Written by Hazel Secco, CFP®, CDFA®

Key Points

- Disney’s benefits go far beyond a paycheck, and can include retirement plans, pensions, equity compensation, health accounts, and severance protections.

- Understanding how your 401(k), deferred compensation, and pension benefits fit together can meaningfully improve flexibility and retirement timing.

- Equity compensation often makes up a large share of total pay for senior leaders and can require proactive planning around vesting, taxes, and diversification.

- HSAs and FSAs can reduce taxes today and, when used strategically, support long-term financial flexibility.

- Severance and insurance benefits can provide critical protection during career transitions and should factor into decisions around role changes and long-term planning.

Table of contents

- Disney Retirement Benefits Summary

- #1: Disney’s Core Retirement Benefits: 401(k) and Deferred Compensation Plans

- #2: Disney’s Pension Benefits

- #3: Disney Stock Awards

- #4: Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA)

- #5: Severance and Insurance Benefits

- Disney retirement FAQs I hear from Women Leaders

- Turning Your Disney Benefits into Real-Life Flexibility

- Related Posts

As a Disney senior leader or executive, your compensation goes well beyond a regular paycheck. Between equity, retirement plans, and other financial benefits, you have access to tools that can meaningfully support long-term wealth building. The opportunity can be significant, but only if you understand how these pieces fit together and how to use them intentionally.

I know how hard it is to find the time or mental energy to dig into the fine print of a benefits package, especially when your days are already full. That’s why I put together a practical guide that helps break down the benefits you’re likely receiving and shows you how they can support the life you’re working toward.

Disney Retirement Benefits Summary

Disney’s retirement benefits are primarily delivered through three plans: the Disney Savings and Investment Plan (your Disney 401k), the Disney Retirement Savings Plan (a cash‑balance pension for many salaried employees), and, for some long‑tenured Disney cast members, the traditional Disney Salaried Pension Plan, all administered through Fidelity.

When you log in to Fidelity NetBenefits to view your “Disney Retirement Savings Plan” or pension details, you are seeing one piece of a larger retirement picture, not the whole story.

#1: Disney’s Core Retirement Benefits: 401(k) and Deferred Compensation Plans

For many senior leaders at Disney, two core retirement benefits form the foundation of your long-term financial plan.

Disney’s Savings and Investment Plan

Disney’s Savings and Investment Plan (Disney SIP) is your main 401(k). It allows you to set aside a percentage of each paycheck on a pre‑tax or Roth basis, and Disney adds a company match based on your eligible compensation. For many salaried Disney cast members, Disney matches up to 2% of your compensation, but the exact formula can vary by role and business unit, so it is important to confirm your match details in your Fidelity 401(k) portal.

Disney’s Voluntary Non-Qualified Deferred Compensation Plan

If you’re an executive or highly compensated employee, you may be eligible to defer a portion of your salary and bonuses on a pre-tax basis. These contributions grow tax-deferred and are taxed when you take distributions later, potentially during lower-income years.

Together, these plans help you save consistently, grow your money over time, and take advantage of potentially meaningful tax benefits.

How to estimate your Disney 401(k) match

- Log in to your Disney 401k on Fidelity NetBenefits and find your “Company Match” percentage.

- Note:

- The maximum percentage of your pay that is eligible for a match (for example, 4 percent).

- The match rate (for example, 50 percent of what you contribute).

- Do this quick calculation:

Example: If you earn 150,000 dollars, Disney matches 50 percent of the first 4 percent you contribute, and you contribute at least 4 percent:

And here’s how to get more out of them:

- Contribute at least enough to your Disney 401(k) to receive the full company match every year. That match is one of the most reliable returns available to you.

- If cash flow allows, work toward the annual IRS contribution limit. For 2026, you can contribute up to $24,500, or $32,500 if you’re age 50 or older.

- Keep your investment choices simple and diversified. Low-cost index funds or an age-appropriate target-date fund can work well, especially if a meaningful portion of your compensation is already tied to Disney stock.

Once you’ve maxed out your Disney 401(k), the Deferred Compensation Plan can help you build additional tax-deferred savings. However, make sure you can comfortably cover living expenses and stay on track with emergency savings and other near-term goals before deferring income.

It’s a good idea to consult with a financial planner before enrolling in the Deferred Compensation Plan since once you make your selections, flexibility is much more limited than in a traditional retirement account.

#2: Disney’s Pension Benefits

Many Disney employees see both the Savings and Investment Plan (Disney SIP) and the Disney Retirement Savings Plan listed when they log in at Fidelity, and it is not always obvious how they differ. The Disney SIP is your employee‑funded 401(k) with a Disney match, while the Disney Retirement Savings Plan is a separate, company‑funded cash‑balance pension that grows based on a formula tied to your pay and years of service.

With the Disney 401(k) plan, you’re responsible for contributions and investment selections. Disney’s pension benefits shift that responsibility to the company, complementing your 401(k) with a steadier and more predictable source of retirement funds.

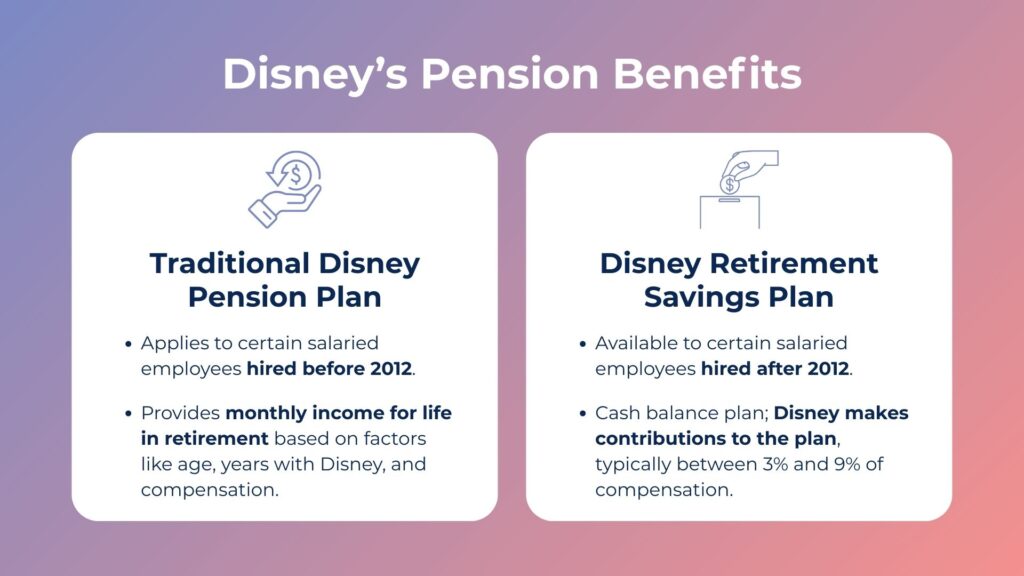

Traditional Disney Pension Plan Vs. Disney Retirement Savings Plan (DSRP)

Disney has two pension plans depending on your date of hire:

Traditional Disney Pension Plan. This plan applies to certain salaried employees hired before 2012 and provides a monthly income for life in retirement. The benefit is based on factors like age, years with Disney, and compensation.

Disney Retirement Savings Plan (DRSP). This is a cash‑balance pension plan available to many salaried employees hired after 2012. Disney contributes a percentage of your eligible compensation. It’s often in a range of 3 percent to 9 percent each year, into a notional account that earns interest based on plan rules.

Key Points About Traditional Pension Plan

If you’re covered by the Traditional Pension Plan, here are a few key points to keep in mind:

The maximum benefit is usually available at age 65 unless you continue working and accruing benefits beyond that point. Earlier claiming options may be available, but they often come with reduced payments.

You have multiple payout options, including choices that provide income for a spouse or other beneficiaries. These decisions can affect both lifetime income and taxes, so it’s worth reviewing them carefully with a financial planner.

Key Points About Disney Retirement Savings Plan (DSRP)

If you’re enrolled in the DRSP, the planning considerations are slightly different:

- At retirement, you can typically choose between monthly payments or a lump-sum distribution. Just know that lump sums can create a sizable tax bill without careful planning.

- You may also have the option to roll the balance into an IRA or a new employer’s 401(k). This usually allows you to continue deferring taxes.

When you review your Disney Retirement Savings Plan balance on Fidelity, think of it as a complement to, not a replacement for, your 401k. Your decisions around when to leave Disney, whether to take a lump sum vs. monthly payments, and how to roll funds to an IRA can all affect taxes and retirement income. And that’s exactly why modeling different scenarios before you submit any pension election forms is so valuable.

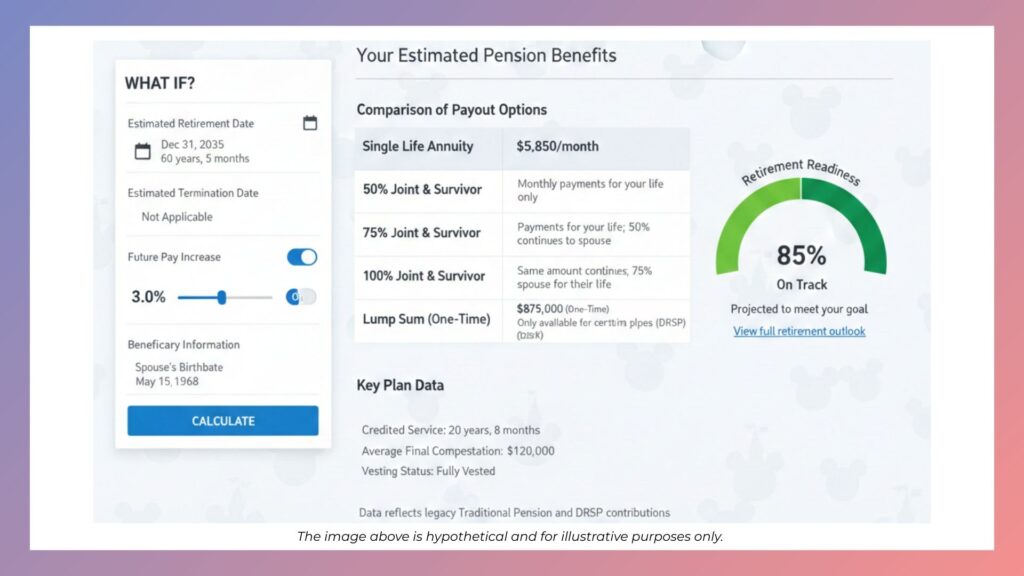

No matter which plan you’re in, use the Pension Estimating Tool in your benefits portal to model different retirement dates. Pension benefits often influence timing decisions more than people expect, especially when you’re thinking about how and when to step back from work.

#3: Disney Stock Awards

As you climb the Disney ladder, equity awards are often a substantial part of your compensation. If you ignore this benefit or let it run on autopilot, you might be leaving money on the table.

Disney tends to award equity in the form of restricted stock units (RSUs) and performance-based awards. If you’re managing either (or both), here are a few tips.

Tips for Your Disney RSUs

Know your vesting calendar.

- When you receive your Disney shares affects both cash flow and taxes. RSUs often vest over three years, usually about a third each year, with smaller amounts vesting along the way.

- Performance-based awards, which are common at more senior levels, typically vest after a three-year performance period and depend on company results.

Treat each vest like a cash bonus that happens to show up in stock. Decide ahead of time how much you’ll sell at vest, so your portfolio doesn’t become too concentrated in Disney stock.

Think about taxes. Withholding on equity income is often lower than your actual tax rate, which can create an unpleasant surprise later. You may need to adjust withholding, make estimated payments, or set cash aside from each vest to stay ahead of the tax bill.

Be intentional with what you do after you sell. Consider reinvesting the proceeds into a diversified portfolio or using them to fund other financial priorities.

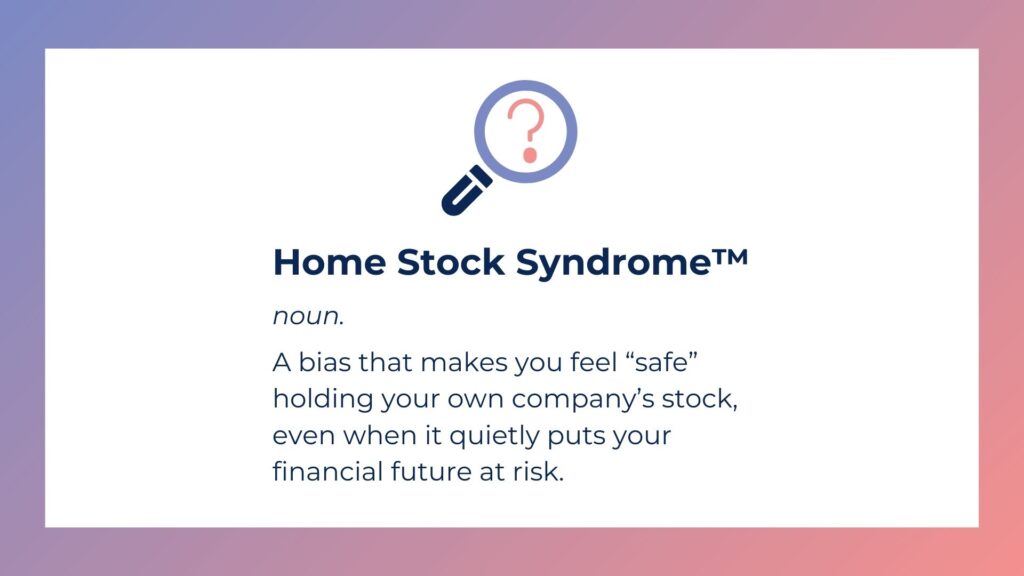

Senior leaders may also receive stock options or be eligible to participate in Disney’s Employee Stock Purchase Plan (ESPP). Both allow you to buy company stock at a discount, which can be valuable, but beware of Home Stock Syndrome™. While holding Disney stock may feel safe because it’s familiar, tying too much of your net worth to one company can potentially put your future at risk.

#4: Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA)

Disney offers tax-advantaged health accounts that can help cover everyday medical expenses. It can also support your long-term financial plan, when used thoughtfully.

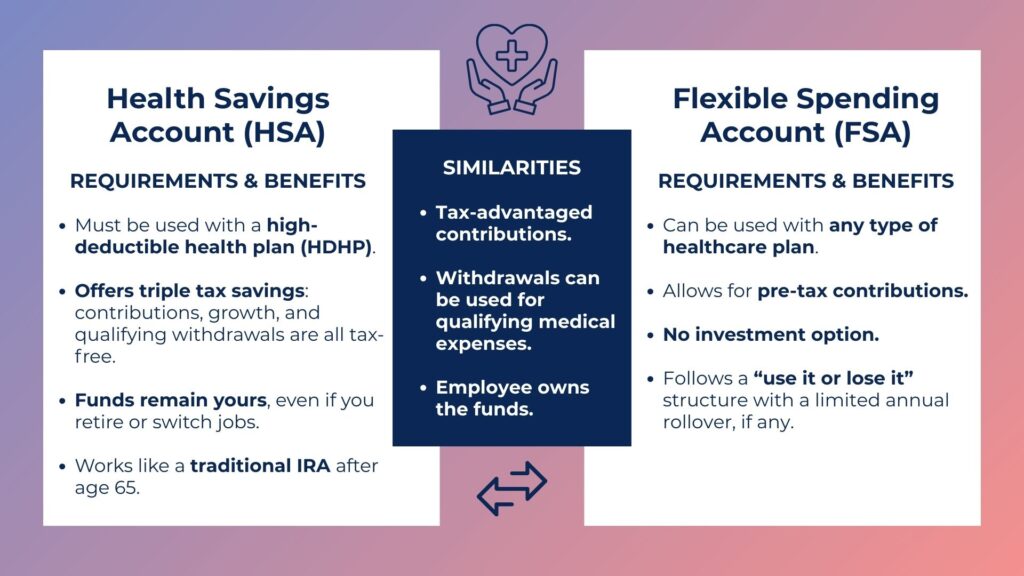

If you’re enrolled in a high-deductible health plan, you’re eligible to contribute to a Health Savings Account (HSA). HSAs are especially valuable because of these reasons.

Values of Health Savings Accounts

They offer triple tax savings.

- You contribute pre-tax dollars.

- You can invest the balance once it reaches the required threshold.

- You can use the money tax-free for qualified medical expenses.

The funds are portable.

- The money is yours, even if you leave Disney.

After age 65, an HSA works much like a traditional IRA.

- Non-medical withdrawals are taxed as ordinary income, while qualified medical expenses remain tax-free.

Disney also offers a Flexible Spending Account (FSA), which allows you to pay for healthcare expenses with pre-tax dollars. But unlike an HSA, an FSA is designed for short-term use.

Most FSAs follow a “use it or lose it” structure, which makes them a better fit for predictable, near-term expenses. Using your FSA for current costs can help preserve more of your HSA balance for the future.

How to Maximize Your HSA Benefits

- If you’re eligible for an HSA, work toward the annual IRS contribution limits: $4,400 for self-only coverage and $8,750 for family coverage in 2026.

- If cash flow allows, consider paying current medical expenses out of pocket or with your FSA and let your HSA stay invested.

- Pro tips: Keep receipts so you have the option to reimburse yourself later if necessary.

#5: Severance and Insurance Benefits

Many Disney benefits focus on building wealth, often in tax-advantaged ways. Others play a quieter but equally important role by protecting what you’ve already built. These benefits don’t always get much attention, but they can matter when circumstances change unexpectedly.

Two parts of your benefits package are especially important to understand:

Executive Severance Pay Plan.

- Effective February 2, 2026, Disney adopted an Executive Severance Pay Plan for eligible executives at the E6 or E7 level. This plan provides severance pay and continued benefits if you’re involuntarily terminated without cause or resign for certain defined reasons and aren’t covered by an individual severance agreement.

Insurance benefits.

- Disney provides employer-paid basic life insurance and accidental death and dismemberment coverage. Additionally, employees can purchase optional long-term disability insurance. Coverage is typically based on a multiple of your base salary, with the option to purchase additional coverage up to plan limits.

Here’s how to think about these benefits in the context of your broader plan:

Know your severance terms.

- Understand your eligibility under the Executive Severance Pay Plan and how many months of income and benefits it could provide if your role ends unexpectedly.

Review your insurance coverage.

- Confirm how many times your salary is covered by life and disability insurance, and increase coverage if needed. The goal is to protect your family and cash flow without forcing you to sell equity or tap deferred compensation at the wrong time.

Look beyond base pay when making career moves.

- When evaluating a new role or internal transition, weigh changes to severance protection, long-term incentive targets, and deferred compensation eligibility alongside any salary adjustment.

When you account for these protections upfront, you can create more resilience in your financial plan and reduce some of the pressure that often comes with career transitions.

Disney retirement FAQs I hear from Women Leaders

- “Is Disney’s 401(k) match good?”

For many cast members, Disney’s match is competitive and can add a significant portion to your retirement savings, especially if you contribute at least enough to receive the full match. The key is to avoid under‑contributing in years when cash flow feels tight, because missed match dollars do not come back later.

- “What is the difference between the SIP and the Disney Retirement Savings Plan?”

Your Disney SIP is the Disney 401(k), where you decide how much to contribute, select investments, and receive a company match. The Disney Retirement Savings Plan is a separate, company‑funded benefit that grows automatically based on your pay and years of service and may be paid monthly or as a lump sum at retirement, depending on your elections.

- “Where do I see all of this?”

You will typically log in to your Disney retirement benefits through Fidelity NetBenefits to see your Disney SIP (401(k)), your Disney Retirement Savings Plan, and, if applicable, your traditional pension. Because the portal shows each plan separately, it is easy to underestimate how strong your overall retirement position is until you look at them together in one plan.

Turning Your Disney Benefits into Real-Life Flexibility

Disney offers a strong benefits package through Disney total rewards, but the real value comes from how you use it. Each benefit can play a distinct role in your financial plan. When you understand how they work together, you can make decisions that support both a work-optional future and the life you want along the way.

At Align Financial Solutions, we help women leaders make sense of complex compensation and benefits, including Disney’s SIP 401(k), Retirement Savings Plan, pension options, equity awards, and severance protections. We help walk you through your options, talk through the tradeoffs, and build a strategy that better supports the life you want now and in the years ahead.

If you’re ready to take the next step, schedule a 15-minute Align Call. Let’s start shaping a plan that helps move you toward a work-optional life.

Related Posts

Disclosures:

Align Financial Solutions (“AFS”) is a registered investment advisor offering advisory services in the State of NJ and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

All written content on this site is for information purposes only and is not intended to provide specific advice or recommendations for any individual. Opinions expressed herein are solely those of AFS, unless otherwise specifically cited. Hazel Secco and AFS are neither an attorney nor an accountant, and no portion of this website content should be interpreted as legal, accounting, or tax advice. Material presented is believed to be from reliable sources and no representations are made by our firm as to other parties’ informational accuracy or completeness. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investment involves risks, including possible loss of principal, and unless otherwise stated, are not guaranteed. Any economic forecasts set forth may not develop as predicted and are subject to change. All information or ideas provided should be discussed in detail with an advisor, accountant, or legal counsel prior to implementation.

Align Financial Solutions, LLC and it’s employees are not affiliated nor endorsed by the Walt Disney Company or its affiliates.