Written by Hazel Secco, CFP®, CDFA®

Estimated reading time: 16 minutes

Key Points:

- IBM’s retirement benefits are most effective when you understand how the 401(k), RBA, equity compensation, ESPP, and HSA work together, not when they’re managed in isolation.

- Using each benefit intentionally helps you manage taxes, balance growth and stability, and reduce overreliance on IBM stock over time.

- Retirement planning decisions at IBM often come down to timing, especially around vesting schedules, pension options, and when to diversify equity.

- A coordinated strategy turns a strong compensation package into flexibility, giving you more control over your financial future and your timeline.

Table of contents

If you’re an executive at IBM, your compensation goes far beyond a paycheck. Between your pension-style benefits, 401(k), and equity compensation, you have access to tools that can build real wealth and move you closer to a work-optional future.

The challenge is that these benefits don’t always fit together in obvious ways. Each piece makes sense on its own, but the real retirement planning opportunity arises when you understand how they work together and how to use them intentionally.

This is a dense topic, and it’s easy to put off digging into the details. I get it. You’re busy, and your time is valuable. That’s why I put together a simple, straightforward guide that walks through IBM’s retirement benefits in plain English.

My goal is to help you see the full picture, make smarter decisions, and feel confident about the path you’re on. Here’s what you need to know to get the most out of your benefits and bring your retirement goals within closer reach.

Key Retirement Planning Benefits at IBM:

- 401(k) Plan

- Retirement Benefit Account/Legacy Pension Plans

- Equity and Incentive Compensation

- Employee Stock Purchase Plan (ESPP)

- Health Savings Account (HSA)

IBM’s 401(k) plan

IBM’s 401(k) plan has changed over time, which is part of what makes it confusing.

In the past, IBM automatically enrolled new employees in the plan at a 5% contribution rate after 30 days unless they opted out. After one year, employees became eligible for a 5% employer match plus a 1% automatic contribution.

That structure no longer applies. As of 2024, IBM still offers a traditional 401(k) with pre-tax, Roth, and after-tax contribution options, but they’ve eliminated the employer match and 1% automatic contribution.

How to Plan

Even without an employer match, IBM’s 401(k) still matters, especially at the executive level. It’s one of the simplest ways to lower your tax bill now while setting money aside for the future you’re working toward.

For 2026, IRS limits allow you to contribute up to $24,500, or $32,500 if you’re age 50 or older. When you use pre-tax contributions, you reduce your taxable income for the year and give your investments room to grow without ongoing tax drag. You’ll deal with taxes later, however, when you start taking withdrawals (ideally after age 59½).

Think of this as your retirement planning baseline. Maxing out the 401(k) gives you flexibility and creates options. From there, you can decide whether you want to take advantage of additional tax planning strategies, like Roth conversions or the mega backdoor Roth.

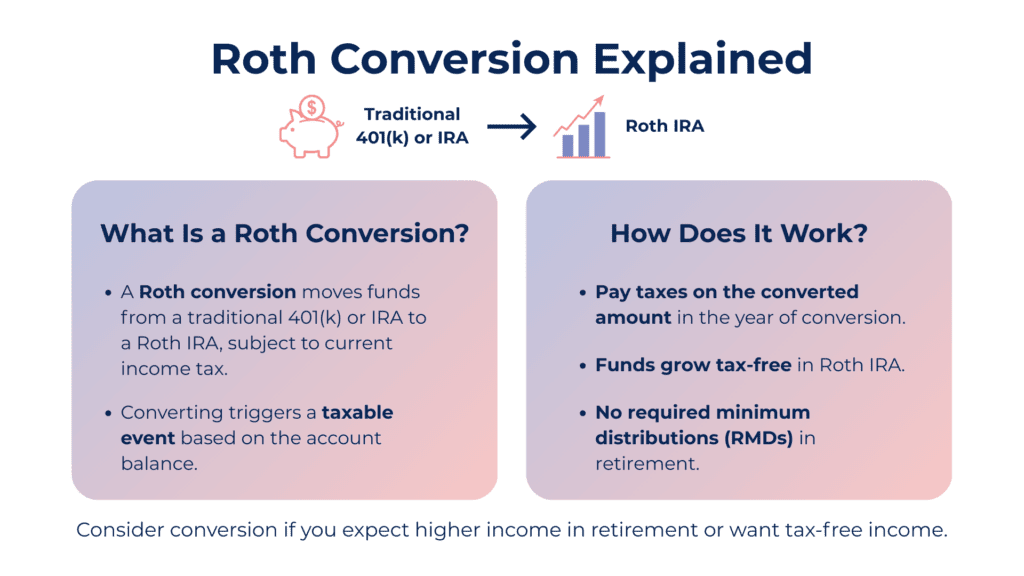

Roth Conversions

Roth IRAs come with strict income limits, and most IBM executives earn too much to contribute directly. This can be frustrating given how valuable Roth money can be later on, but there is a workaround: the Roth conversion.

A Roth conversion works by moving money from a pre-tax account, like a traditional 401(k) or IRA, into a Roth IRA. You pay income taxes on the amount you convert in that year. After that, the money can grow tax-free, and qualified withdrawals in retirement are tax-free too.

This strategy can be especially helpful if you expect your income to stay high or increase over time. It also gives you more control over future taxes and more flexibility when you start living off your investments.

One thing to keep in mind: Roth conversions tend to make the most sense in years when your income dips or when markets are down, since both can lower the tax cost of converting.

The Mega Backdoor Roth

If your 401(k) allows after-tax contributions, you may have access to what’s known as the mega backdoor Roth. This is a slightly more complicated strategy, but once you understand the basic idea, it can be an extremely valuable retirement planning tool for IBM executives.

Here’s how it works. Beyond your regular 401(k) contributions, you can add after-tax dollars up to the IRS’s “all-in” 401(k) limit. For 2026, that limit is:

- $72,000 if you’re under 50

- $80,000 if you’re 50 or older

- $83,250 if you’re between ages 60 and 63

Once those after-tax dollars are in the plan, you can convert them to Roth, either inside the 401(k) or by moving them to a Roth IRA. Since you’ve already paid taxes on the contributions, the conversion itself usually comes with little to no additional tax, as long as it happens before meaningful earnings build up.

Keep in mind this isn’t something everyone needs to do. But for IBM executives who want to build a pool of tax-free income and move more quickly toward a work-optional future, it can be incredibly effective when used thoughtfully.

IBM’s Retirement Benefit Account (RBA) and Legacy Pension Plans

IBM has made a meaningful shift in how it provides pension-style benefits, and this is one area where it really pays to slow down and understand what you have.

The Retirement Benefit Account (RBA)

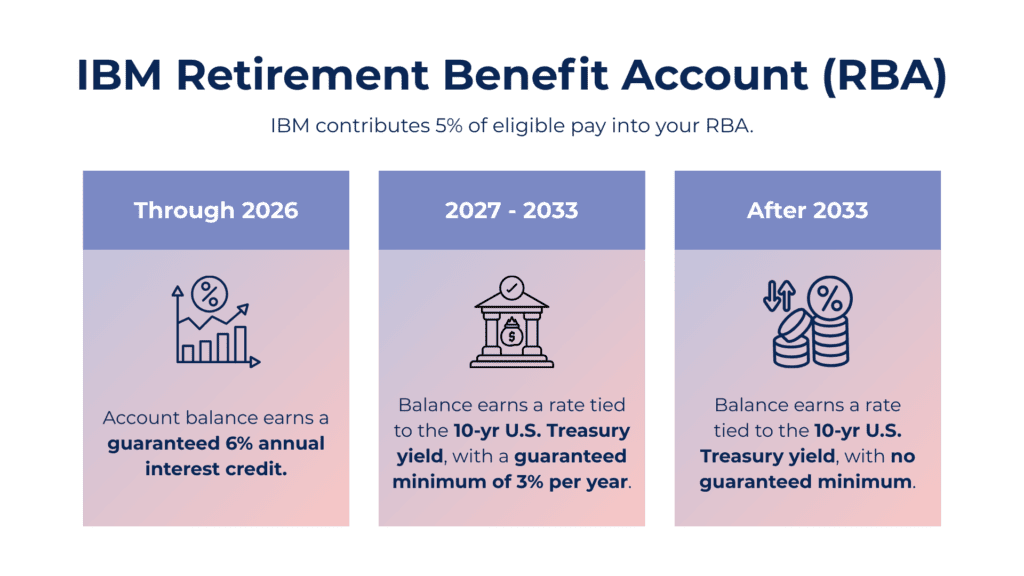

As of January 1, 2024, IBM moved to a Retirement Benefit Account (RBA). Eligibility generally requires one year of service, and employees are immediately vested once eligible.

Think of the RBA as a modern version of a pension, structured as a cash balance defined benefit plan. Here’s what that means in plain terms:

- IBM funds the account entirely.

- You don’t contribute to it, and you don’t choose the investments.

- IBM manages the money and credits your account based on a set formula.

- When you’re vested and eligible, you can typically choose between taking the benefit as a lump sum or turning it into lifetime income through an annuity.

Specifically, IBM contributes 5% of eligible pay into the RBA. Through 2026, those balances earn a guaranteed 6% annual interest credit. After that, the account will earn a rate tied to the 10-year U.S. Treasury yield, with a guaranteed minimum of 3% per year through 2033.

Theoretically (and according to IBM), this change adds a stable, predictable benefit and helps diversify employees’ retirement resources. In practice, it gives you something many retirement plans don’t: a company-funded benefit with built-in downside protection and steady growth.

How to Think About the RBA in Your Plan

Because you don’t control how the RBA is invested, it helps to think about where it fits in your overall investment approach. For most IBM executives, the RBA functions like the conservative or fixed-income portion of their retirement portfolio.

That perspective matters when you decide how to invest the rest of your money. If the RBA represents a meaningful portion of your total retirement assets, you may feel more comfortable investing your 401(k), IRAs, and taxable accounts with a growth focus, such as stocks or real estate.

Over time, the RBA can also serve as a stabilizing foundation, especially as you get closer to retirement and start thinking more about income and downside protection.

Legacy Pension and Personal Pension Plan Benefits

If you’ve been with IBM for a long time, you may also have benefits from the older Personal Pension Plan. While that plan was frozen for many participants, the introduction of the RBA effectively builds on those legacy benefits rather than replacing them outright.

This is where details really matter. The timing of when benefits become payable, whether early retirement reductions apply, and how interest rates affect lump sum values can all influence when it makes sense to retire and how much risk you’re taking relative to the markets.

You’ll also want to understand the trade-offs between taking a lump sum versus electing lifetime income. That decision can affect not just your cash flow, but also your tax situation and how much market risk and longevity risk you are willing to carry personally.

When you thoughtfully coordinate these pieces of your retirement plan, the RBA and any legacy pension benefits can provide a strong income foundation. This can give you more freedom in how you use the rest of your investments and more confidence as you move toward a work-optional future.

Equity and Incentive Compensation for IBM Executives

For many IBM executives, equity compensation makes up the largest portion of total pay and is a significant piece of your overall retirement plan. These incentives tie your income and long-term wealth directly to company performance, stock price growth, and IBM’s strategic priorities.

Because these awards often arrive over several years, they can quietly become one of the most important drivers of your financial future. They can also create stress if you don’t feel clear on how they work or how they fit into the rest of your plan.

Equity Compensation at IBM

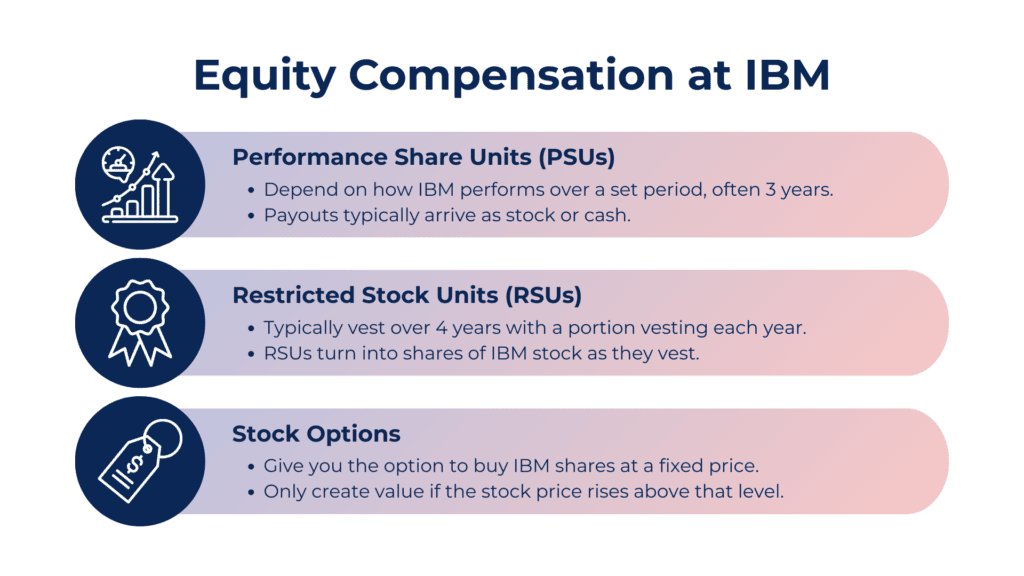

IBM executives typically receive a mix of PSUs and RSUs, and, for some roles and years, stock options as well. Each one plays a different role in your retirement strategy.

- Performance Share Units (PSUs) depend on how IBM performs over a set period, often three years. You receive a target number of units up front, but the final payout depends on whether the company hits specific goals. While some periods pay out less than expected, strong performance can lead to payouts well above the original grant. When the period ends, payouts typically arrive as stock or cash. (Be sure to check your award terms since these specifics differ by role, grant year, and plan document.)

- Restricted Stock Units (RSUs) vest over time. A common structure is four years, with a portion vesting each year. As RSUs vest, they turn into shares of IBM stock, and their value depends on the stock price on the vesting date.

- Stock options give you the ability to buy IBM shares at a fixed price. They only create value if the stock price rises above that level. When they do, you have decisions to make around when to exercise and what to do with the shares.

Key Factors That Influence Equity

When it comes to equity and incentive compensation at IBM, a couple of things tend to matter more than people expect.

First is timing. Vesting schedules and performance periods drive when equity turns into real money. Leaving IBM too early can mean walking away from unvested awards, unless you meet specific retirement or service requirements, so be sure to check this before taking a job elsewhere or setting your retirement date.

The second factor is concentration risk. As RSUs vest and PSUs pay out, it’s easy to end up with a large portion of your net worth tied to IBM stock.

That can feel comfortable when things are going well and uncomfortable when they’re not. Paying attention to how much of your net worth is tied to company stock helps you decide when it makes sense to hold and when it might be time to diversify.

IBM’s Employee Stock Purchase Plan (ESPP)

IBM’s Employee Stock Purchase Plan gives you a simple way to buy company stock at a discount using money that comes straight out of your paycheck. For a lot of executives, an ESPP one of the easiest ways to invest consistently in IBM and participate directly in the company’s growth.

The plan offers a 15% discount on IBM stock and runs in six-month cycles. You can contribute up to 10% of your eligible pay, capped at $25,000 per year. If your cash flow changes, you can generally change or stop contributions during the period, subject to IBM’s ESPP rules and deadlines.

How IBM’s ESPP Works

Here’s how the ESPP works:

- You enroll during set enrollment windows before January 1st or July 1st. Once you’re enrolled, payroll deductions start automatically.

- Each offering period runs for six months, either January through June or July through December. Throughout the period, IBM sets aside the amount you’ve elected from each paycheck.

At the end of the six-month ESPP period, IBM looks at the stock price on that specific day and applies the 15% discount to that price. That discounted amount is what you pay for the shares.

Some ESPP plans look back and let you buy shares at the lower of the stock price at the beginning or the end of the period. IBM’s plan doesn’t do that. Your discount applies only to the price on the last day of the period. (It’s a good idea to confirm this in the latest IBM plan materials in case the specifics change.)

Why Participating in the ESPP Can Make Sense

The biggest advantage of IBM’s ESPP is the built-in discount. Buying shares at 15% below market price gives you an immediate edge the moment the shares are purchased. For some people, that discount alone makes participation worthwhile.

The plan is also flexible, which matters if your cash flow changes. You’re not locked in for the full six months. If priorities shift, you can stop contributions or exit the plan mid-cycle without penalty.

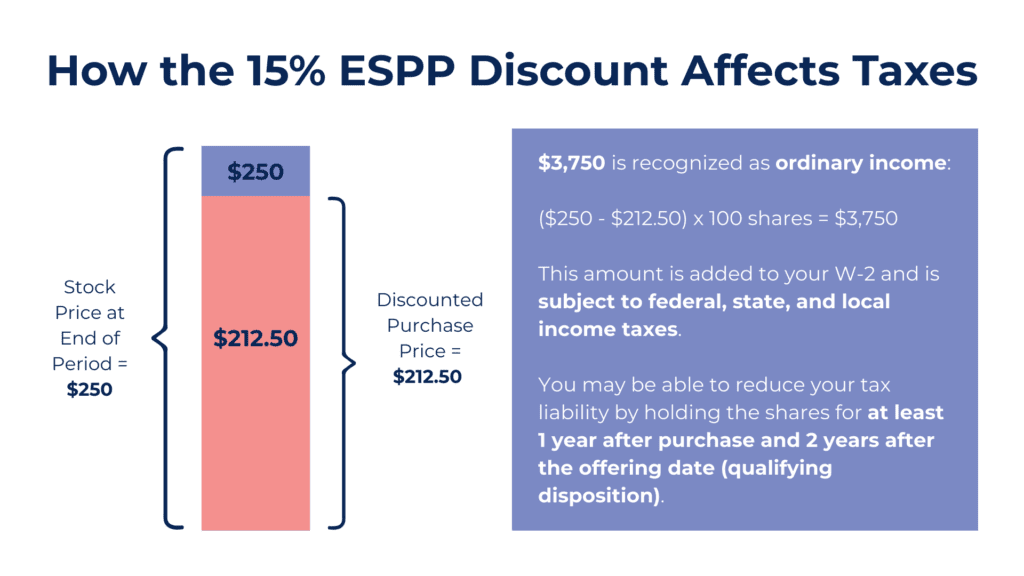

Taxes are an important consideration, but they’re manageable once you know what to expect. Simply put, the 15% discount is treated as ordinary income.

So, if the stock price at the end of the period is $250 and you purchase 100 shares for $212.50 per share, $3,750 is recognized as ordinary income:

($250 x 100 shares) – ($212.50 x 100 shares) = $25,000 – $21,250 = $3,750

This example assumes a qualified Section 423 plan. Tax results differ for qualifying vs. disqualifying dispositions and for non-qualified ESPPs.

If you sell within one year of the purchase date, any additional gain or loss is taxed as short-term capital gain or loss. If you hold the shares for more than one year, additional gains are taxed at long-term capital gains rates.

Using IBM’s ESPP Intentionally

How you use IBM’s ESPP may depend on your broader financial goals. Some executives use it as a steady, automated way to invest. Since payroll deductions make saving and investing more consistent, those purchases can add up over time.

Others take a more tactical approach. They sell shares soon after purchase, capture the discount, and redirect the proceeds toward other goals, such as building cash reserves, funding investments outside IBM, or reducing concentrated stock exposure.

Either approach can work as long as you’re intentional about it. It’s important to remember that ESPP shares add to your overall exposure to IBM stock, and for many executives, that exposure already shows up through equity compensation and career income. Deciding in advance whether you plan to hold, sell, or periodically diversify can help keep the ESPP aligned with the rest of your retirement plan.

IBM’s Health Savings Account (HSA)

If you’re enrolled in one of IBM’s high-deductible health plans, you also have access to a Health Savings Account, or HSA. This is often one of the most flexible and underused benefits available, especially for executives.

An HSA lets you set aside money specifically for health care costs. You contribute pre-tax dollars, the money can be invested once your balance reaches the required threshold, and withdrawals for qualified medical expenses are tax-free.

IBM also contributes to your HSA each year, which helps offset some of your out-of-pocket costs. These contributions count toward annual IRS limits, which are $4,400 for self‑only coverage and $8,750 for family coverage in 2026.

Once your balance is high enough, you can invest HSA funds through your custodian, giving the account long-term growth potential instead of letting it sit in cash.

Using an HSA for Retirement Planning

The primary advantage of an HSA is how favorable it can be from a tax perspective:

- Contributions reduce your taxable income.

- Investment growth can be tax-free.

- Withdrawals for qualified medical expenses are also tax-free.

Because of the way it’s taxed, an HSA can be one of the most efficient ways to save for health care costs. But what many people don’t realize is that unused HSA dollars roll over year after year and stay with you if you change jobs or retire.

In other words, there’s no deadline to use the money. You can let the account grow over time and use it later, including as an additional resource in retirement.

After age 65, you can even use HSA funds for non-medical expenses. Those withdrawals are taxed as ordinary income, much like a traditional IRA, but you won’t pay a penalty. This means an HSA can serve two roles at once: a way to help manage health care costs today and an additional retirement resource tomorrow.

Pulling It All Together: Retirement Planning Strategies for IBM Executives

IBM’s retirement benefits work most effectively when you stop looking at them as separate buckets and start using them as a system.

Your 401(k) is a good foundation. It helps lower your tax bill today and gives you flexibility later, especially if you layer in Roth strategies over time.

The RBA and any legacy pension benefits can add stability. Because IBM funds them and manages the investment risk, they can serve as a reliable income base and allow you to think differently about risk in the rest of your portfolio.

Equity compensation and the ESPP bring growth potential, but they also require intention. These benefits can meaningfully accelerate wealth, but they also increase your exposure to IBM stock. Coordinating vesting schedules, retirement timing, and diversification decisions can help turn equity from a source of stress into a tool that helps support your goals.

The HSA can help round out your retirement plan. Used well, it covers health care costs today and adds another flexible pool of money down the road.

When these pieces work together, you gain options. You can manage taxes more thoughtfully, balance growth and stability, and create additional income streams that support a work-optional future.

Align Your Retirement Plan with Your Broader Goals

IBM gives you meaningful options to build long-term security and flexibility. You’ve earned these benefits, and when you use them intentionally, they can support far more than a retirement date or a balance sheet. Stepping back to see how everything fits together can help you make decisions that align with your goals, your lifestyle, and your timeline.

At Align Financial Solutions, we work with women leaders to turn complex benefits into clear, practical plans. We help you understand your options, weigh the tradeoffs, and build a strategy that helps support the life you want now and in the years ahead.

If you’re ready to take the next step, schedule a 15-minute Align Call and let’s start shaping a plan that moves you toward a work-optional future.