Written by Hazel Secco, CFP®, CDFA®

Estimated reading time: 6 minutes

Table of contents

- Introduction

- Why ESPPs Matter More Than Ever for Women Executives

- 1. Choose a Contribution Level That Makes Sense for You

- 2. Take Full Advantage of the ESPP Discount

- 3. Know the Holding Rules So You Don’t Miss Out on Tax Benefits

- 4. Your ESPP shouldn’t sit on its own island — it’s just one part of your overall wealth plan. It helps to pause and ask yourself:

- 5. Set Clear Rules for When to Sell So You Stay Protected

- Bonus Tip: Use Technology to Make Smarter ESPP Decisions

- The Bottom Line

- Next Steps: Optimize Your ESPP Strategy with Confidence

- Disclosures

- You May Also Like

Introduction

As a woman executive in a Fortune 500 company, you face unique opportunities and challenges. Your Employee Stock Purchase Plan (ESPP) isn’t just an optional perk—it’s a strategic tool to help you build long-term wealth.

Let’s explore key strategies to ensure you’re maximizing its potential in 2025.

Why ESPPs Matter More Than Ever for Women Executives

ESPPs can be an overlooked but powerful way for women executives to build long-term wealth with less effort. Buying company stock at a discount gives you an immediate return, and with the right strategy, it can help you grow your savings faster without adding more to your already full plate.

For women who are juggling demanding roles and big financial decisions, ESPPs offer a simple, structured way to turn career success into financial independence. And when managed intentionally, especially around taxes and concentration risk, they can become a meaningful part of creating a future where work is truly optional.

1. Choose a Contribution Level That Makes Sense for You

The first step is deciding how much to put into your ESPP — and it doesn’t have to be all-or-nothing. Some plans (especially those with higher discounts or a lookback feature) are worth contributing more to, while others with smaller discounts may make sense at a more moderate level.

Pro tip: Start with an amount that feels comfortable for your cash flow, then adjust up or down once you understand how your ESPP fits into your bigger financial picture.

Why this matters: Overcommitting can make your day-to-day finances feel tight, but contributing too little means you might miss out on a simple, low-effort way to build wealth — especially in stronger ESPP plans.

2. Take Full Advantage of the ESPP Discount

Most ESPPs let you buy company stock at a 10–15% discount, which means you’re getting an immediate return the moment you purchase. It’s one of the simplest ways to build wealth without extra effort.

Action step: Take a look at your plan details and make sure you’re actually capturing the full discount available to you.

Key insight: There aren’t many investment opportunities that hand you a 15% gain right away. This is one of the biggest advantages of participating in an ESPP, especially for busy professionals who want their money to work smarter.

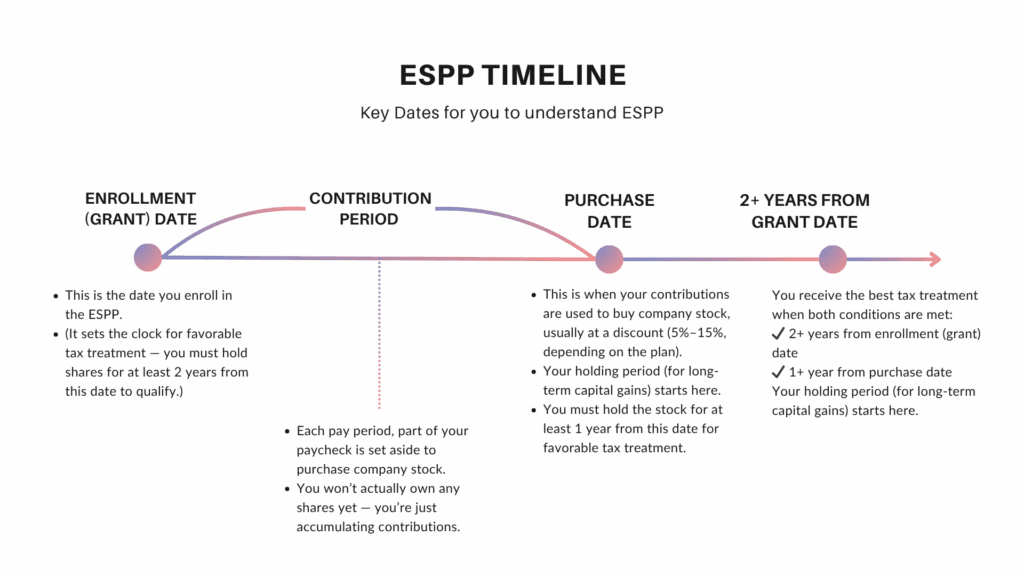

3. Know the Holding Rules So You Don’t Miss Out on Tax Benefits

ESPPs come with specific holding periods, and understanding them can make a big difference in how much you keep after taxes.

Here’s the simple breakdown:

- Qualifying Disposition:

- If you hold your shares for at least one year after purchase and two years after the grant date, you get the best tax treatment. More of your gain is taxed at long-term capital gains rates, which are usually much lower.

- Disqualifying Disposition:

- If you sell earlier, part of your profit may be taxed as ordinary income — meaning a bigger tax hit.

Key takeaway: Taxes shouldn’t drive every choice you make, but knowing these rules helps you avoid surprises and keep more of your hard-earned money working for you.

4. Your ESPP shouldn’t sit on its own island — it’s just one part of your overall wealth plan. It helps to pause and ask yourself:

- How does this fit into my full investment portfolio?

- Am I holding too much company stock?

- Does this support my short-term needs and long-term goals?

Strategic tip: Diversification really is essential. If a large portion of your net worth is in your employer’s stock, you may be taking on more risk than you realize. A thoughtful, structured selling plan can help you lower that risk while still taking advantage of ESPP benefits.

5. Set Clear Rules for When to Sell So You Stay Protected

One of the biggest questions women ask is, “When should I sell my ESPP shares?” The answer depends on your goals — but having a plan makes the decision much easier.

A few guidelines that work well for many executives:

- Decide how much employer stock feels comfortable (no more than 5–10% of your portfolio is a common guideline).

- Once you hit that limit, consider selling new ESPP shares immediately.

- Automate your selling strategy so you don’t have to think about it or accidentally take on too much risk.

Why this matters: Your salary, bonus, and career are already tied to your employer. You don’t need your entire investment portfolio tied there, too.

Bonus Tip: Use Technology to Make Smarter ESPP Decisions

You don’t need to guess when it comes to your ESPP. Today’s financial planning tools make it much easier to understand how your ESPP fits into your broader financial picture and what choices help you build wealth more intentionally.

These tools can help you:

- Compare the tax impact of selling now versus holding longer

- See how your ESPP contributions fit into your full portfolio

- Identify the best time to sell based on your goals and projections

Tech tip: Modern planning and tax tools can run different “what-if” scenarios so you can make decisions with clarity instead of stress. And if you prefer guidance, a financial advisor who works with high-achieving women can help you interpret the numbers and build a plan that supports your long-term goals.

The Bottom Line

Financial planning as a female executive requires strategy, foresight, and confidence. Your ESPP is a valuable wealth-building tool—but only when managed effectively.

- Contribute at a level that makes sense for you. Some ESPPs offer incredible value, while others (like plans with only a 5% discount) may not be worth maxing out. Start with a comfortable amount and adjust based on the plan’s structure and your goals.

- Take advantage of the ESPP discount when it’s meaningful. A strong discount or lookback feature can create an immediate return — just make sure it aligns with your broader strategy.

- Know the tax rules. Understanding qualifying vs. disqualifying dispositions can help you keep more of your gains.

- Make your ESPP part of your overall financial plan. It shouldn’t operate on its own. Look at how it fits into your full portfolio, risk tolerance, and long-term goals.

- Use technology to support your decision-making. Planning tools can help you compare scenarios and understand the tax and portfolio impact before taking action.

- Watch your concentration levels. If too much of your wealth sits in company stock, a structured selling plan can help you stay diversified and protected.

Next Steps: Optimize Your ESPP Strategy with Confidence

If you want to feel clearer and more in control of your ESPP decisions, I’m here to help.

Every woman’s situation is unique — your cash flow, your tax picture, your comfort with risk, and your long-term goals all matter.

If you’d like a personalized look at your ESPP and how it fits into your bigger financial plan, book a call with me. We’ll walk through your options together and make sure your choices support the future you want.

👉 Book a call: Let’s take the next step toward creating a more confident, work-optional life — on your terms.

Disclosures

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. We suggest that you discuss your specific tax issues with a qualified tax advisor.

No investment strategy assures a profit or protects against loss.