Written by Hazel Secco, CFP®, CDFA®

Estimated reading time: 13 minutes

Table of contents

Key Points

- Meta RSUs can be a significant part of compensation, and understanding how they work sets the foundation for better decisions.

- Proactive planning helps manage taxes, limit overconcentration in Meta stock, and decide how much to hold versus sell.

- A rules-based selling plan removes emotion and keeps RSU decisions aligned with real-life goals and diversification.

- Used intentionally, RSUs can become a powerful long-term wealth-building tool, especially with experienced guidance.

If you work at Meta, a meaningful portion of your compensation likely comes in the form of restricted stock units (RSUs). For many people, it’s one of the largest and most impactful parts of their pay.

RSUs have the potential to do a lot of good for you financially, but they’re often explained quickly, handed off, and left for you to “figure out later,” which can make them feel more complicated than they need to be.

But here’s the good news: once you see how your RSUs fit into the rest of your financial life, they stop feeling abstract and start feeling useful. You’ll be able to make intentional decisions, manage taxes more thoughtfully, and avoid tying too much of your financial future to a single stock.

In this guide, we’ll walk through how Meta RSUs really work, how they connect to the rest of your finances, and how to make decisions that actually serve you. It might not be the most exciting thing on your to-do list, but spending a little time getting this right can pay off in a big way as you head into 2026.

Understanding Your Meta RSUs

If you work at Meta, your RSUs can end up being one of the most valuable parts of your compensation, especially with how the stock has performed in recent years. Depending on your role, they may even make up a large share of what you’re earning overall, which is why they’re worth a little attention beyond “they’ll vest when they vest.”

RSUs are shares of Meta stock (NASDAQ: META) that you receive over time. Meta grants you a specific number of units, and as you meet the vesting requirements, those units turn into shares that you can hold or sell. That vesting timeline is the part that creates both opportunity and complexity.

Most Meta RSU grants vest over four years, with 25% vesting each year in quarterly increments. However, your exact schedule can look different if you’re dealing with a new-hire package or a promotion grant, so be sure to check the specifics of your equity plan.

The reason this matters is simple: vesting creates a steady stream of value, and that can play a powerful role in your financial plan. It also comes with tax implications that can catch people off guard.

In the sections ahead, we’ll walk through a practical way to think about your Meta RSUs so they support your goals and give you more control over this part of your compensation.

How to Make the Most of Your Meta RSUs

Step 1: Know How They Work

Meta RSUs are granted as a dollar-based equity award, not a fixed number of shares. That dollar amount converts to shares using Meta’s average stock price around your start date or grant date, typically the average closing price over the month before your first day.

For example, if your offer includes a $150,000 RSU grant and Meta’s average share price used for the grant is $300, your grant consists of 500 RSUs. That share count is what vests over time.

Vesting is where things start to vary. Meta uses three different vesting schedules, commonly referred to as Schedule A, B, and C. For each schedule, the first vest occurs on the first Meta vesting date after your date of hire. Meta’s standard vesting dates are February 15, May 15, August 15, and November 15.

From there, the pace depends on your schedule:

- Schedule A: 1/16 of your RSUs vest each quarter over four years.

- Schedule B: 1/12 vests in the first quarter, 1/16 in the next two quarters, and 2/48 in the final quarter.

- Schedule C: 5/48 vests in the first quarter, 1/16 in most quarters after that, and 1/48 in the final quarter.

Each time your Meta RSUs vest, the value of those shares is treated as W-2 income, similar to a bonus, and shows up on a separate $0 RSU pay stub in Workday.

Step 2: Manage the Tax Hit Proactively

This is where RSUs tend to create the most frustration, usually because the tax impact shows up after the fact.

When your RSUs vest, the full value of those shares is treated as ordinary income and taxed at the federal, state, Social Security, and Medicare level. Federal withholding follows the IRS’s supplemental wage rules, which for most people means a withholding rate of 22%. (If you make more than $1 million, the withholding rate increases to 37%.)

Meta typically handles this through a “sell to cover” process. When your shares vest, they sell enough shares on your behalf to cover estimated taxes and then deposit the remaining shares into your brokerage account. For many high earners, the default withholding doesn’t fully cover their true tax bill, which is how RSUs end up creating surprises at tax time.

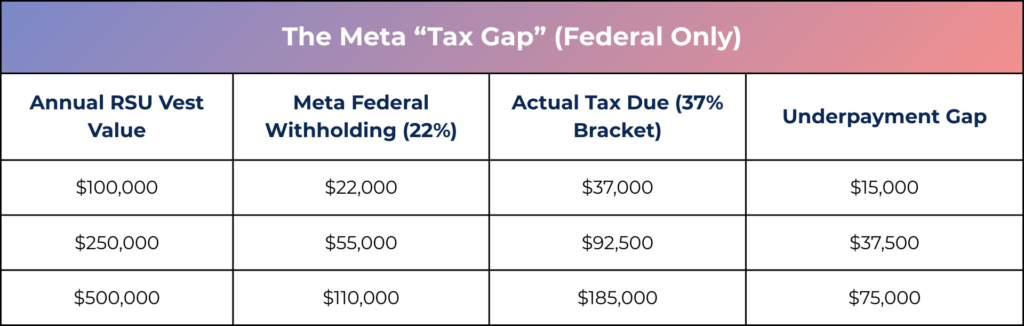

The Meta “Tax Gap”

For example, if you have a $250,000 vest, Meta is going to send about $55,000 to the IRS by default. But if you’re in the top tax bracket, you actually owe $92,500. That leaves a $37,500 hole in your tax plan that you have to make up elsewhere. Seeing this number ahead of time is the difference between a calm April and a very stressful one.

For illustrative purposes only. Based on the 2026 supplemental withholding rate of 22% vs. the top executive tax brackets.

Note: The table above doesn’t account for the 3.8% Net Investment Income Tax (NIIT) or State Taxes (NJ/NY), which can push that “gap” even wider.

There are a few ways to reduce this underpayment gap:

- Adjust your regular paycheck withholding to align more closely with your actual tax rate.

- Make quarterly estimated tax payments to account for the shortfall.

- Set aside part of each vest as a tax buffer so you have enough cash available at tax time to cover your actual liability.

A Quick Note on Your W-4

One of the most common reasons Meta employees fall behind on taxes is the “default” withholding. Since the 22% rate rarely covers the full bill for high earners, you might consider adjusting your W-4 elections to “Single” (even if you’re married). This simple change triggers a slightly higher withholding on your base salary, which acts as a built-in buffer for your RSU vests.

If you decide to go this route, just keep two things in mind:

- The Household View: Consult with a professional to make sure this makes sense for your specific household situation so you aren’t accidentally over-withholding.

- The “Safety” Rule: Check in with your financial planner and tax professional mid-year. They can help you align your withholdings with your actual expectations for the year so you know exactly what’s coming due—and can avoid any underpayment penalties.

Meta also gives you the option to increase the federal withholding rate specifically for RSU vests, which can be one of the simplest ways to stay ahead of the tax impact. You can do this at almost any point during the year, and the change will apply to future vests as long as it’s made far enough in advance, usually about a week before the scheduled vest date.

How to find it:

To find the RSU supplemental withholding options in Workday, go to your Workday profile → Job → Additional Data.

Step 3: Decide How Much Meta Stock to Keep

After you account for taxes, the next big decision is how much Meta stock you actually want to hold. This is where things can get tricky, because it’s very easy for a large portion of your wealth to end up tied to the same company that also pays your salary.

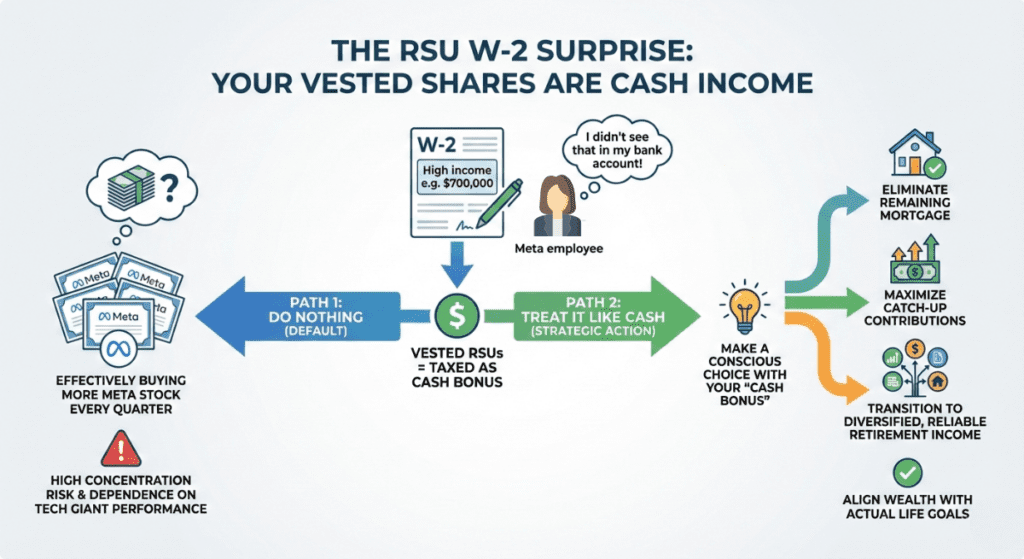

The “W-2 Surprise”: Why Your RSUs Are Actually Cash

Every year, I talk to Meta employees who open their W-2 and are shocked to see they “earned” $700k. Their first reaction is usually: “There’s no way—I didn’t see that much hit my bank account!”

Here’s the reality: It’s because your Meta RSUs are your income.

The moment your shares vest, the IRS treats it exactly like a cash bonus. Imagine if Meta handed you a $100,000 cash bonus today. Would you take every single dollar of that cash and immediately go buy more Meta stock?

Most people wouldn’t. They’d take that “cash bonus” and use it to eliminate a remaining mortgage, maximize catch-up contributions, or transition those funds into a diversified stream of reliable retirement income that doesn’t depend on the daily performance of a tech giant.

But when you “do nothing” with your vested RSUs, you are effectively making the choice to buy more Meta stock every single quarter. If you want your wealth to align with your actual life goals, you have to stop treating RSUs like a “stack of shares” and start treating them like the cash flow they actually are.

So, if the logic says to treat it like cash, why do so many of us stay heavily invested in one place?

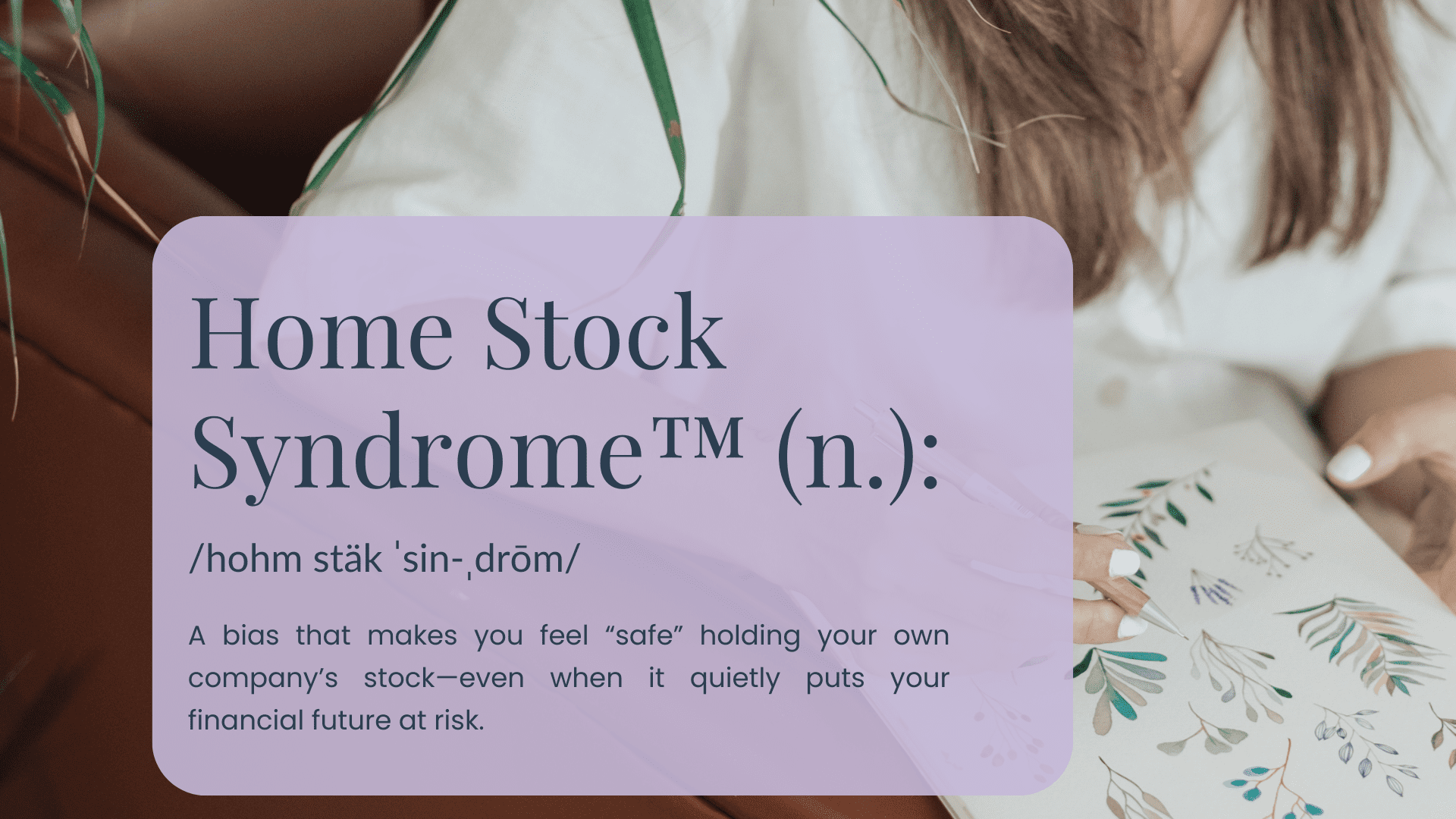

The Challenge with Home Stock Syndrome™

Most people naturally feel more comfortable holding their own company’s stock (I call this Home Stock Syndrome™). You know the business, you follow the news, and it feels familiar.

The challenge is that when your income, your equity compensation, and a large share of your investments all depend on the same stock, your financial life becomes less resilient than it looks on paper. A sharp drop in the share price can affect multiple areas at once.

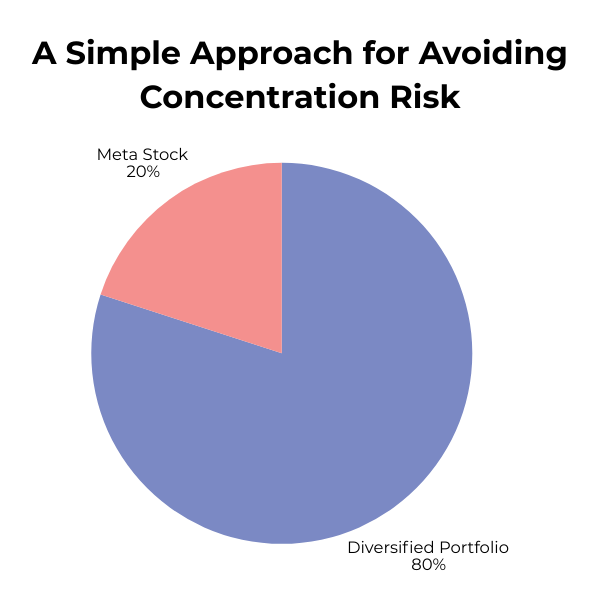

One simple way to keep this in check is to look at how much of your total investable assets are tied up in vested Meta equity. As a general rule of thumb, once a single stock starts creeping past about 15–20% of your investable assets, it’s time to diversify.

This is where a clear, written plan helps. Deciding ahead of time what percentage of Meta stock you’re comfortable holding, and what you’ll do once you exceed that level, removes emotion from the equation.

Step 4: Create a Rules‑Based Selling Plan

Once you’ve decided how much Meta stock you’re comfortable holding, the next step is making that decision easy to follow in real life.

A rules-based plan gives you something steady to lean on through market ups and downs. Instead of reacting to headlines or second-guessing yourself at each vest, you’re following a framework you already chose when things felt calm and rational.

There are a few common ways people approach this:

- Sell shares as soon as they vest and reinvest the proceeds into a diversified portfolio, treating Meta RSUs much like cash compensation.

- Sell a set percentage over time to reduce timing risk (for example, selling 25% of your shares over the next four quarters).

- Adjust the pace of sales based on price levels, selling more aggressively when the stock is above a certain range and slowing down when it’s below, while still working toward diversification.

It also helps to align your selling plan with real life. If you have near-term needs, such as taxes, building an emergency fund, or a home purchase, for example, those priorities can guide how you use your vested shares early on. You can then apply your diversification rules to your remaining shares.

Step 5: Transform Meta RSUs Into Long‑Term Wealth

The point of your Meta RSUs isn’t to give you more to manage or worry about. When handled thoughtfully, they can become one of the strongest drivers of long-term progress in your financial life.

Many people use RSU proceeds to strengthen the foundation first. That might mean fully funding pre-tax, Roth, or after-tax 401(k) contributions, including a Mega Backdoor Roth if it’s available to you. Others direct RSU dollars into a diversified taxable investment portfolio that isn’t overly concentrated in tech or a single company.

RSUs can also be a powerful way to fund specific goals, like a future home purchase, education savings, or creating more flexibility around when and how you work.

A few timing details are worth keeping in mind as you consider your approach:

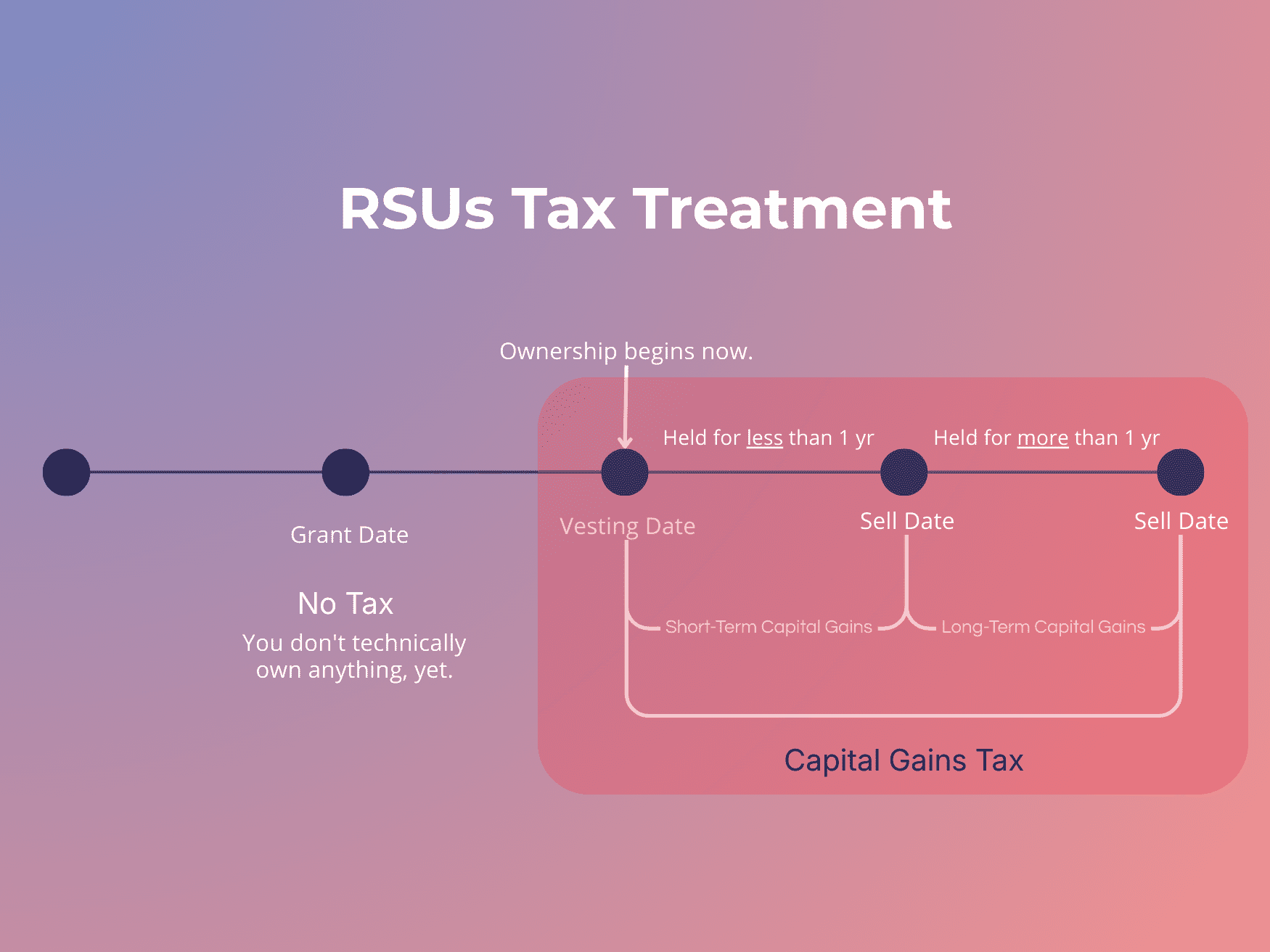

- Once your Meta RSUs vest, any additional growth is taxed as capital gains. Shares sold within a year are taxed at short-term rates, while shares held longer than a year qualify for lower long-term rates, making your holding period a deliberate planning choice.

- As your career progresses and grant sizes increase, especially at more senior levels, it’s important to revisit your RSU strategy regularly. For many people, equity compensation becomes a primary source of long-term wealth, driven less by the grants themselves and more by the discipline behind how those shares are managed over time.

Align Your Meta RSUs with the Life You’re Building

Your Meta RSUs can play a meaningful role in the life you’re building when you have a plan that’s thoughtful and intentional. You deserve to understand how this part of your compensation fits into the bigger picture and to make decisions that feel confident and informed. And you don’t have to sort through it on your own.

One of the most effective ways to make the most of your RSUs is to work with someone who has helped other Meta employees navigate these same decisions in real life. At Align Financial Solutions, we partner with women leaders to turn complex benefits into practical and purposeful plans. We’ll help you review your options, talk through the tradeoffs, and build a strategy that supports the life you want to live, not just today, but years from now.

If you’re ready to take the next step, schedule a 15-minute Align Call and let’s start creating a plan that puts your Meta RSUs to work for you.