Written by Hazel Secco, CFP®, CDFA®

As you look ahead to 2026, your mind might be on new goals, upcoming trips, or a milestone you’re excited to celebrate. You’re probably not thinking about retirement contributions, next year’s tax bracket, or which deductions you’ll be eligible for.

And honestly, who would be? Most of us handle those details on autopilot or deal with them as they come.

Still, a little awareness can make a big difference.

Think of this as a simple guide you can keep nearby as you organize your finances for the year ahead. When you know the key numbers, it’s easier to make choices that are proactive rather than reactive and to move through 2026 with a little more clarity and confidence in the decisions you make.

Table of contents

2026 Retirement Planning Numbers

Qualified Plans and IRAs

Qualified retirement plans and IRAs give you an efficient way to save for your future while reducing your tax burden. With contribution limits increasing in 2026, you’ll have more room to invest, more flexibility in your strategy, and more potential for long-term growth.

- Elective deferral limit for 401(k), 403(b), 457(b), and SAR-SEP plans: $24,500, up from $23,500 in 2025. This is the maximum you can contribute as an employee on a pre-tax basis.

- Age 50+ catch-up contribution: $8,000, up from $7,500 in 2025. If you’re 50 or older, you can contribute this amount on top of the $24,500 employee limit.

- “Super catch-up” limit for ages 60–63: $11,250 in 2026, unchanged from 2025. Savers in this age range get an extra opportunity to put more aside thanks to the new OBBBA rules that separate standard and age-based catch-ups.

- Defined contribution annual additions limit (415(c)): $72,000, up from $70,000 in 2025. If your 401(k) allows it, this is the total amount you can contribute in 2026, including your contributions, employer match, and any after-tax contributions.

- Defined benefit annual benefit limit (415(b)): $290,000, up from $280,000. This typically applies to small business owners and highly compensated employees who use a defined benefit plan instead of a 401(k).

- SIMPLE IRA deferral limit: $17,000, up from $16,500. SIMPLE IRAs are commonly used by small business owners and their employees.

- SIMPLE IRA catch-up (50+): $4,000, up from $3,500.

- SIMPLE IRA additional catch-up for ages 60–63: $5,250, unchanged from 2025.

- Annual IRA and Roth IRA contribution limit: $7,500, up from $7,000. You can put a total of $7,500 into a traditional IRA, a Roth IRA, or any mix of the two. Just know there are income limits for contributing to a Roth IRA.

- Annual IRA and Roth IRA catch-up (50+): $1,100, up from $1,000.

IRA Phaseouts and Qualified Charitable Distributions (QCDs)

The IRS sets income limits that determine whether you can deduct a traditional IRA contribution or contribute directly to a Roth IRA. As your income rises, these benefits phase out starting at the lower end of each range and disappearing entirely at the upper end.

Traditional IRA deduction phaseouts for active plan participants in 2026:

- $81,000–$91,000 for single or head of household

- $129,000–$149,000 for married filing jointly

- $0–$10,000 for married filing separately

Roth IRA contribution phaseouts for 2026:

- $153,000–$168,000 for single or head of household

- $242,000–$252,000 for married filing jointly

- $0–$10,000 for married filing separately

One more update worth noting: the annual QCD exclusion limit for IRA owners over age 70½ increases to $111,000 in 2026, up from $108,000 in 2025. This gives charitably minded retirees the ability to make larger direct gifts from their IRAs.

Health Savings Accounts (HSAs)

If you expect to have a qualifying high-deductible health plan (HDHP) in 2026, pairing it with a health savings account (HSA) can be one of the most tax-efficient ways to save for future medical expenses and even build a pool of savings you can use in retirement. HSAs come with a rare triple tax advantage: your contributions go in tax-free, the growth is tax-free, and withdrawals for eligible expenses are tax-free as well.

Here are the HSA and HDHP limits for 2026:

- Minimum HDHP deductibles: $1,700 single / $3,400 family.

- HDHP maximum out-of-pocket: $8,500 single / $17,000 family.

- HSA contribution limits: $4,400 single / $8,750 family.

- HSA catch-up contribution (age 55+): $1,000.

2026 Estate, Gift, and GST Tax Numbers

The One Big Beautiful Bill Act made several key provisions of the 2017 Tax Cuts and Jobs Act permanent, including the federal estate, lifetime gift, and GST exemptions that were set to drop sharply after 2025. Keeping these higher exemptions in place opens the door to more flexible lifetime gifting strategies and thoughtful legacy planning.

- Annual gift tax exclusion: Remains at $19,000 per recipient in 2026.

- Exclusion for gifts to a non-U.S. citizen spouse: $194,000 in 2026, up from $190,000 in 2025.

- Federal estate, lifetime gift, and GST exemption: $15,000,000 in 2026, up from $13,990,000 in 2025.

- Top federal estate, gift, and GST tax rate: Remains unchanged at 40%.

2026 Income Tax Deductions, AMT, and QBI

Whether you claim the standard deduction, deal with the Alternative Minimum Tax (AMT) because of incentive stock options, or handle taxes as a small business owner, the OBBBA changes several key tax rules for 2026. What stays the same: the top ordinary income tax rate is still 37%, and the maximum AMT rate remains 28%.

Here are the updated numbers that could affect you next year.

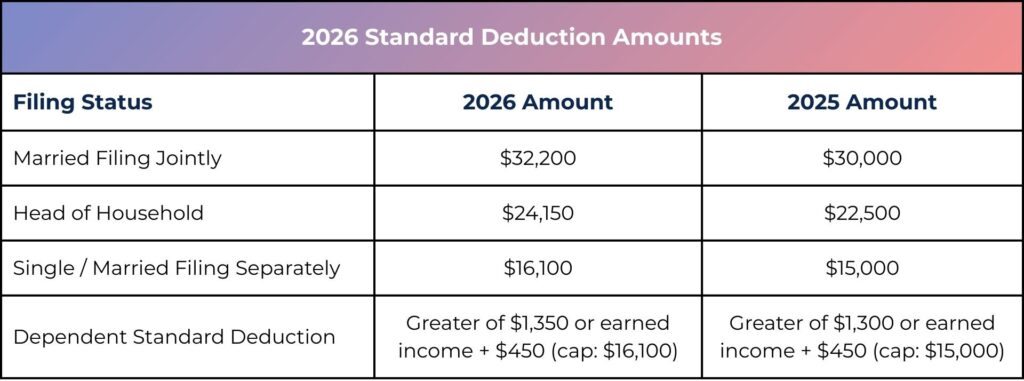

Standard deduction amounts for 2026:

- $32,200 for married filing jointly (up from $30,000)

- $24,150 for head of household (up from $22,500)

- $16,100 for single and married filing separately (up from $15,000)

- The dependent standard deduction is the greater of $1,350 or earned income plus $450, capped at $16,100.

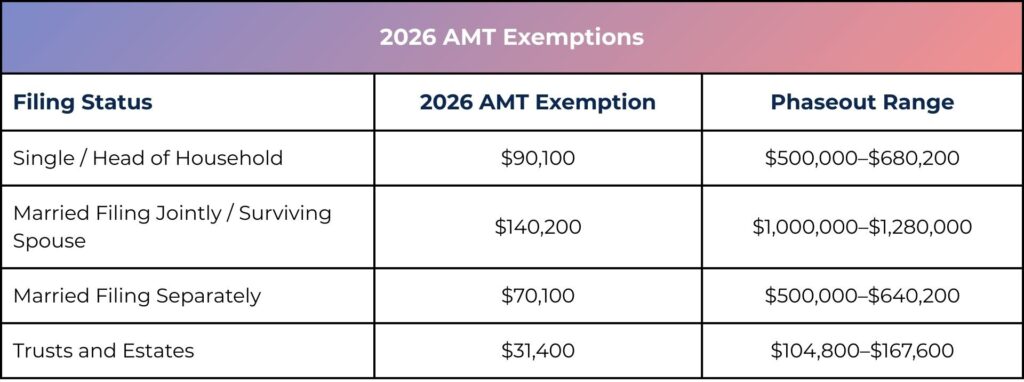

AMT exemptions for 2026:

- $90,100 for single or head of household, with phaseout at $500,000–$680,200

- $140,200 for married filing jointly or surviving spouse, with phaseout at $1,000,000–$1,280,000

- $70,100 for married filing separately, with phaseout at $500,000–$640,200

- $31,400 for trusts and estates, with phaseout at $104,800–$167,600

QBI (Section 199A) phaseout ranges for 2026:

- $403,500–$553,500 for married filing jointly

- $201,775–$276,775 for single or head of household

- $201,750–$276,750 for married filing separately

2026 Capital Gains Thresholds

If you expect to sell stock or other investments with gains next year, it helps to know the updated capital gains tax thresholds for 2026. These are the tax rates that apply when you hold an investment for more than a year. While they may feel steep at first glance, they’re still considerably lower than most ordinary income tax rates, which is what makes long-term investing so valuable.

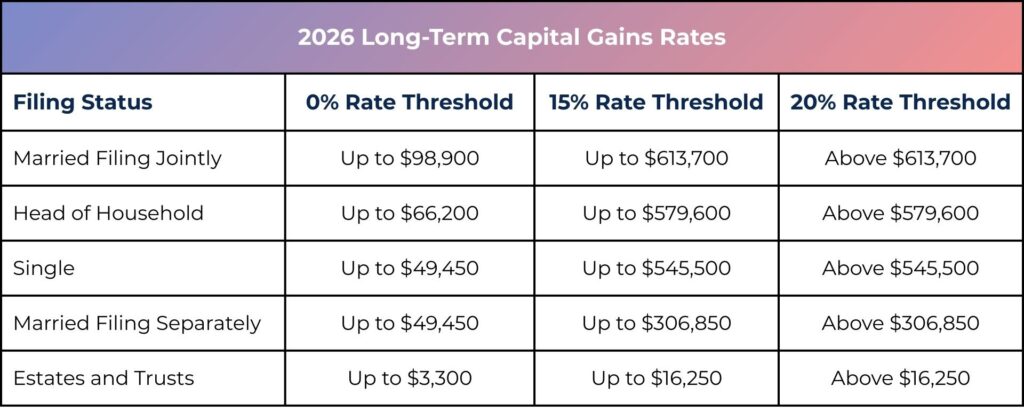

Long-term capital gains tax rates in 2026:

- Married filing jointly: 0% up to $98,900 / 15% up to $613,700 / 20% above $613,700

- Head of household: 0% up to $66,200 / 15% up to $579,600 / 20% above $579,600

- Single: 0% up to $49,450 / 15% up to $545,500 / 20% above $545,500

- Estates and trusts: 0% up to $3,300 / 15% up to $16,250 / 20% above $16,250

Also keep in mind that if your income exceeds the thresholds below, the 3.8% net investment income surtax (NIIT) applies. These thresholds don’t adjust for inflation, so they remain the same every year:

- $200,000 for single or head of household

- $250,000 for married filing jointly

- $125,000 for married filing separately

- $16,000 for estates and trusts

Use These Updated Numbers to Step Into 2026 with Confidence

Understanding these updated limits makes it easier to make thoughtful decisions in the year ahead. When you look at these changes early, you can save with more intention, manage your income strategically, and take advantage of planning opportunities that might otherwise slip by.

If you want guidance as you move into 2026, Align Financial Solutions is here for you. We work with women in leadership and female breadwinners to build wealth with clarity and purpose, without the jargon, the pressure, or the mansplaining.

If you’re ready for financial advice that feels like it actually fits your life, let’s connect. Schedule a 15-minute Align Call to get started.