Written by Hazel Secco, CFP®, CDFA®

Navigating your financial life can feel overwhelming. With so many investment choices, tax decisions, and long-term planning considerations, it’s easy to feel unsure about where to start. That’s where a financial advisor can help.

But not all financial advisors are the same — and choosing the right one matters.

This guide will walk you through how to choose a financial advisor who fits your goals, values, and financial needs, so you can move forward with confidence and clarity.

Table of contents

Understanding Your Financial Needs

Before you start looking for a financial advisor, it’s important to understand what kind of help you actually need. Are you focused on retirement planning, investing, tax planning, or something else? Knowing your priorities will help you find an advisor who is the right fit for your situation.

Retirement Planning

If you’re thinking about life after work, you may want an advisor who specializes in retirement planning. A retirement-focused advisor can help you understand your savings options, estimate future income, and build a plan that supports the lifestyle you want.

Beyond the numbers, a good retirement planner helps you clarify what matters most to you and your family, so your financial plan reflects your values and goals.

Investment Management

If your main goal is growing and managing your wealth, look for an advisor experienced in investment management. They can help you understand different investment options, build a diversified portfolio, and manage risk.

A financial advisor will also make sure your investments align with your comfort level, time horizon, and long-term goals—so you’re not taking on more risk than you’re comfortable with.

Tax Planning

Tax planning is an important part of financial planning, especially as you approach retirement. A knowledgeable advisor can help you look for ways to reduce taxes over time and make your income more efficient.

For example, some people may benefit from gradually converting retirement accounts like a 401(k) or IRA, while others may consider different timing strategies. Because everyone’s situation is different, tax planning requires careful analysis and coordination with professionals such as your financial advisor, CPA, or tax preparer.

Charitable Planning

If giving back is important to you, working with a financial advisor who understands charitable planning can make a big difference. There are many ways to donate—some more tax-efficient than others—and the right strategy depends on the type of assets you own and your giving goals.

An experienced advisor can help you support causes you care about while maximizing the impact of your contributions.

Debt Management

If you’re dealing with significant debt, a financial advisor can help you create a clear and realistic plan to pay it down. Advisors experienced in debt management can help prioritize balances, improve cash flow, and reduce financial stress over time.

Estate Planning

If leaving a legacy or protecting your family is a priority, estate planning is essential. While estate attorneys handle legal documents, financial advisors often work closely with them to make sure your financial plan aligns with your wishes.

A financial advisor can help explain complex estate documents, coordinate with attorneys, and guide decisions around trusts, beneficiaries, and wealth transfer—especially when family dynamics or assets are more complex.

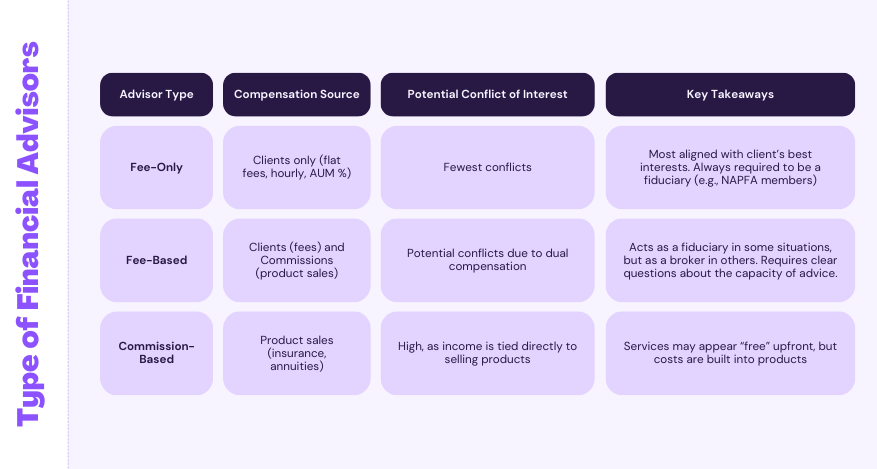

Types of Financial Advisors

Fee-Only Advisors

Fee-only advisors are commission-free advisors. They are compensated only by their clients—never by commissions, referral fees, or product sales. Clients may pay through flat fees, hourly rates, or a percentage of assets under management.

According to the National Association of Personal Financial Advisors (NAPFA), fee-only advisors have the fewest conflicts of interest because their compensation does not depend on selling financial products. NAPFA also requires its members to act as fiduciaries at all times, meaning they are legally and ethically obligated to put their clients’ interests first.

Because fee-only advisors do not receive compensation from third parties, their advice is designed to be objective, transparent, and aligned solely with the client’s goals.

Fee-Based Advisors

Fee-based advisors are often dually registered, meaning they can operate in two different roles. In some situations, they act as fiduciaries under an investment advisory registration. In other situations, they may act as brokers under a broker-dealer registration.

Because of this structure, fee-based advisors are not compensated exclusively by their clients. While they may charge fees for financial planning or investment management, they can also earn commissions from insurance or financial products they recommend.

This dual compensation model can create potential conflicts of interest, depending on the products involved and the role the advisor is acting in at the time. That’s why it’s important for clients to understand how and when their advisor is being paid and under which capacity the advice is being provided.

As part of this process, it’s appropriate to ask direct questions—such as whether the advisor is fee-only—even if they describe themselves as a fiduciary. Understanding both compensation structure and fiduciary responsibility helps ensure the advice you receive truly aligns with your best interests.

Commission-Based Advisors

Commission-based advisors are paid when they sell financial products, such as insurance policies or annuities. While their services may appear “free” upfront, the cost is often built into the products they recommend.

Because their income is tied directly to product sales, this compensation model can create incentives that may not always align with a client’s best interests. For this reason, clients need to understand how, when, and how much an advisor is compensated—something that can be difficult to fully see or evaluate without clear disclosure.

Why Compensation Model Matters

A financial advisor’s compensation structure affects the advice you receive. Working with a fee-only fiduciary advisor can provide confidence, knowing that your financial advisor provides recommendations without hidden incentives or product-driven pressure.

For many individuals and families—especially those navigating complex financial decisions—this alignment can make a meaningful difference in both trust and long-term outcomes.

Checking Professional Credentials

A financial advisor’s credentials can offer valuable insight into their training, experience, and ethical standards.

Advisors who hold the Certified Financial Planner™ (CFP®) designation have completed rigorous education requirements, passed a comprehensive exam, and met experience standards in financial planning. CFP® professionals are also held to a fiduciary standard, meaning they are required to act in their clients’ best interests when providing financial advice.

You can search for a CFP® professional by location or specialty through the Financial Planning Association (FPA) or the CFP Board’s official website.

In addition, some advisors are members of the National Association of Personal Financial Advisors (NAPFA). NAPFA has particularly strict requirements, including a fee-only compensation structure and a fiduciary obligation at all times. Because of these standards, only a small percentage of financial advisors nationwide qualify for NAPFA membership, making it a helpful credential for those seeking highly transparent, client-aligned advice.

Checking credentials and professional affiliations can help you better understand an advisor’s qualifications and commitment to ethical financial planning.

Questions to Ask Potential Financial Advisors

When meeting with a potential financial advisor, don’t hesitate to ask direct and thoughtful questions. Understanding how an advisor works—and how they are paid—can help you determine whether they’re the right fit for you.

11 Questions To Ask When Looking for a Financial Advisor

Here are some important questions to consider:

- What services do you offer, and who do you typically work with?

- What professional credentials do you hold?

- Are you a Certified Financial Planner™ (CFP®)?

- Are you a fee-only financial advisor?

- How are you compensated for your services?

- Are you always acting as a fiduciary?

- What is your approach to financial planning?

- How often will we meet to review my financial plan?

- Who will I be working with throughout the planning process?

- How long have you been working as a financial advisor?

- Do you collaborate with other professionals, such as my CPA or estate planning attorney?

Choosing a financial advisor is a meaningful decision. Take your time, ask questions, and make sure the advisor you choose aligns with your goals, values, and expectations.

Ready to take the next step?

Contact us to learn how our fee-only, fiduciary process can help bring clarity and intention to your financial life. As Certified Financial Planners™ based in Hoboken, NJ, we proudly serve clients nationwide.