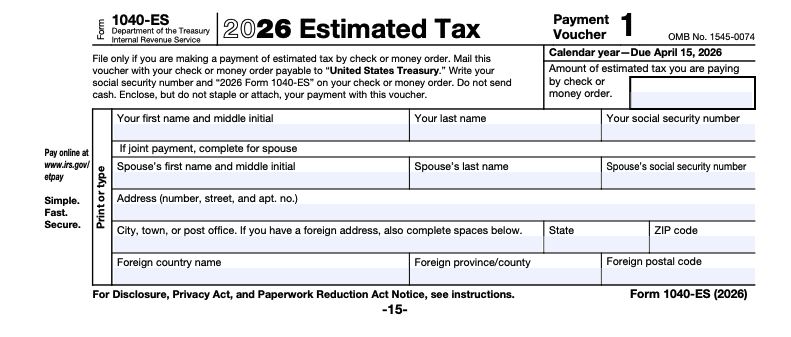

Make Quarterly Payments by Mailing a Check with Form 1040-ES Vouchers

1. Download the current Form 1040-ES for the tax year you’re paying. This form includes payment vouchers and instructions for estimated taxes.

Note: Some people still prefer to mail tax payments so they can hold onto their money as long as possible. That’s fine, but keep in mind that the risk of identity theft and fraud tends to increase with mailed payments. In fact, the Bureau of the Fiscal Service notes that paper checks are “over 16 times more likely to get lost, stolen, altered, or delayed.”

2. Complete the appropriate payment voucher for the quarter you’re paying. Make sure the voucher and payment reflect the correct tax year.

3. Write a check, money order, or cashier’s check payable to U.S. Treasury. Do not send cash.

4. On the payment, include your name, address, daytime phone number, and the tax year the payment is for. Don’t staple or paperclip your payment to the voucher.

5. Mail the voucher and payment to the correct IRS address for Form 1040-ES. The mailing address depends on where you live, and the IRS publishes those addresses separately.

6. Finally, be sure to mail your estimated payment early enough to arrive by the deadline, as the U.S. Postal Service is no longer guaranteeing a same-day postmark.

A Smarter Way to Stay Ahead of Taxes on Equity Compensation

No one loves paying taxes, but having a clear, repeatable system can take a lot of the stress out of estimating and paying them throughout the year. When you have a process for projecting your income, estimating your tax liability, and closing the gap between what’s withheld and what you actually owe, tax season becomes a lot more predictable.

Making estimated payments isn’t complicated. The harder part is figuring out how much to send, especially when your income includes equity compensation, bonuses, or multiple income streams. A thoughtful plan can help you stay compliant, avoid penalties, and make more confident decisions about when to exercise options or sell shares.

And you don’t have to figure it all out on your own. At Align Financial Solutions, our goal is to simplify complex financial decisions so you can move forward with confidence, without the jargon or mansplaining. If you’d like help building a strategy around your equity compensation and taxes, book a 15-minute Align Call to see how we can support your goals.