Written by Hazel Secco, CFP®, CDFA®

Estimated reading time: 7 minutes

Table of contents

CDFA vs. CFP: Which Specialist Do You Need for Your Divorce?

When navigating a high-net-worth divorce, the professionals you invite into your “inner circle” will determine the quality of your life for the next 20 years. While most people recognize the Certified Financial Planner (CFP®) designation, many are unaware of the critical role played by a Certified Divorce Financial Analyst (CDFA®).

If you are currently in the middle of a transition, understanding the difference between these two designations is the first step toward divorce-proofing your wealth.

What is a CDFA®?

A Certified Divorce Financial Analyst (CDFA®) offers divorce financial planning, including invaluable insight and guidance on navigating the financial complexities of divorce. Simply put, a CDFA is a divorce financial advisor or a divorce financial planner. From dividing assets and determining spousal support to creating a post-divorce budget, a CDFA can provide comprehensive support throughout the process. They specialize in analyzing financial information to help you understand the tax implications of various settlement options, ensuring that you make informed decisions that lay the groundwork for financial success in the future.

Why Work with a CDFA?

When your bone breaks, you don’t go to your family doctor. It is crucial to understand the distinction between a generalist and a specialist. A CDFA is a financial advisor during divorce. Thus, they can assess your current financial situation during divorce proceedings and advise on division of assets. They have intricate knowledge of the divorce process and understand the implications of retaining specific marital assets versus others.

Frequently Asked Questions to a CDFA

Can I keep my primary residence?

A frequently asked question we receive is whether one can retain the main home. In divorce settlement discussions, the issue of maintaining the primary home should not be treated as a universal question. Instead, we must consider your overall financial situation, family dynamics, and financial goals following a divorce.

While navigating this question, it’s essential to identify the main reasons driving this decision. Perhaps you wish to maintain stability for your children, particularly regarding their school and community connections. However, it’s crucial to dive deeper into the practical implications of this choice.

Firstly, determine how long you intend to stay in the home and assess the associated mortgage payments. You must understand the financial commitment involved in maintaining the property to make an informed decision. Consider your cash flow during this period and ensure that you can comfortably afford the ongoing expenses associated with homeownership.

Furthermore, it’s vital to weigh the potential financial burdens of keeping the home, especially if it involves buying out your ex-spouse’s portion of the property. This buyout may require significant financial resources and could result in depleting your liquid assets.

Ultimately, while the desire to keep the primary residence may be driven by emotional considerations or practical concerns, it’s crucial to conduct a thorough financial analysis to ensure that this decision aligns with your long-term financial goals. By carefully evaluating the financial implications, you can make a well-informed choice that serves your best interests both now and in the future.

A second set of eyes during the asset division

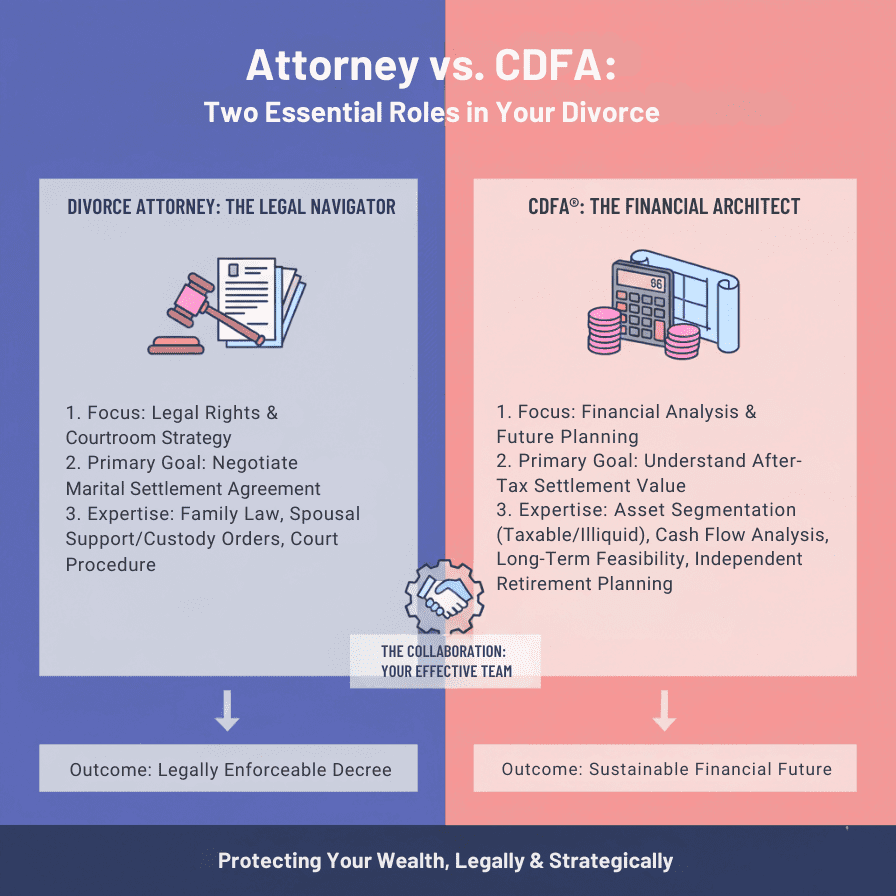

It’s important not to rely solely on the suggestions of a divorce attorney when it comes to asset division during divorce proceedings. While divorce attorneys excel in addressing the legal aspects of divorce, they may not possess the specialized financial expertise required for comprehensive asset division.

Indeed, it’s not uncommon to encounter situations where one spouse ends up with a disproportionate share of liquid assets versus illiquid assets, or investment accounts versus retirement accounts. Understanding the distinction between these types of assets is crucial during the asset division process.

For example, liquid assets such as cash or stocks can be readily converted into cash without significant penalties. In contrast, illiquid assets, such as real estate or certain investments, may take longer to convert into cash and could incur costs or penalties if liquidated prematurely.

Similarly, distinguishing between regular investment accounts and retirement accounts is essential. Retirement accounts often come with specific tax implications and withdrawal restrictions, making them distinct from regular investment accounts. Failing to consider these differences during asset division could have significant financial implications for both parties involved.

Therefore, while divorce attorneys play a vital role in navigating the legal complexities of divorce, it’s advisable to seek guidance from a financial expert, such as a Certified Divorce Financial Analyst (CDFA), to ensure that asset division decisions align with your long-term financial goals and objectives. By leveraging the expertise of both legal and financial professionals, you can achieve a fair and equitable division of assets that sets you up for financial success in the future.

Then, what is a CFP®?

On the other hand, a CFP® (Certified Financial Planner) can help you with overall financial planning, including investment management, retirement planning, and insurance planning. A Certified Financial Planner may not have the same specialized knowledge in divorce finances as a Certified Divorce Financial Analyst. However, they can provide valuable advice on how to manage your finances and pursue your long-term financial goals, not specific to divorce. A CFP® is one of the highest regarded financial advisor’s designations because of its rigorous education requirements and its high ethical standards.

The CFP Board’s Code of Ethics and Standards of Conduct mandates that CFP® professionals adhere to a set of fundamental principles, including integrity, objectivity, competence, fairness, and confidentiality. One of the core tenets of the Code of Ethics is the commitment to prioritize clients’ interests above all else when providing financial advice. This commitment ensures that CFP® professionals act in their clients’ best interests and avoid conflicts of interest that may compromise the quality of their advice.

A Certified Financial Planner is a financial advisor who specializes in comprehensive financial planning including retirement planning, estate planning, insurance planning, and tax planning.

Final Takeaways

In conclusion, both a Certified Divorce Financial Analyst (CDFA®) and a Certified Financial Planner (CFP) can serve vital roles in guiding you through your financial journey. While a CDFA® specializes in navigating the complexities of divorce and planning for an independent financial future post-divorce, a CFP® offers broader financial planning services that encompass investment management, retirement planning, and insurance planning.

It’s worth noting that some Certified Financial Planners may also hold a CDFA® certification, blending expertise in both general financial planning and divorce finances. However, if your current financial advisor is not a CDFA®, it may be advantageous to consider adding a Certified Divorce Financial Analyst to your divorce professional team.

By incorporating a CDFA® into your financial planning process, you can ensure that all aspects of your financial situation, including divorce-related matters, are thoroughly addressed. A CDFA®’s specialized knowledge and expertise in divorce finances can help you make informed decisions and navigate complex financial challenges with confidence.

Ultimately, whether you choose to work with a CDFA®, a CFP®, or both, the key is to have a comprehensive financial plan in place that addresses all of your financial needs and goals. By leveraging the expertise of qualified professionals, you can navigate the complexities of divorce and plan for a financial future that aligns with your objectives.

Feel free to reach out to us today to learn more about how a CDFA® vs a CFP® can help you navigate divorce finances. Our 15-minute FREE Align session can help you determine if we are a good fit.

Follow us on social media to get our latest insights about divorce financial planning.

Disclaimer: Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.