Key Points:

- You don’t need to be a spreadsheet person to understand your financial health; just keep an eye on five key numbers: your net worth, monthly cash flow, emergency fund, credit score, and financial wellness score.

- Your net worth shows your progress, your cash flow reveals your habits, and your emergency fund protects your peace of mind when life throws a curveball.

- A healthy credit score gives you flexibility and freedom, while your financial wellness score helps you check in with how confident and in control you actually feel about your money.

Table of contents

Women in leadership are often masters at juggling multiple responsibilities: careers, families, friendships, community involvement. But with so much on your plate, it’s easy for your personal finances to take a back seat. And let’s be honest, when you finally do get a few hours of free time, the last thing you want to do is open a spreadsheet and crunch numbers.

The truth is you don’t need to be a numbers person to have a clear picture of your financial health. Just like you might track your steps or check your blood pressure as part of maintaining your physical well-being, there are a handful of key financial indicators that tell you how healthy your money life is and whether you’re moving in the right direction.

Here are five simple numbers worth knowing—no math degree required—that can help you feel more confident, make smarter financial choices, and take control of your financial future.

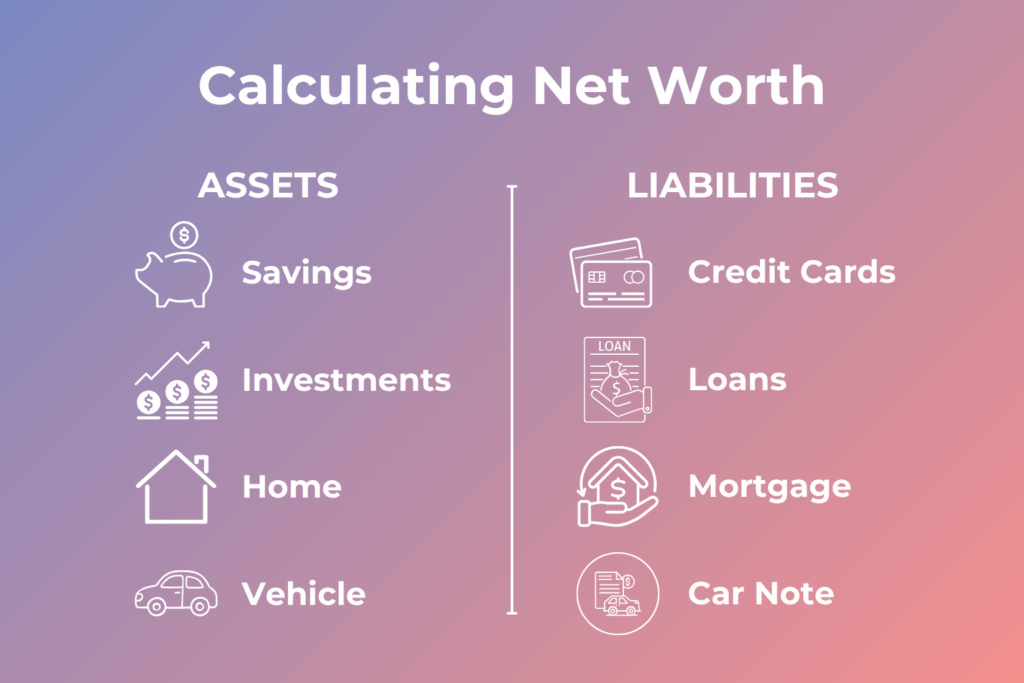

#1: Net Worth

Your net worth is a snapshot of your overall financial position. It represents everything you own (your assets) minus everything you owe (your liabilities).

In simple terms:

Net Worth = Total Assets – Total Liabilities

Your assets might include cash, savings, investments, real estate, and retirement accounts. Liabilities include credit card balances, student loans, car loans, and your mortgage.

Why it matters:

Net worth tells you where you stand. It’s the single most important measure of your financial progress because it captures your entire picture, not just your income or how much is in your checking account today. Tracking it over time shows whether your wealth is growing, stagnant, or shrinking.

A growing net worth usually means your money is working for you. A declining one can signal overspending, too much debt, or an asset that’s losing value.

Here’s how to calculate and track it:

- List your assets and their current values (bank accounts, investments, real estate, vehicles, etc.).

- List your debts (credit cards, loans, mortgage, etc.).

- Subtract your total debts from your total assets.

You can use a simple spreadsheet, your bank’s financial dashboard, or an app like Monarch Money or Tiller to automate the process. It’s best to update your net worth at least twice a year to spot trends and make any necessary adjustments.

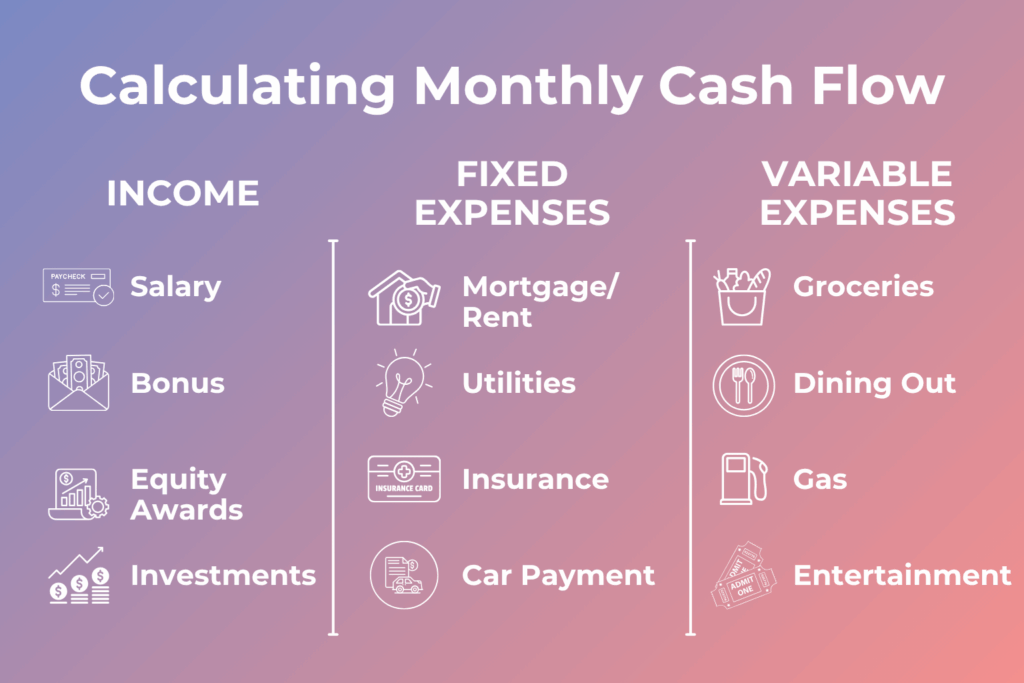

#2: Monthly Cash Flow

Your cash flow shows how much money comes in and goes out each month. It’s the starting point for any financial plan because it reveals whether you’re living within your means or stretching beyond them.

The formula is pretty straightforward:

Monthly Cash Flow = Total Income – Total Spending

Why it matters:

Positive cash flow means you’re spending less than you earn, which creates room for saving, investing, and building long-term stability. Negative cash flow means you’re either dipping into savings or relying on credit to fund your lifestyle. This is a red flag that deserves your attention.

Knowing your cash flow also helps you make informed decisions. For instance, if you’re considering a sabbatical, buying a home, or funding your child’s education, understanding where your money goes allows you to plan realistically instead of reactively.

Here’s how to calculate and track it:

- Start by totaling all sources of monthly income (salary, bonuses, vested RSUs, rental income, etc.).

- Subtract your monthly expenses, both fixed (mortgage, insurance, subscriptions) and variable (groceries, dining out, travel).

Apps like YNAB (You Need a Budget) make it easy to categorize and visualize your spending. Or, if you prefer a simpler system, review your bank and credit card statements for the past three to six months to estimate your average monthly cash flow. Just be sure to leave a buffer for unplanned expenses like car repairs or doctor visits, as these will inevitably come up from time to time.

#3: Emergency Fund Balance

Your emergency fund is your personal safety net, the calm beneath life’s chaos. It’s the cash you set aside for the curveballs you can’t plan for: a sudden home repair, an unexpected medical bill, or a job change you didn’t see coming.

Why it matters:

Think of it as your permission slip to breathe easier. An emergency fund keeps life’s surprises from turning into financial setbacks. Without it, a single unexpected expense can quickly spiral into stress or debt.

For women in leadership, especially those juggling careers, families, and a thousand competing priorities, this cushion also creates freedom. It gives you the flexibility to pause, pivot, or pursue what matters most, whether that’s stepping away from a toxic job, taking time for family, or launching something of your own.

How to calculate and track it:

A good rule of thumb is to keep three to six months of essential expenses in a high-yield savings account. Here’s how to figure out your number:

- Add up your necessary monthly expenses (housing, food, insurance, utilities, and loan payments).

- Multiply that by the number of months you want to cover. So if your essentials total $5,000 a month, aim to set aside $15,000 to $30,000.

Once you’ve built your fund, check in with it once or twice a year. As your life and lifestyle evolve, your safety net should grow right alongside you.

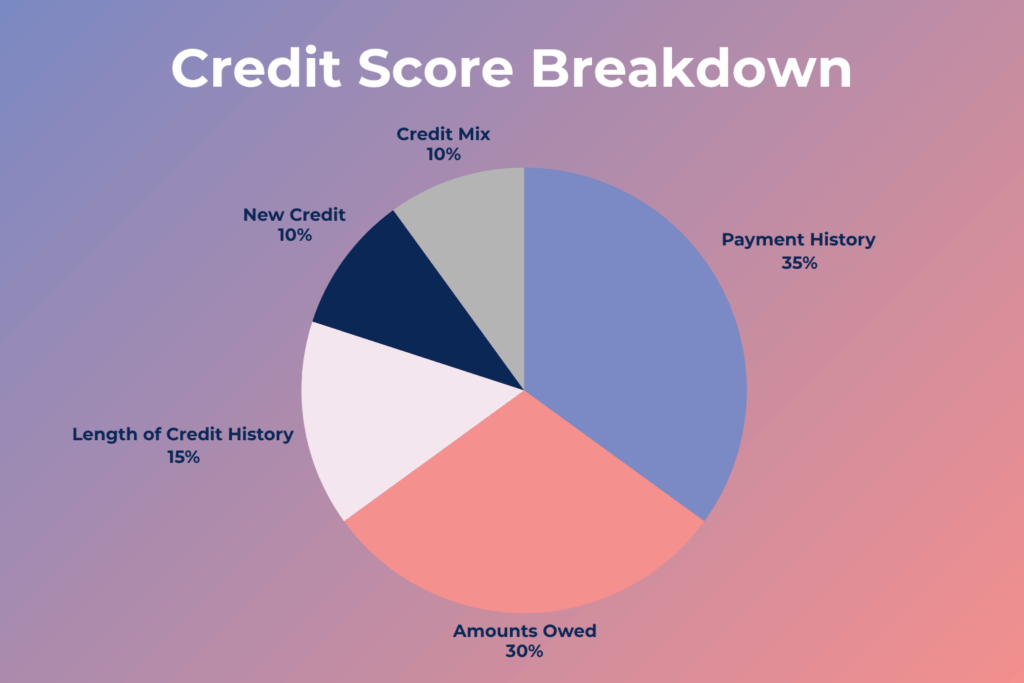

#4: Credit Score

Your credit score is a three-digit snapshot of how you manage debt. It’s built from a mix of factors, including your payment history, how much credit you use, how long you’ve had credit, and the types of accounts in your name.

Scores range from 300 to 850, with higher numbers signaling stronger credit health:

- 800+ = Excellent

- 740–799 = Very Good

- 670–739 = Good

- 580–669 = Fair

- Below 580 = Poor

Why it matters:

Your credit score affects the interest rates you’re offered, determines how easily you can qualify for a mortgage or car loan, and even plays a role in things like renting an apartment or, in some cases, landing a job. For women building careers, managing businesses, or planning major life transitions, a healthy credit score is power.

It’s proof to lenders that you’re in control of your finances, giving you options and leverage when opportunities arise. This flexibility is one of the most underrated forms of financial freedom.

Here’s how to calculate and track it:

You can check your credit score for free using tools like Credit Karma or your credit card company’s dashboard, and it’s worth making a habit of it. Regularly monitoring your score helps you stay on top of your debt management and can serve as an early warning system for potential fraud.

If you ever notice a sudden, unexplained drop, don’t assume you’ve done something wrong. It could be a sign of identity theft, so take it seriously and investigate right away.

Here are a few tips for keeping your credit score strong:

- Pay every bill on time.

- Keep your credit card balances below 30% of your total limit.

- Avoid opening too many new accounts at once.

- Check your credit report once a year at AnnualCreditReport.com to correct any errors.

#5: Financial Wellness Score

Your financial wellness score is your personal gut check. It’s less about hard data and more about how you feel about your money.

In short, it measures your sense of security, confidence, and control: how comfortable you feel making financial decisions, how prepared you are for a curveball, and how steady your progress feels toward the bigger goals you care about.

Why it matters:

Many women carry the invisible weight of financial expectations, family responsibilities, and societal pressure. Tracking your wellness score helps you tune in to how you actually feel about your finances, spot where things might feel off, and celebrate growth that doesn’t always show up in your account balance.

Here’s how to calculate and track it:

Once or twice a year, take five quiet minutes and rate yourself on a scale of 1–10 in each of these areas:

- Confidence in managing your money day to day

- Preparedness for financial emergencies

- Progress toward long-term goals (like retirement or home ownership)

- Ability to make financial decisions without fear or second-guessing

- Overall satisfaction with your financial life

Add them up, divide by five, and you’ve got your personal financial wellness score—the higher, the better. Write it down and revisit it every six to twelve months.

Over time, watching that number rise is a reminder that true financial success isn’t just about having more. It’s also about feeling grounded, capable, and at peace with the life you’re building.

Awareness Of These Numbers Is the First Step Toward Lasting Financial Health

Tracking your financial health isn’t about perfection; it’s about awareness. You don’t need to track every transaction or live in a spreadsheet. Simply knowing and revisiting these five numbers gives you a clear, big-picture view of your financial life. And the more you check in with them, the more confident and intentional you’ll become.

These numbers are simple enough to track on your own. But as your income rises and your financial world expands, things can get more complex. When that happens, Align Financial Solutions is here to help. We partner with women in leadership and female breadwinners to build intentional wealth, without the jargon, the pressure, or the mansplaining.

If you’re ready for financial advice that finally feels like it fits, let’s talk. Schedule a 15-minute Align Call to get started.