Written by Hazel Secco, CFP®, CDFA®

Estimated reading time: 3 minutes

Most high-net-worth divorces aren’t lost in the courtroom—they are lost in the spreadsheets. When you treat every dollar the same, you risk losing a fortune to taxes, penalties, and “paper wealth” that you can’t actually spend.

The Core Framework: The 3 Pillars of Asset Segmentation

To protect your future, we move beyond simple balance sheets and categorize your wealth into three critical buckets:

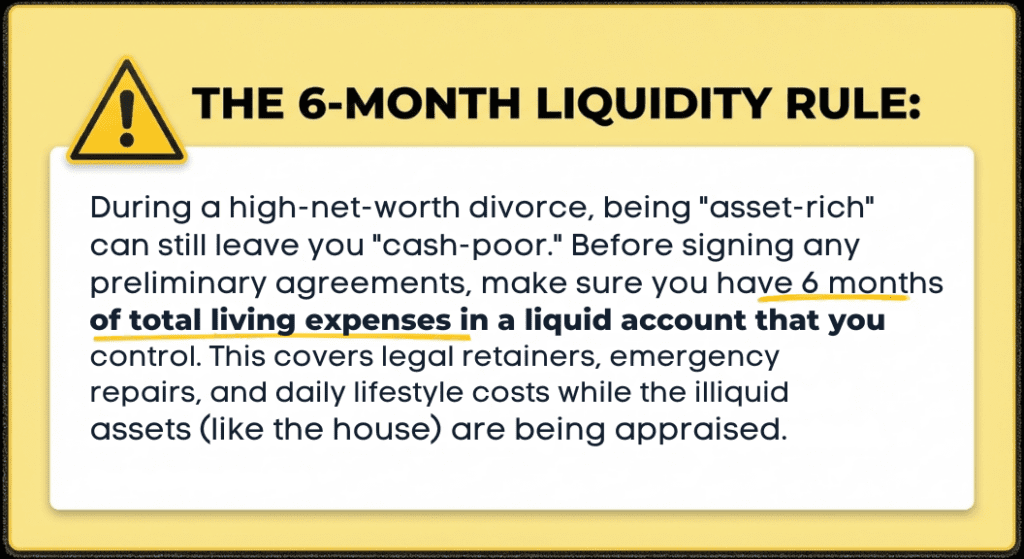

1. Liquid vs. Illiquid: Not All “Million-Dollar” Assets are Equal

A $1M checking account is not the same as a $1M home. Analyze your “cash-ready” position to make sure you aren’t left “asset rich but cash poor.”

- The Trap: Retaining the family home while sacrificing the liquid cash needed for immediate lifestyle expenses and legal fees.

- The Strategy: Maintain a minimum of six months of living expenses in short-term liquid assets.

2. Taxable vs. Non-Taxable: The “Silent” Settlement Shrinker

A $500k IRA is worth significantly less than $500k in a Roth 401(k). We look for the “hidden” tax liabilities that divorce attorneys often overlook.

- The Trap: Accepting an equal split of accounts without accounting for the future taxes due on withdrawals.

- The Strategy: Identifying Roth vs. Non-Roth components to ensure your net, after-tax recovery is actually equitable.

3. Tangible vs. Intangible: Valuing the Invisible

From private business revenue to intellectual property royalties, intangible assets are the most difficult to value—and the easiest to hide.

- The Trap: Undervaluing business interests or ignoring future royalty streams.

- The Strategy: Using professional valuations to ensure every dollar of business growth and intellectual property is on the table.

Why Work with a Divorce Financial Planner?

Divorce attorneys are experts in the law, but they aren’t always experts in the nuances of Private REITs, HELOC qualifications, or complex 401(k) structures. We act as the financial “architect” of your team to:

- Hire the Right People: Avoiding costly mistakes or reducing legal fees by knowing who to hire for your specific situation.

- Analyze Cash Flow: Ensuring your post-divorce lifestyle is sustainable.

- Avoid Penalties: Structuring the division of retirement assets to avoid unnecessary IRS hits.

“Preserving wealth during a high-net-worth divorce isn’t just about dividing what you have—it’s about understanding exactly what each piece is worth after the ink is dry.” — Hazel Secco, CFP®, CDFA®